CreditAccess Grameen is looking attractive after the recent sell-off for a few reasons:

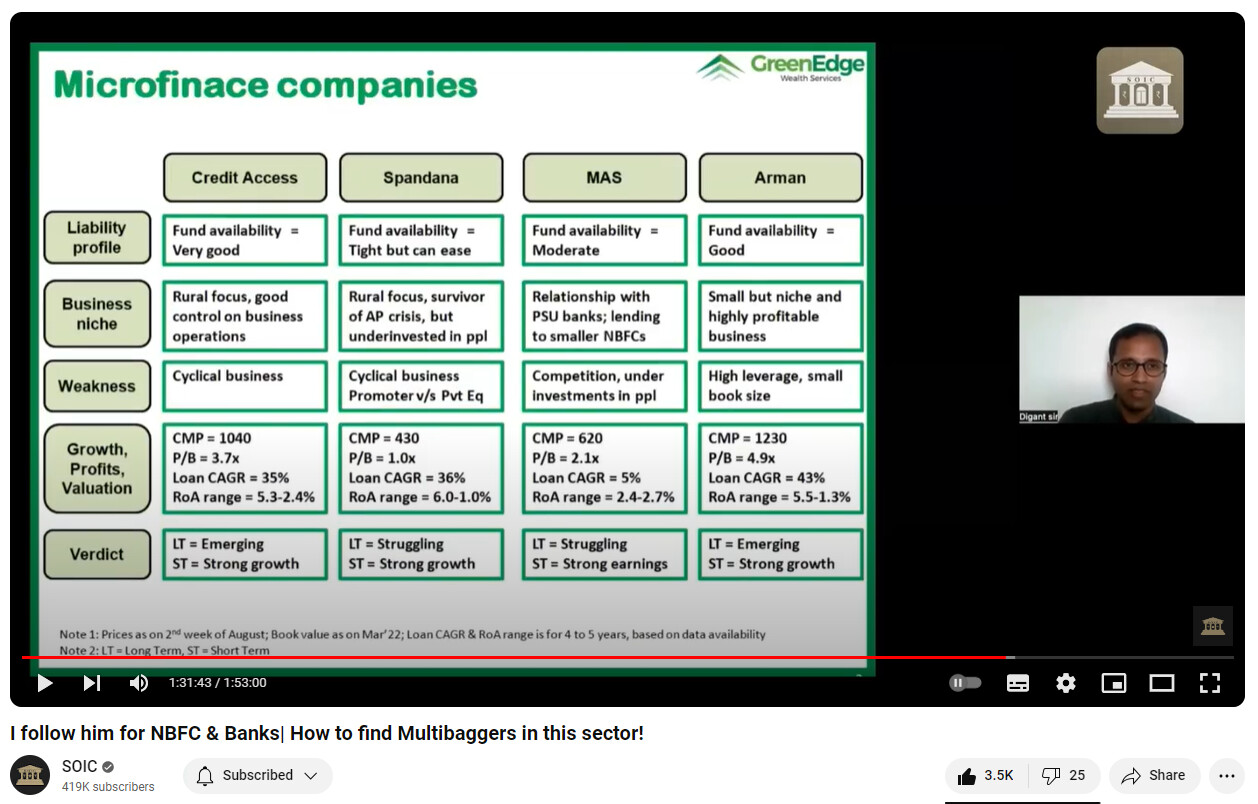

- Largest amongst the NBFC micro-finance cos. with 5M+ customers across 16 states; They’ve developed the largest network and knowledge within the rural lending space

- They have the lowest lending rate amongst microfinance cos (~21%)

