Posts tagged Value Pickr

HBL POWER SYSTEMS: Booting-up for the Race of the Century (07-02-2024)

Absolutely, learned this the hard way. Bought this stock at 80 and sold it around 400 levels just on the back of TTM valuations which at that juncture looked very high in a already crazy market. I think the biggest lesson is to adjust the P/E with the growth rate for a better picture. PE in isolation can be very deceiving.

From a minority shareholder’s perspective a big negative point when the company is growing at this scale is they should be hosting concalls for the benefit of the minority investors so we can get better insights of the business.

Disc: Not invested but tracking very closely.

Lupin – Is it the time to buy for long term (07-02-2024)

Excellent Q3 results. Crossed Rs.5000 crores in quarterly sales for the first time, and EBITDA margin crossed 20% after a long time. Surprisingly, Europe’s contributed strongly and US only grew marginally (I thought US sales would be better).

With their recent launches and approvals, the company seems set for a few good quarters unless some FDA issue strikes again or some goodwill write-downs are still left (don’t think so, but they did make a few small acquisitions recently).

The stock’s of course already run up a fair bit. Theoretically, seems fairly valued now, but with the growth momentum and improving margins, can go up some more. If one of their recent and upcoming launches translate into higher sales than anticipated, then it can go up substantially too.

RACL Geartech Limited (07-02-2024)

Results are out. Muted one. Top line up 15% and PBT up by 4%. But more interesting parts is in the notes

NSE listing is big news along with next year sales target of 550 Cr

52 week highs and all time highs strategy (07-02-2024)

