when it comes to travel, the two Jim Rogers book one with motorcycle and one with his mercedes, combined finance with travel nicely! Always enjoy your summaries and find new books had not hit upon yet! Thanks.

Posts tagged Value Pickr

Dreamfolks services limited( DFS) (26-01-2024)

Bank cost varies with lounge, i.e. Delhi lounge access is costlier than Patna lounge access. The cost is a function of lounge area, food menu

I had an opportunity to discuss this with Patna airport lounge operator

Investment strategy review (Long term) (26-01-2024)

Welcome to the forum. You are in the right forum at a very young age, that is good.

There is no safety in equity, even with MFs. MFs too lose money, the NAV can fall by 20%, and if we don’t want to sell, then we have to wait for longer periods. Better to have a number in mind and time period in mind, because it is volatile, there is no compounding here, the returns are not linear, they are volatile, it goes up and down, what good it is if we want to withdraw and the NAV is the same as 2 years ago, because it has fallen and not yet moved up. Direct equity is an ocean, so it will take time.

Go through freefincal.com for MF related things, it helps.

Invest in debt, if you are concerned about return and safety. And if you think of emergency, split the investments into different products, along with a debt fund, you can go for RDs, keep some in the bank account, keep hard cash too, because in emergency, liquidity is important, we will need cash. With debt funds, there could be limits for instant redemption, and redemption requests may take 2-3 days.

In the initial years, keep it simple, don’t think about returns and focus on learning. And as time passes, with the gained knowledge, and with the capital from your profession, you can do a lot of things, so focus on your profession too.

Investment strategy review (Long term) (26-01-2024)

Thanks. This was a good read. Definitely looks like I still have some homework to do. But the main thing that’s concerning me is the money that I’m earning right now is being stored in my savings account and is getting inflated as we speak. That’s why in the mean time I wanted to invest it somewhere.

Will spend some more time learning and reading portfolio building topics and will probably make some better choices then.

HDFC Bank- we understand your world (26-01-2024)

I had always wondered about this contradictory behavior of returning cash to shareholders via dividend and then raising additional capital by diluting shareholders. Dividend payout ratios for ICICI, HDFC have always been much higher than Kotak which had promoter shareholder who was more aligned with shareholders. Dividend yield for large private banks has been around 1-1.5% where as for Kotak it was around 0.07% so big difference of 100-150 bps vs 7 bps.

I think this behavior is explained by looking at the management incentives. Banks are typically valued at BVPS. When large private sectors banks prefer to raise funds when are trading at P/B of 3-5 unless they are forced to raise funds at lower valuation. Suppose bank BVPS is 100, P/B of 4 (share price of 400) and bank has 100 shares outstanding and. When they issue dividend of 1 then updated BVPS is 99.

Now bank issues 1 share at 4 P/B so updated share count 101. Earlier total book value was 100100 = 10,000 now new book value is 100100 + 1*400 = 10400 so BVPS is 102.97 and now Raising money at P/B > 1 raises book value. Increased book value with same multiple leads to higher share price. 102.97 * 4 = 411.88 (price bump from 400)

If you look at history of growth in the book value of HDFC Bank then you can see book value increasing 3-4% every quarter from net income and also increasing in larger step whenever they did share issuance (typically every 3-4 years whenever price was suitable)

This benefit starts to dilute when P/B decreases towards 1 and reverses completely below P/B of 1.

IDFC First Bank Limited (26-01-2024)

This exact question was asked to Mr Vaidya on the recent CNBC interview after earning. https://www.youtube.com/watch?v=BpQ-AR6FIaU Listen from 0:45 mark onwards.

Here is explanation from the MD:

“It just a specialization it’s a specialization you have and people should be should appreciate able to lend a particular segment in a very low risk model with a low credit cost I think we should get used to.”

