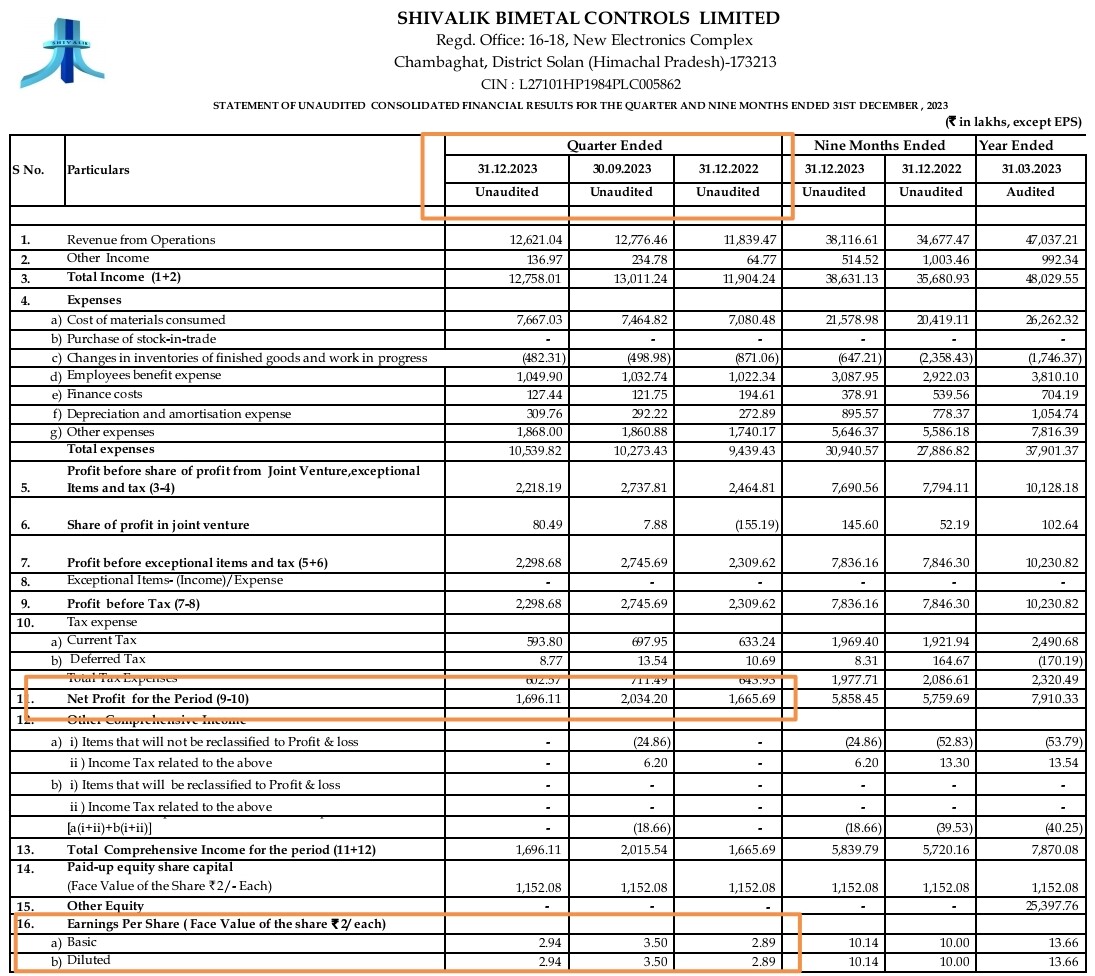

Please check consolidated numbers, YoY bottom line is actually up!

QoQ material costs have gone up, seems biggest contributor to lower PAT, together with slight decline in sales. Also ‘other income’ decreased.

Disc: invested, smallest holding

Please check consolidated numbers, YoY bottom line is actually up!

QoQ material costs have gone up, seems biggest contributor to lower PAT, together with slight decline in sales. Also ‘other income’ decreased.

Disc: invested, smallest holding

Results are out. Big YoY and QoQ drop. This will correct further I think

Nothing. GST not paid by supplier many years ago is not CG issue. Such things happened in business.

Just for example, HDFC was fined for not submitting timely information of foreign subsidary. – we may shocked by such news until you hear management.