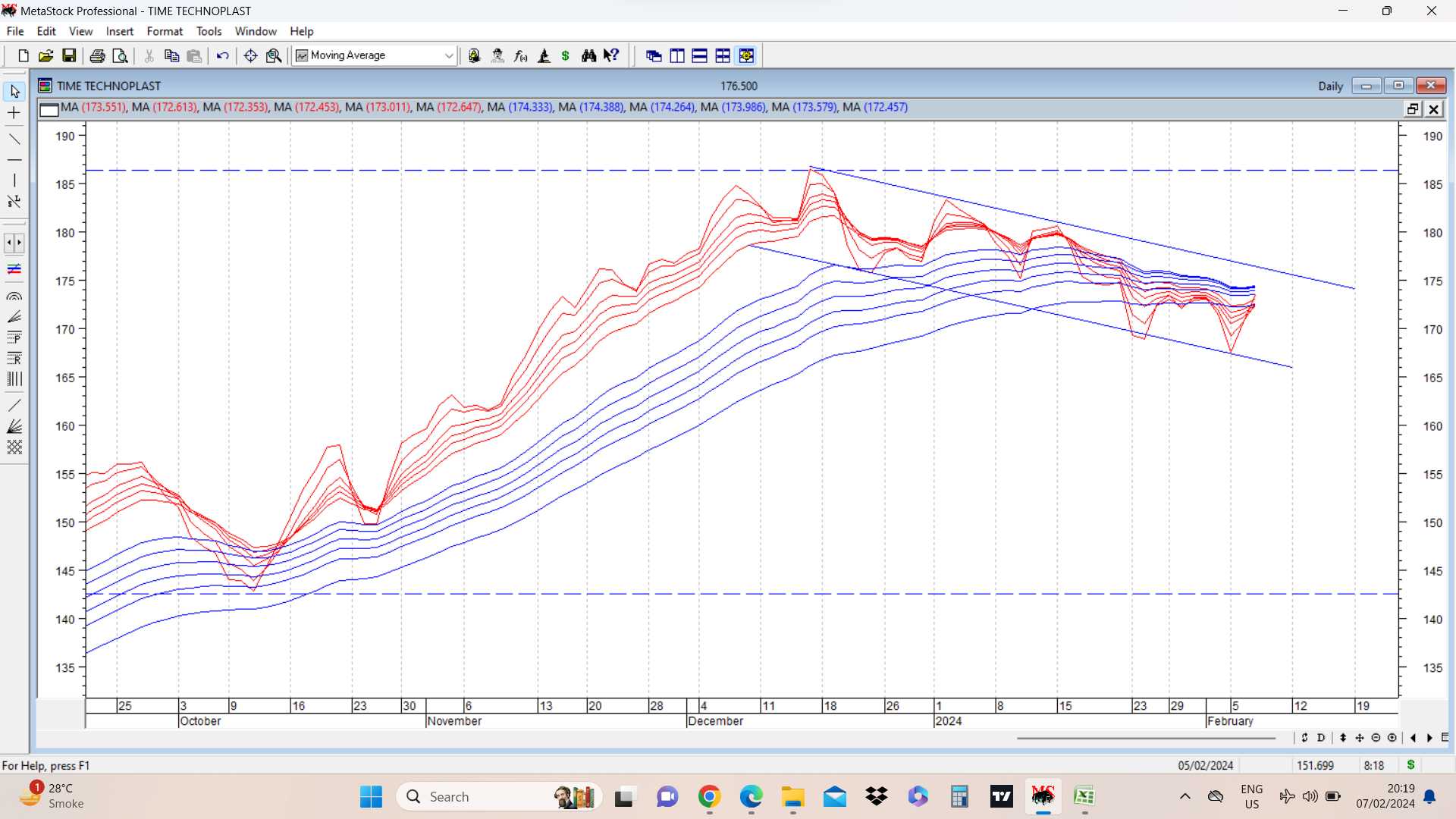

Time techno cmp 175 has been making a variety of technical patterns without going up meaningfully. ![]() Keeps giving knowledge on technical analysis without significant returns since past few weeks…

Keeps giving knowledge on technical analysis without significant returns since past few weeks… ![]() Sometimes it takes a long time for markets to forgive a company with respect to its past sins.

Sometimes it takes a long time for markets to forgive a company with respect to its past sins.

To add to the list of patterns, a flag like pattern is viaible on GMMA ( guppy multiple moving averages) charts. Attached below. Flag extends from 145 to 185, a distance of 40 rs. Breakout point is at 175. There is compression of long term (blue) and short term (red) moving averages. Successful breakout can provide near term target of 215.

disc: invested.

52 week highs and all time highs strategy (07-02-2024)

Do you guys also discuss reversal trends on this thread?

Any views on this?

IEX

Biocon

52 week highs and all time highs strategy (07-02-2024)

looks decently valued and guide for reasonable growth

platform business which has good margin is growing with 20% +

margin recovery good growth with reasonable valutation

looks expensive but with good order book of about 1400 cr guiding for double their revenue next year and 50% cagr growth from FY26 TO 28.

PLZ SHARE VIEWS

DIS. INVESTED

Usha Martin- Coming out of Chaos (07-02-2024)

As per the q3 fy 24 concall, FY 25 will be an year of value added growth. ( sales growth with margins being sustained or improving depending upon how the LRPC and other lower margin business fare)

Capex to come on stream in next month (during q4 fy 24) and will start contributing from q1 fy 25 and will ramp up from there.

A lot of questions were asked about the prospects of the Saudi markets for the company. Company is the only producer in GCC area for Wire ropes and that should hold them in good stead. Plans for establishing manufacturing facility in Saudi Arabia would be considered after seeing the response to the foray.

There was mention of plasticated and other specialised varieties of LRPC products going forward. (already alluded to in previous concalls)

Logistics costs due to global geopolitical situation have gone up and is a risk, but it applies to all the players catering to European markets.

Balance sheet remains healthy in terms of overall debt, cash flow, free cash flow, and working capital.

Waaree Renewables – old Sangam Advisors – can it keep on renewing? (07-02-2024)

Why this stock is moving so much is there any news

Aptus Value Housing : Is valuation justified or just another HFC? (07-02-2024)

Answers to your questions:

-

Capital adequacy is super high because the bank raised a fair chunk of capital during ipo. Debt/equity was also < 1 at the time of IPO. CAR is reducing quarter on quarter as the company is leveraging and will likely move towards 25% at a 4-5x leverage. Aptus is super profitable with 8% roa and 17%+ roe which result in high internal accruals as a result the decline in car and roe is slow (a great problem to have!) and roe is increasing slowly. In order to speed up this process they have started paying dividends (because the raised too much during ipo, when markets were buoyant).

-

No, Balaji is not a relative of Mr. Anandan. He is a very early employee and was brought on board as CFO. Recently promoted to MD, he is super competent.

Disclosure: 25% of portfolio.