Hi Shashank, as Sonacomstar has consistently decreased its shareholding, isn’t it a red flag?

Posts tagged Value Pickr

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (26-01-2024)

Any view on Balrampur chini , uttam sugar and avadh sugar… the details on them is very less on internet or concall.

Should we invest in CMP or wait.

Jubilant Ingrevia – Life Science Ingredients (LSI) (26-01-2024)

I also read this in their exchange filing but unable to understand what will they do with this acquisition. What benefit will the company get with this acquisition.

SmallCap Hunter : Trying to find the dark horses with triggers (26-01-2024)

Aries agro

Hemant instruments

Rico auto

Good company for studies on valuation and growth

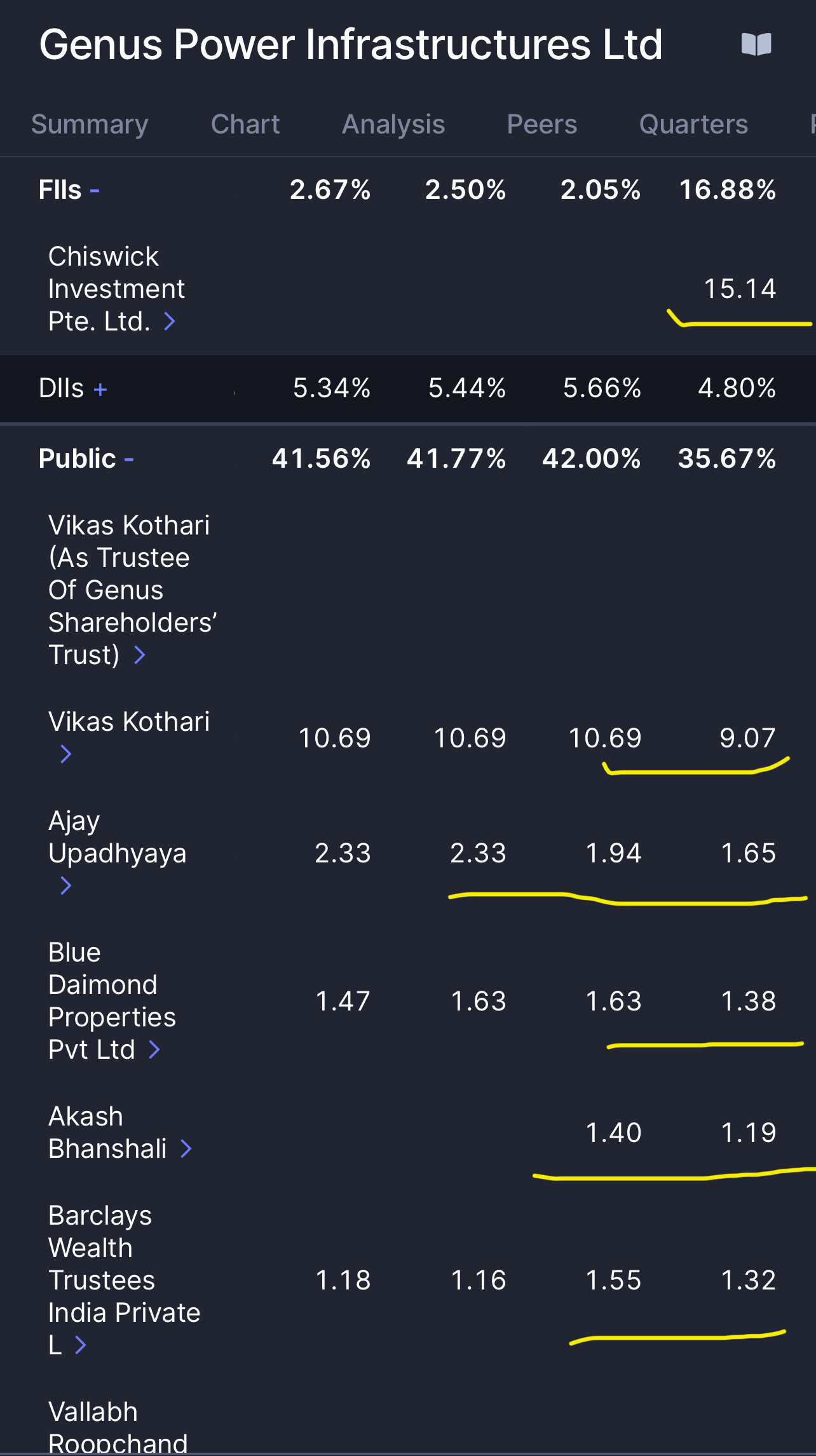

Genus Power – Smart Metering (26-01-2024)

@narayans79 why is their name not in the investors list anywhere?

