Anyone knows is there any specific reason for the fall in share price? It could be just because of broader market sell-off if nothing specific.

Posts tagged Value Pickr

Manaksia Coated Metals & Industries Ltd – manufacturing & exporting high-quality coated metal products (22-10-2024)

@SITARA

Q2FY25 results are not released yet, Looks like the above numbers and results are from Q1FY25, can you please check, thanks.

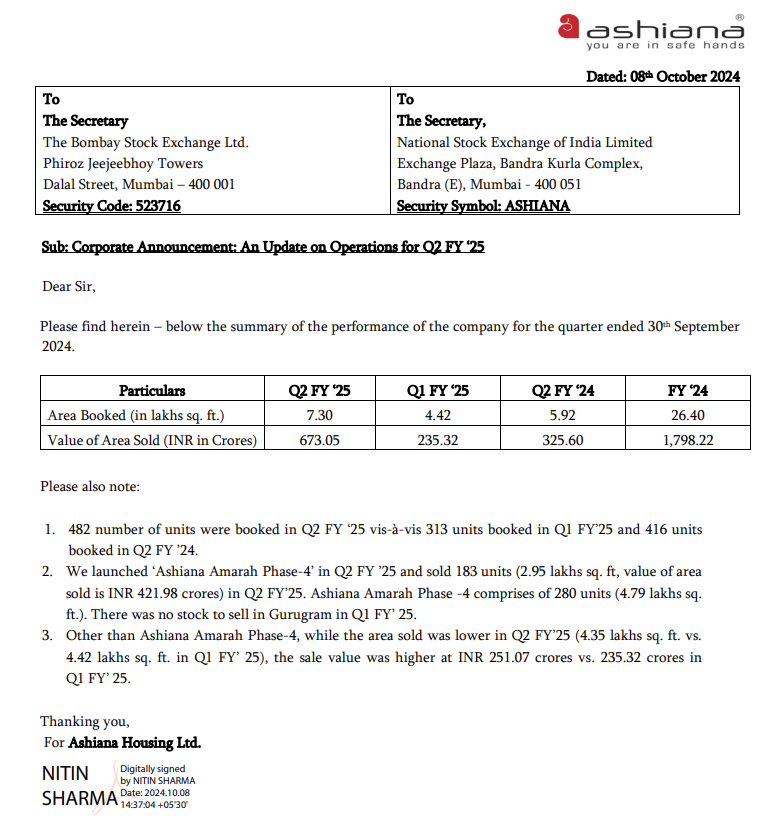

Ashiana Housing – Banking on Tier II and III towns! (22-10-2024)

Company recently announced their Q2 metrics:

Q2FY25 Pre-sales at 673 crores vs 325 crores in Q2FY24 and 235 crores in Q1FY25

PayTM (One 97 Communications Ltd) (22-10-2024)

This doesn’t look good.

Paytm shifts lending strategy, enters into first FLDG agreement to boost merchant loans

Paytm shifts lending strategy, enters into first FLDG agreement to boost merchant loans (22-10-2024)

Paytm shifts lending strategy, enters into first FLDG agreement to boost merchant loans

Aditya Birla Fashion and Retail Ltd (22-10-2024)

A little surprised that ABFRL is still being considered a big bet. The strategy over the last decade has been a lot underwhelming. New brands added haven’t done much.

Legacy brands haven’t been able to reinvent anything. Lifestyle division still rests on the old shoulders of 4 brands. I think you are playing on the demerger theme.

Once they were cautious about what to add to their portfolio and come today they are cautious enough to not leave anything out ![]() Too many brands added. Execution seems to be very very lacklustre. My two cents

Too many brands added. Execution seems to be very very lacklustre. My two cents ![]()

Note: Not invested

Aditya Birla Fashion and Retail Ltd (22-10-2024)

Have the ABFRL shares been allotted the TCNS shareholders?

Your Equity portfolio you can control returns and risk- part 11 (22-10-2024)

Hello Folks,

Sharing the trick of the trade, but everything cannot be done manually need powerful analytical tools. For risk computation I have used tool.

Let me begin with an example- I take 3 large caps ACC, Axis Bank and Apollo hospital (Neither I recommend nor reject these scrips, I take this as example for illustration purpose only)

What I have is, I have last 3 years monthly closing price data, I have found the difference between closing price of successive month and found the return. But I need to convert this return in into 1 Rupee invested, how much return I am getting . Hence what I have is delta=(P2-P1)/P1 for 36 months. Average return=sum(delta)/36, standard deviation (risk)= standard-deviation of sample ( delta)

Here is my data in excel for all the 3 scrips-

Now what I do is I change the weights from 0.6,0.25,0.15 to 0.4,0.3,0.3 see how return/month has increased as well as risk has reduced!

One need to know We can vary these returns for these scrips between range (0.5 to 1.6%- expected return).

But risk also varies, Same returns can be obtained in more than one ways, but only one of them will have least risk. That is what user should discover.

Combined standard deviation or risk is based on 2 things- scrips can also have covariance, it means their risk is not independent, the risk of one scrip is related to price of another scrip, some scrips rise and fall together, some are opposite-means if one rises the other falls. This relationship we need to know.

Hence, I used a web-based tool to compute weights with minimum risk by using this tool – see the report attached.

This tool also has advanced option – in screen 2-to vary return to max, min or average and then generate the report. I use it for my portfolio results are quite impressive!

SAMPLE REPORT.pdf (99.7 KB)

See the optimized scrip has slightly lower return-in this case- But still if this is my scrip, I still would go with optimized scrip as it reduces my risk. During correction or downfall every % reduction in risk helps in resisting fall.

Red Tape Ltd. – The next fashion giant? (22-10-2024)

Went through their online portfolio as well as visited some stores. I’m a bit worried that they are explicitly becoming a discount store.

While I do agree that other good brands(Nike, Adidas) also use this in India but I don’t see non discounted products at all. Without premiumization there can be 2 big issues :

- Brand being looked as a discounted product brand only – might have negative connotations attached about it in the minds of people despite being a good product(eg Tata Nano being linked as a “lakhtakiya”/non rich product)

- Pricing power being taken away from the brand if the customers have an anchoring bias in their minds.

Does anyone have any insights on if they are planning to try and premiumize their offerings or at least have a fresh stock of non discounted products so that not every red tape shoe is discounted at 80% ?

Disc : invested and part of top 3 holdings.

Kalyani Cast-Tech Ltd – An Innovator in Container Manufacturing (22-10-2024)

Detailed risk analysis & disclosure of your holding is missing.