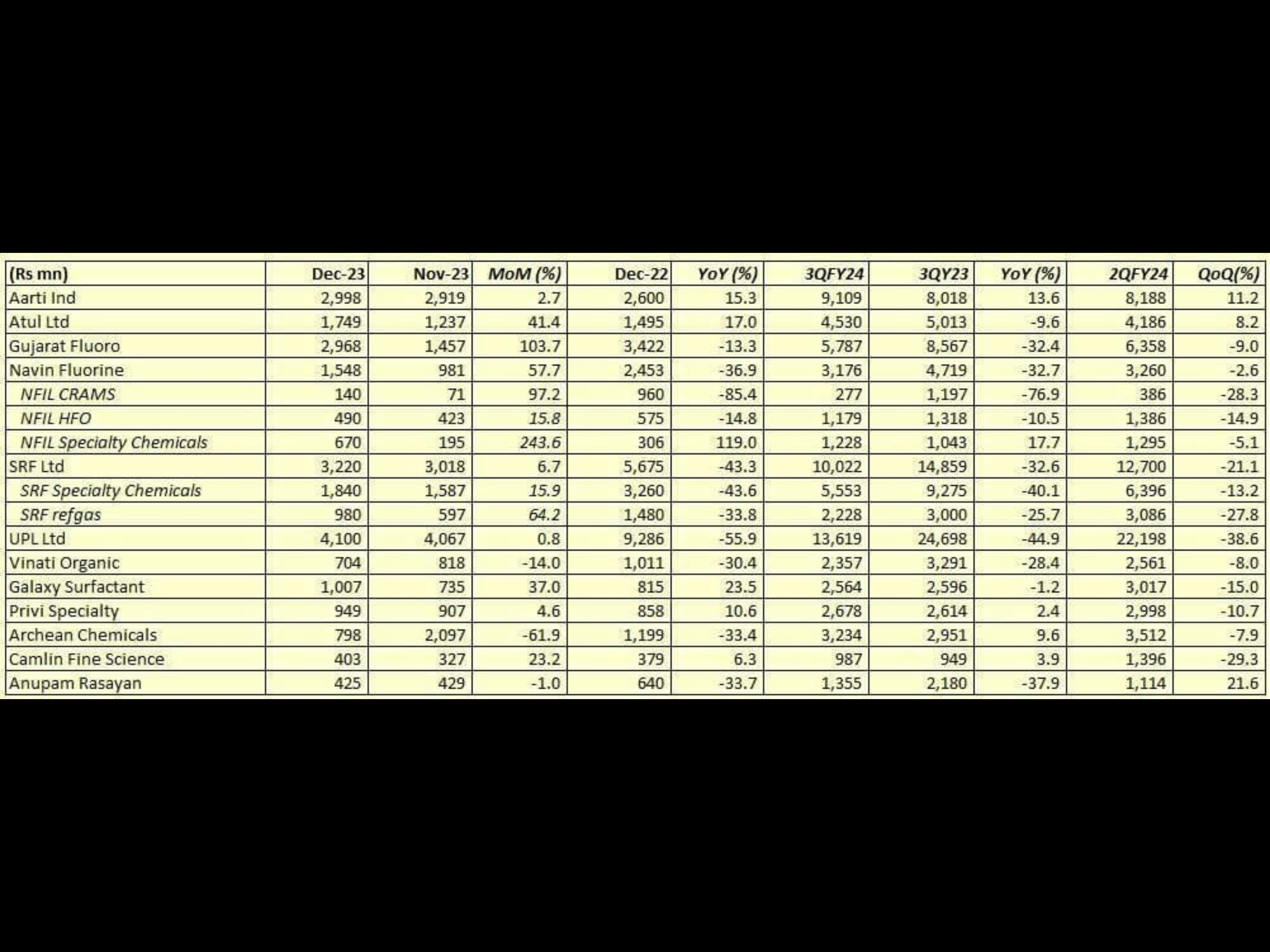

Amara Raja Energy & Mobility Limited: Powering Ahead (26-01-2024)