“ Genus Power & Infrastructure on Wednesday announced that Singapore’s sovereign wealth fund GIC will acquire a 74% stake in the company’s new smart metering solutions venture for $2 billion (over Rs 16,000 crore).6 Jul 2023”

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (26-01-2024)

@MANU_JINDAL

Good analysis done by you. While the numbers add up – which is evident by increase in recovery, increased cane crushed by 3% and high sugar and ethanol stocks, it is not reflecting in share price – this is only due to poor representation by the company (CFO). Even as per my estimates minimum share price should be Rs. 230 – 250 price in 6 months.

Regarding the recovery-cost calculation:

If cost of cane is Rs. 350 per quintal, if recovery is approx 10% then sugar production is 10 kg and cost of sugar is 35 (350/0.10) and if recovery is 11% – cost of sugar is 31.8 (350/0.11) so 1% improvement in recovery is Rs. 3.2 reduction in cost. In fact if the numbers are calculated more accurately, then the total margin improvement is higher at Rs 1.4 per kg and not Rs. 1 per kg (after improvement in recovery and increase in cane cost to Rs 370).

With higher volume, higher margin will have a multiplier effect.

The MD is very good – explains all numbers in detail and has answers to any questions asked- shows that he is very hands on. This is the biggest comfort for me. In turnaround cases hands of MD / promoter is most important for success. The best decision was to postpone the new ethanol plant. I am sure with his focus on cane development, energy efficiency projects, pharma grade sugar, etc DBOL could replace Dwarikesh as the most efficient sugar company.

But the CFO is surely not doing a good job of good investor presentation – even in the concall he just reads out from the presentation which everybody has already read !! Nevertheless I see this as an opportunity to make money when the numbers improve and stock price appreciates.

PS – there is one more reason for the share price to remain depressed. At the time of split, Dhampur Sugar Mills price was Rs. 300. After 1:1 split, Dhampur Sugar current price is 250 and Dhampur Bio is 150 – put together it is 400. so investors are selling Dhampur Bio and keeping Dhampur Sugar as it is believed to be the better company – which may be true at the time of split but with the new capacities DBOL will be better than Dhampur sugar – they have one more plant (and higher crushing capacity) which means more command area and more sugarcane. Implying that share price should be 250. In times of mkt volatility i think it is a very safe bet.

Genus Power – Smart Metering (26-01-2024)

This Jan update is purely GIC stake induction… when there is stake dilution existing share holders % obviously gets reduced

Genus Power – Smart Metering (26-01-2024)

Typically, ace investors know more and before it’s public.

Is the stake reduction by them a sign of worry?

When the main execution is shortly coming up and the smart metre future is so bright — why will they want to reduce stake?

Invested. Puzzled.

Linde India Ltd. – A Case Study by a Newbie! (26-01-2024)

Linde India nowhere mentions anything about it exploring green hydrogen business at all. Annual reports, presentations nowhere? any source you have outside company docs that proves green hydrogen business pursued by the company?

Vedant Fashions (Manyavar) – Niche Branded Retail (26-01-2024)

Comments are encouraging, but I would like to add a point-of-investment thesis on my end. The bet is on the premiurization and management strength and, of course, the liquidity available at the free float. They are doing great business in their niche area, with increasing foot traffic and the expansion of stores. They operate on a franchise model, which is asset-light, and of course margins have not changed with the addition of so many new outlets. The crux of margin impact can only be seen in the EBO’s, but with Twamev stores, the asp ticket is about in the range of 30k to 40k, and selling the goods of 10-15qty itself is sufficient to overcome the expenses of individual stores, and the rest would lead to profits. I have visited Twamev EBOs in Hyderabad. The collection is extremely good, and the price point starts at 30K+. The area in which they operate this store is elite. Of course, the footfall may be less for Twamev, but the sales average is close to Manyavar even with the lower volumes. In otherhand, in terms of age of population, India is a nation with a higher number of youngsters who are unmarried. The mantra is simple, an increase in per capita will lead to an organized market, and when this happens, it is a win-win for Vedanta fashions and shareholders.