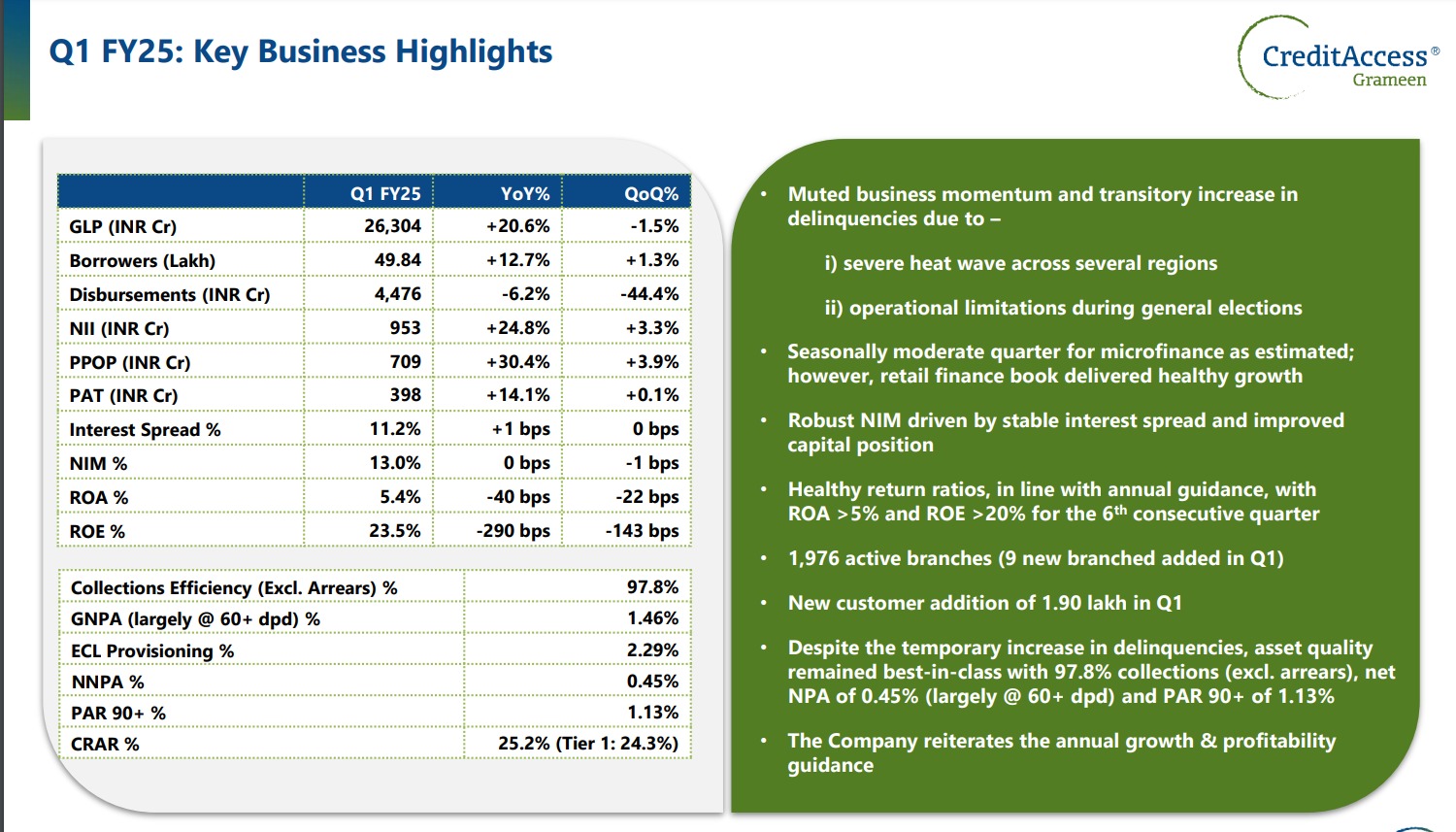

- Growing at 20% CAGR; this is bound to slow down in the future, but there is still a lot of room to grow and I also expect them to increase their market share due to their best-in-class interest rates

- Financially conservative; NIM of 13%, ROE of 23.5% and CRAR of 25.2%

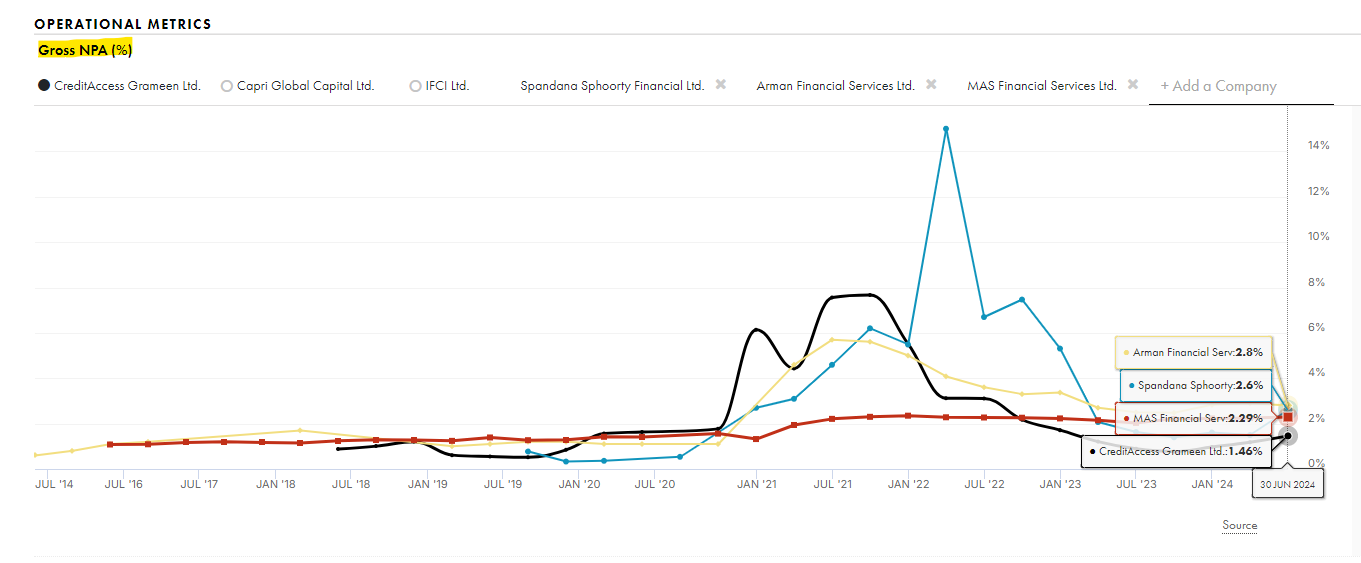

- Seem to be lending conservatively as well: GNPA of 1.46% and NNPA of 0.45%. However, this could shoot up in case of economic distress (GNPA went to 7.6% during COVID)

