Amazing growth + maintaining high margins, without bank debt for a small company with high working capital cycle/requirements.

Q3 ppt https://www.bseindia.com/xml-data/corpfiling/AttachLive/ad9e52cb-9f23-4767-a501-78287813e869.pdf

Posts tagged Value Pickr

Zen technologies – A micro cap in the defense space! (31-01-2024)

Kitex Garments Limited (31-01-2024)

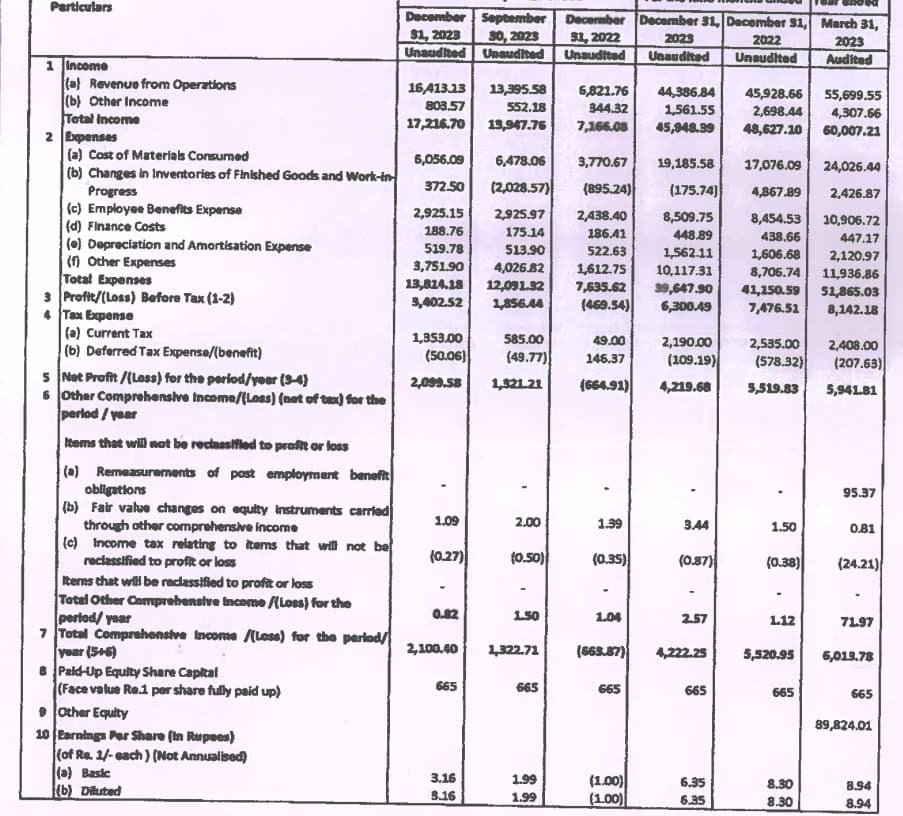

Results are good. With YoY turnaround

Sadhana nitro :a Dog or a Horse? (31-01-2024)

Fixed assets of the company have stabilised indicating completion of capex

Para aminophenol import prices crashed in last 1 year

Possible that company is with holding production due to unfavorable market conditions?

Carysil (earlier Acrysil) – Kitchen sinks (31-01-2024)

Great results from Carysil

Revenue up 37% YOY

Net Profit up 28% YOY

Premiumisation story continues to play out well

Sandeep Kamath Portfolio | Momentum Investing (31-01-2024)

Equal weight portfolio so each is around 5%…

As to the other point, protection mechanism is timely exits…will be scanning through my portfolio every friday and will exit as needed…the idea is to be either in strong stocks or in cash…

Neuland Laboratories Limited – Transformation towards niche APIs? (31-01-2024)

Please check this

Hope this helps

Journey of a Small Cap investor! (31-01-2024)

MPS Q3 numbers were clearly disappointing, more so as the mgt. had needlessly upped the guidance just a qtr ago. The numbers themselves were not that bad, with operating margins getting better despite the set back in the e-learning business. I guess the mgt too has learned its lessons & will hopefully, going forward, let their numbers do the talking! I guess the the pressure of having concalls after every quarterly numbers also gets to the mgt whose enthusiasm to please shareholders can sometimes get the better of their judgement! The mgt. though has stayed committed to their vision 2027 of 1500 crs, & hope to actually achieve it before time with similar margins.

I am of the view that the mgt. is well meaning & have by & large walked the talk over the last 7-8 qtrs, which is a sufficiently long time. I also believe the the mgt. has the wherewithal & ability to grow inorganically by successfully acquiring companies & then integrating them. That is what will create shareholder value in the long run. It matters less that the vision 2027 is realised 2-3 quarters behind schedule but the journey forward should clearly show a pattern in that direction.

The Co. is generating free cash flows of about 130-150 crs annually. Has given a interim dividend of Rs. 30/-, & could easily give another similar final dividend (I think the mgt has mentioned something to this effect in the previous concall, admittedly to be taken with a pinch of salt!) That would make the stock give about a 4% dividend yield.

I feel any meaningful correction from current levels of about 1490 could present a decent buying opportunity & I will look to add.

Kaveri seeds company limited — kscl (31-01-2024)

I liked this point.

In fact, I am doing research on finding secular growth companies for investments. I believe that, in long term, downside can be protected to some extent if one can identify secular growth in sales and profits and EPS all.

Many times, earlier secular growth story may turn non-secular and that impacts stock price on a larger scale than secular growth story.

Stocks which do not demonstrate secular growth in sales and profits, often have deep corrections from time to time. Slow growth is also sometimes acceptable but negative growth in sales and profits generally creates more deep corrections.

This point is not applicable to Kaveri Seeds but a generic point which I am mentioning here.

The PSU Rally- Could Another Ketan Parekh Jack Up Prices Now? (31-01-2024)

PFC is much cheaper than IREDA (I have both). Mr Market has gone bonkers about the PSU stock. Of course they were undervalued, but an apple to apple comparison shows that the market is now assigning too high a value to the PSU stocks.

If one has to choose between a govt management and a Tata managed company, which way should the choice lie? And if on cold calculation too the PSU stock appears overpriced?

The PSU Rally- Could Another Ketan Parekh Jack Up Prices Now? (31-01-2024)

Of course I love them faster. ![]() But sometimes when it is too good, it seems too good to be true.

But sometimes when it is too good, it seems too good to be true.