Merger will add the cash of Rs. 211 cr in HoldCo to the SFB and also there will be share cancellation. In overall the BVPS will increase by more than 2.5 per share

Posts tagged Value Pickr

Elecon Engineering Limited (25-01-2024)

if you see sept and dec 22, revenue is flat. March in general there is a 10 – 15% jump.

In the current year, they have done 1373 Cr. March had 474 cr. Assuming a 12.5% revenue jump in March, total year becomes close to 1906 cr. In my mind, they may marginally miss the 2000 mark – they will not be way off.

Tata Technologies (25-01-2024)

Good Numbers by TATA TECH

Total operating revenue up 14.7% YoY and up 1.6% QoQ to ₹12,895 million

Services revenues were up 5.8% YoY

Continued improvement in the customer ramp-up activity, with 39 customers now in the

million-dollar-plus revenue bucket compared with 34 at the end of Q3 FY23Operating EBITDA at ₹2,366 million. Operating EBITDA margin at 18.3%, a 140-bps increase

QoQ driven by improved Services gross marginsNet income at ₹1,702 million; Net margin at 13.2%

Net headcount addition of 172; Workforce strength of 12,623

Vedant Fashions (Manyavar) – Niche Branded Retail (25-01-2024)

What I fail to understand is why they still compare with FY20! FY23 was a very normal base especially Oct22-Dec22, why do they not compare with it?

Plus their sales increase is always meagre and margins have started to decline, marginally but yes they are!

Their whole strategy is to open more stores and drive sales from data driven marketing and collection which does not seem to work so far. They are already in all the metros and Tier 1 towns of India. I doubt they will have a much customer base in Tier III and IV as compared to Tier I and II.

Wearing nice looking clothes in weddings isn’t a habit which they will inculcate in people. Just saw the interview of Vedant Modi, shared by another member an hour back, and he mentioned that almost 90% of their sales is wedding driven. I do not see a lot of optimism at this point of time with the subdued numbers one quarter after another!