- Current PE of 10 & earnings yield of 9%+

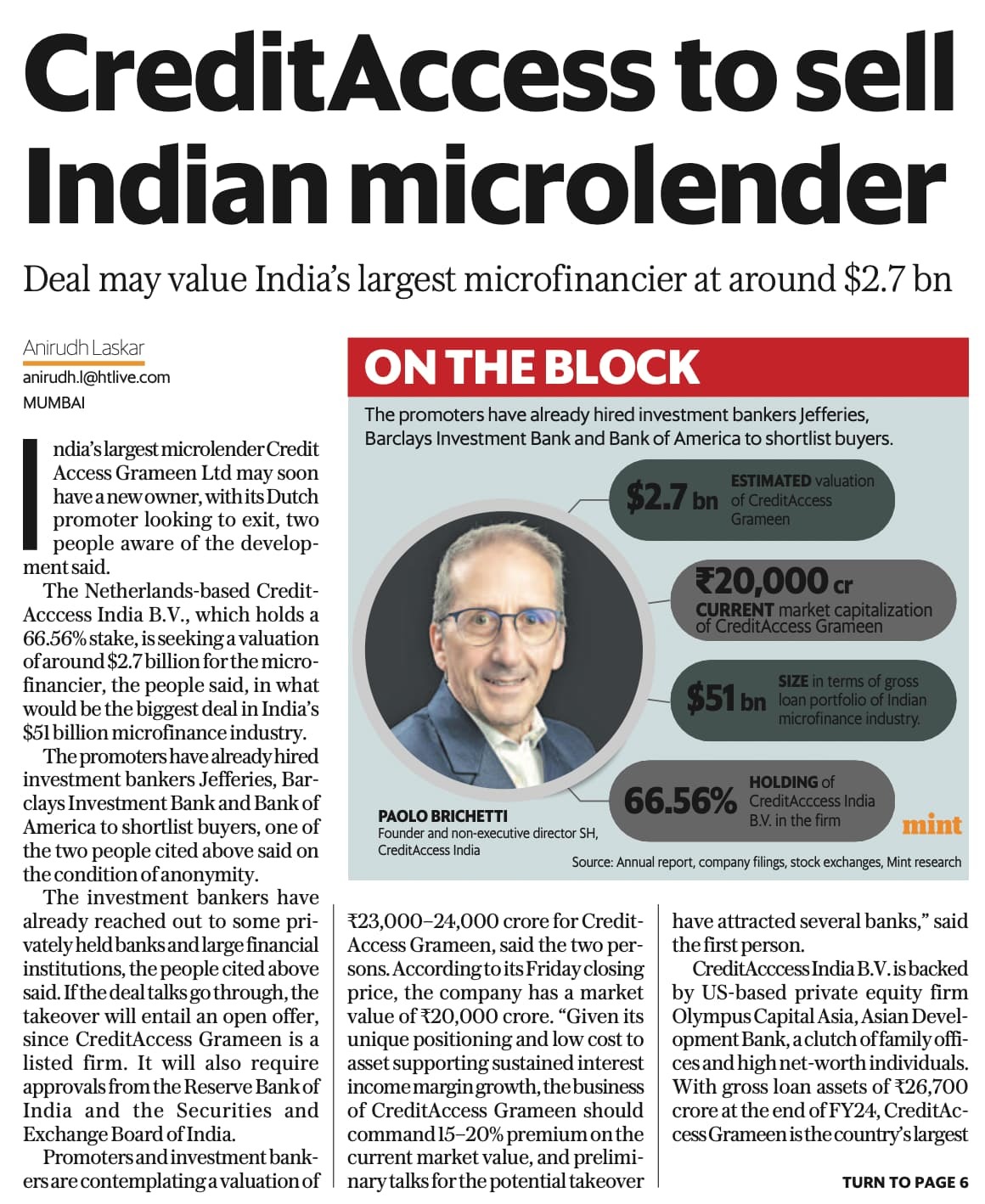

- Paolo Bruchetti, a Dutch national, is the prompter with 66% ownership. Both him and the current management team have a long track record of successful growth and zero frauds that I could find

- Microfinance industry will exist and thrive for the next few decades, as there is still a large percentage of the population that doesn’t have access to traditional banking products or wouldn’t be able to get approved for low interest loans

One of the reasons that the stock has dropped is the concerns over their promoter selling off their stake. However, the promoter is not involved in day-to-day operations even today, so I don’t expect any major changes to management team or company culture.

I didn’t find any obvious red flags, so seems like a great long-term opportunity. Please let me know if I missed any major points.

Sources & further info:

GreenEdge:

Tijori (GNPA):

Disc: recently bought a small position; Will monitor this for the next few quarters and decide whether to increase my holding.

Cheers,

Sharad

OpenSourceInvestor