Mr D Parekh explained in AGM that the said subsidary is run my single person and hence such delayed happened. Don’t read too much.

Once in a while, I come across investor letters which gives me brainfood to think. Today, I came across yet another one from Greenhaven Road Capital.

Here are a few excerpts I liked:

This point has been circling on my mind lately. The cacophony of narrative that we get to hear (not just from politicians whose primary job is to sell hopium) but also from many marquee market participants about India becoming a $5 tn / $10 tn / $30 tn economy over the next decades when projections few quarters down the line is difficult, if not downright impossible in today’s world.

So in such times, we as fundamental investors need to follow the evidence…

Finally, we should not forget that tomorrow’s results are being baked today. For larger companies, it will take 2/3 years, while for smaller units, 1-1.5 yrs.

So it becomes all the more important for fundamental investors like us to learn as much about the companies we own, the narratives that mgmt teams are sharing, and execution prowess demonstrated YoY (if not QoQ) to enjoy long-term compounding stories.

Do share such insightful investor letters if you’ve come across… ![]()

Birla Cable Current Market Price @ 325 Birla cable last 1 month daily average trading volume 1lakh shares today now more than 30 lakh shares ![]()

![]() any one knows why Increased ?

any one knows why Increased ?

TRacking and Holding from Rs 170 to till now

Naveen, can you elaborate which meeting is scheduled in Chennai today ? NCLT ?

Don’t think HBL will have any role in it. BEL works on a Transfer-of-Technology (ToT) with an Israeli company – Reshef Fuzes (subsidiary of Aryt Industries). There is an article in Haaretz (a popular Israeli News Publication):

Aryt’s main customers are the IDF and the Indian Army. The company has had a long-standing partnership with the BEL company of the Indian Ministry of Defense. Aryt assisted its Indian partner in setting up a factory to assemble fuzes and regularly provides technical assistance in the production and supply of fuze components.

BEL (in partnership with Reshef) is the main supplier of the Indian Army and delivers tens of millions of dollars in orders. “In 2015, we signed an agreement with BEL to help them with everything related to fuze solutions,” Steffler says. “To date, BEL has supplied about a million fuzes to the Indian army, all with our backing and assistance.”

Source: Shooting a Shell Without an Advanced Fuze Is Like Burning Money.

In the same article the there is a reference to this contract won by BEL:

Lately, one of Reshef’s biggest achievements was winning a sizable tender from the Indian Ministry of Defense amounting to hundreds of millions of dollars, with Reshef’s share in the tender in the amount of 170-190 million dollars. “There was a major breakthrough after BEL won a huge tender for a period of ten years, which will bring us projects of some tens of millions of shekels every year for the next decade. Winning the tender is based on our technical advantages. Reshef’s technical capabilities gave the Indian Army the confidence that it was worthwhile to work with us.”

Yes, also when they buy 75% from Glenmark Pharma, any excess shares they receive has to be sold off within 3 years as part of minimum shareholding norms

I think Pe is not the right metric to value shipping business with balatic dry index at an all time high ,revenues would be elevated and shipping is a cyclical buisness.Price to book value would be the right metric to judge this company according to me and it is at an all time high currently.

Our focus on increasing capacity utilization in the quartz sinks category has been steady, with progress reaching 70% by the end of 9 months FY24 and expected to increase further on a quarter-on-quarter basis

We expanded our capacity by adding 90,000 units in the last quarter, bringing the total to 1,80,000 units. The demand in this segment remains strong, with capacity utilization of 67% of the quarter ended 31st December 2023

Our performance in the US and the UK market continues to be strong. The destocking process concluded and inventory is returning to its normal levels

We expect better operating margins in the coming quarters due to various actions taken by improvement in, material sourcing, and business expansion

Howdens is the Number 1 trade kitchen supplier in the UK. It has 750 depots. It has 27 granite

models. They sell 10,000 kitchen sinks per week. That’s 500,000 kitchens per annum. Their gross revenue is 3.3 billion pounds with approximately 20% EBITDA margins. That has been a great feather on the cap for our UK team. And we also have received the first order from them

It’s exciting to inform you that we have initiated the sale of appliances from our new manufacturing setup. By March 2024, our state-of-the-art facility, capable of producing 1 lakh units annually will be fully operational