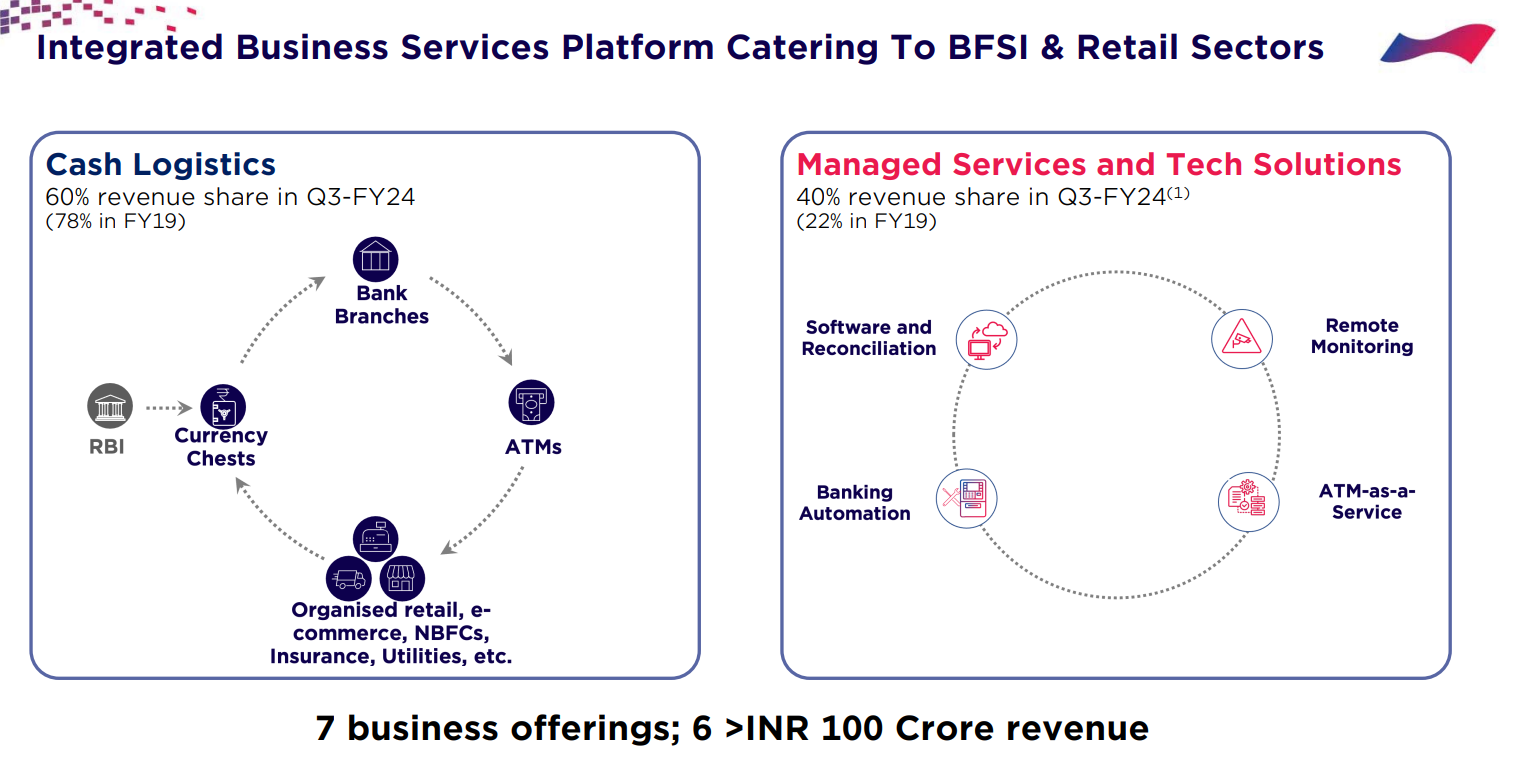

CMS Info Systems Ltd (25-01-2024)

I don’t know why the market is not giving valuation to this company.

Pros-

Good Mgmt,

Leader in their sector,

Back to back good results(slight dip in margins in Q3)

Cons-

Increasing cashless system in the economy

UPI trend increasing.

Anybody who is tracking this company can elaborate why the market is not giving value to this company?

Vedant Fashions (Manyavar) – Niche Branded Retail (25-01-2024)

Since it is seasonal business, you need to compare results on YoY basis ( this quarter with same quarter last year). YoY numbers are 11% top line growth and 7% EPS growth. For a stock having 67 PE, it is pretty average performance to be honest. Not sure how market would react though…

IDFC First Bank Limited (25-01-2024)

Good thoughts. They are doing unsecured retail/ rural loans mostly but have a low creidt cost. So, Bank obviously has good underwriting process in place.

What do you think of their spread or Avg yield on advances? I couldn’t get that number… should Yield be like 11-12% to be able to get 6+% NIM?

South Indian Bank (25-01-2024)

Very good run-up in stock after the result from Rs. 28 to Rs. 33. So, obviously results are taken up very well by the market. Below is my comment on Q3FY24 results:

-

To repeat, Since the corporate book is a shorter term with very high ratings, NIMs will continue to remain under stress until MSME loans are not grown. The share of Corporate Loan in the mix increased Q-o-Q and MSME reduced. So, a thing to watch out for.

-

Employee expenses have been a bigger issue in the last few quarters due to which C/I Ratio is increasing. Despite a marginal reduction in employees and adjustment of 24cr. one-time additional expenses in Q3FY24, the cost has grown. So, again need to see how this will be managed.

-

However, slippage numbers are well as guided. Also, GNPA, NNPA, PCR, etc. numbers along with ROA (>1% now) and ROE (>15% now) are very encouraging signs and as guided by management.

-

But we need to be again careful that this ROA/ROE are outcome of very healthy recoveries. We need to analyze ROA/ROE given that recoveries slow down going forward.

-

The major focus area is laid down to grow MSME loans and rationalize costs by management in Q3FY24 with no clear guidance as of now. However, he mentioned that we will continue to function the way the previous MD has laid and make some slight changes as we go ahead.

Conclusion:

I will keep tracking this stock till the time I get more hang on the new MD at SIB. Also, actively looking to see how MSME will grow with good underwriting standards. Currently, looking at numbers would not be in a hurry to buy as I have already taken an exit post Q2FY24 results.

No-Position Currently

Regards,

Mukul Jain

CMS Info Systems Ltd (25-01-2024)

Increase tech business % and decreasing Cash Management business %.