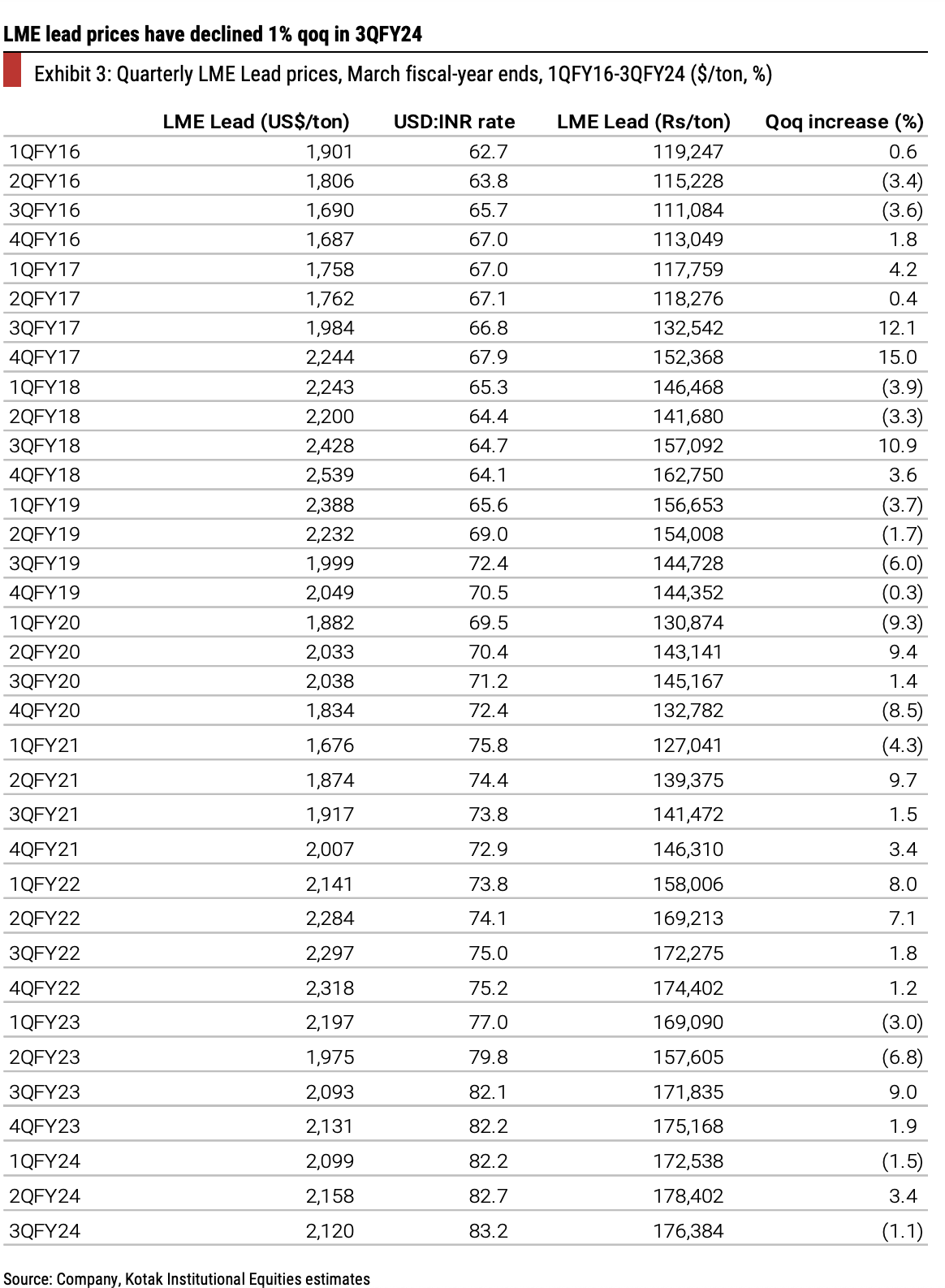

LME Lead pricing

Investment strategy review (Long term) (26-01-2024)

You said that “…will probably change the approach” so I think it’s too soon for me to comment/evaluate something. Plus, you seem to have just started so I don’t want to be critical.

From a broader perspective, I can suggest the following:

1. Luck and Skill are two different things

There has to be a rationale for the decisions you make. I am not able to find a rationale in your allocation or investment choices. Casual decision-making leads to casual outcomes. If it’s a casual choice, then you need to be ready to live with the consequences when things go wrong.

2. Past performance does NOT guarantee future performance.

I do not track Invesco so do not what’s going on there. Your expectation about linear returns tells me that you need more time in the markets before I can advise. A few years back, a large bank that seemed to give consistent returns for years has been now going through a price correction.

3. Safe assets are NOT for return maximizing.

Maximizing returns will bring risks. I used to try to maximize returns on debt investments and was lucky to learn early why not to do it. Perhaps, you will have your own lessons.

Try understanding the Franklin saga and why Investors got locked in the popular fund.

4. Choosing your teachers

This again is quite concerning. Not talking about the quality of their advice but the advice-seeking process. In general, you need to choose people whom you want to learn from.

5. Portfolio Construction

When I said “3k can’t be considered as a part of the PF”, I meant that I would consider its value to essentially become zero. It might never reach there but there are reasons why I would consider to be 0. You can read about “portfolio construction”.

6. Maths.

The numbers don’t add up. From 1cr to 5cr is 5x in 5 years. That too, when you’re starting with 55% of investments in safe investments.

Given your age, your income might increase with time but then it’s generic information since I do not know the growth trajectory (for example: how much % increment, frequency of increment etc).

Plus, you’ll need to consider the fact that your expenses will likely increase. Also, there can be unpredictable circumstances – say health emergencies. Think of people dependent upon you. There’s a lot more to this. Once again, I think you should read about “portfolio construction”.

If I have to review your approach currently, I would say there are several shortcomings. But I do believe that it doesn’t matter where one starts from as long as we end up right. Further, sometimes we need to burn our hands to understand fire. As long as one keeps on introspecting and working on themselves, one gets there.

Disclaimer: I am not a SEBI registered research analyst or an institution. These are my personal views. My views keep on changing with learnings and time and I often go wrong.

Annapurna Swadisht Ltd – A Swadisht FMCG investment? (26-01-2024)

I think they have not included the SME feed into their data. Annauprna, Dentalkart, Alphalogic Industries, Inflame Appliances, Robu are some of the names that I tried and are not coming up.