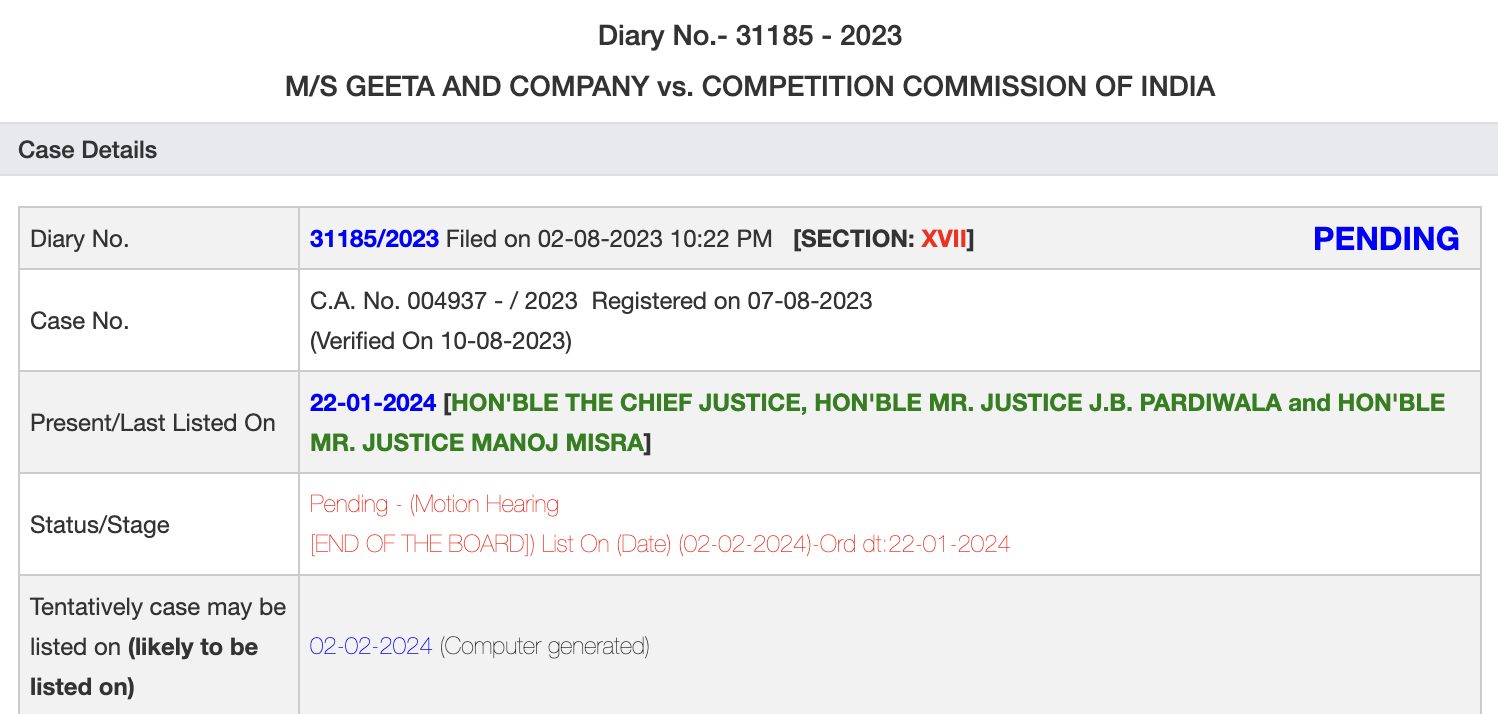

check sci website with this diary entry. 2nd feb is the tentative date for now.

check sci website with this diary entry. 2nd feb is the tentative date for now.

Correct

It depends on the various prices at which such equity capital has been raised. For instance IDFC First raised around Rs 2,196 crores by issuing around 37.75 crores of shares @ 58.18 per share in March 2023. On Oct 6, it raised Rs 3,000 crores by issuing about 10% fewer shares – 33.24 cr @ 90.25 per share.

I had worked out (my post above) that y-o-y PAT growth had been 18.4%, EPS growth was much lower at 4.47%. I calculated EPS on Issued shares, but the company has substantial exercisable options that would dilute EPS further

q2 fy24 (edited and added some data points).pdf (2.6 MB)

q2 notes with some data points from DRHP

Sorry for the late reply. Was a bit busy.

1 – Yes. Sector rotation can give a better CAGR than simple long-term compounding with fewer transactions. But as I have said, THESE ARE MY PERSONAL OPINIONS. And I am ‘not that smart’ to analyse and know which sectors will turn around. And waiting on the sidelines means not investing any fresh capital. The study of businesses is a continuous ongoing process in the background. And conviction is not a BLIND one. Long-term doesn’t mean you don’t track the businesses. The days of buying it and forgetting it are gone. You need to analyse each and every one of your businesses quarterly.

2 – Nowadays, it’s very difficult to differentiate between noise and knowledge on SM. We don’t know other people’s incentives. Yes. I know with a few technical indicators like RSI, etc., we can determine which sectors are trending. But again, you have to be on your toes to do it. One important point to remember is that – Retail investors are different from asset managers. At least I am investing along with my private medical practice. Asset managers are under pressure to perform every quarter ( which we retail investors don’t have to). Recently, I have reduced following everyone who is in asset managing/advisory, etc services. They have their own incentives. Nowadays, I try to follow individual investors who don’t have such incentives.

3 – It takes time to know whom to follow and whom to avoid. I am still learning that after three years of investing. Yes. For us retail investors, developing your own ideas is nearly impossible. We must depend on social media and prominent authorities for the stock names. But here, we have to avoid the HERD MENTALITY and AUTHORITY BIAS. Mohnish Pabrai is a huge proponent of ‘CLONING’. However, the stock ideas that you get from your authorities are only the first step in the stock filtration process. Then, you have to apply your own criteria for investing in them.

6 – I am slightly biased here as I have gotten excellent returns from SIP investing in PPFAS since its inception in 2013. YES. This looks like a good strategy to increase your SIP amount in, say, a kind of bear market and reduce it in a bull market.

But overall, your points are pretty much valid, provided you are a full-time investor.

For a part-time retail investor like me, it’s impossible to analyse and predict future trends and invest accordingly. At least, I am not that smart.

dr.vikas

the route for their majority export that is china is different orignating from bay of bengal although some impact on japan(8% of export revenue) going from red sea route can be there

source of info: DRHP

Even if they grow profitability at 20℅, EPS growth would be below it due to equity dilution. Isn’t it? For example, if the bank raises Rs 5,000 crore of equity capital and the profit grows at a CAGR of 20%, the EPS growth would be around 16%.

Is it a right assumption or am I missing something?

In the prevailing scenario, characterized by a widespread increase in provisions across the banking sector, it is imperative to acknowledge that a diminished margin of safety persists concerning asset quality or non-performing assets (NPA) for virtually all banks.

Taking a lighthearted perspective, it becomes apparent that short-term challenges are nearly unavoidable. In such a context, it would be judicious to regard five-year projections as aspirational, recognizing the dynamic nature of the current scenario.

Bro, did this tentative case hearing heard on 22 Jan?

.

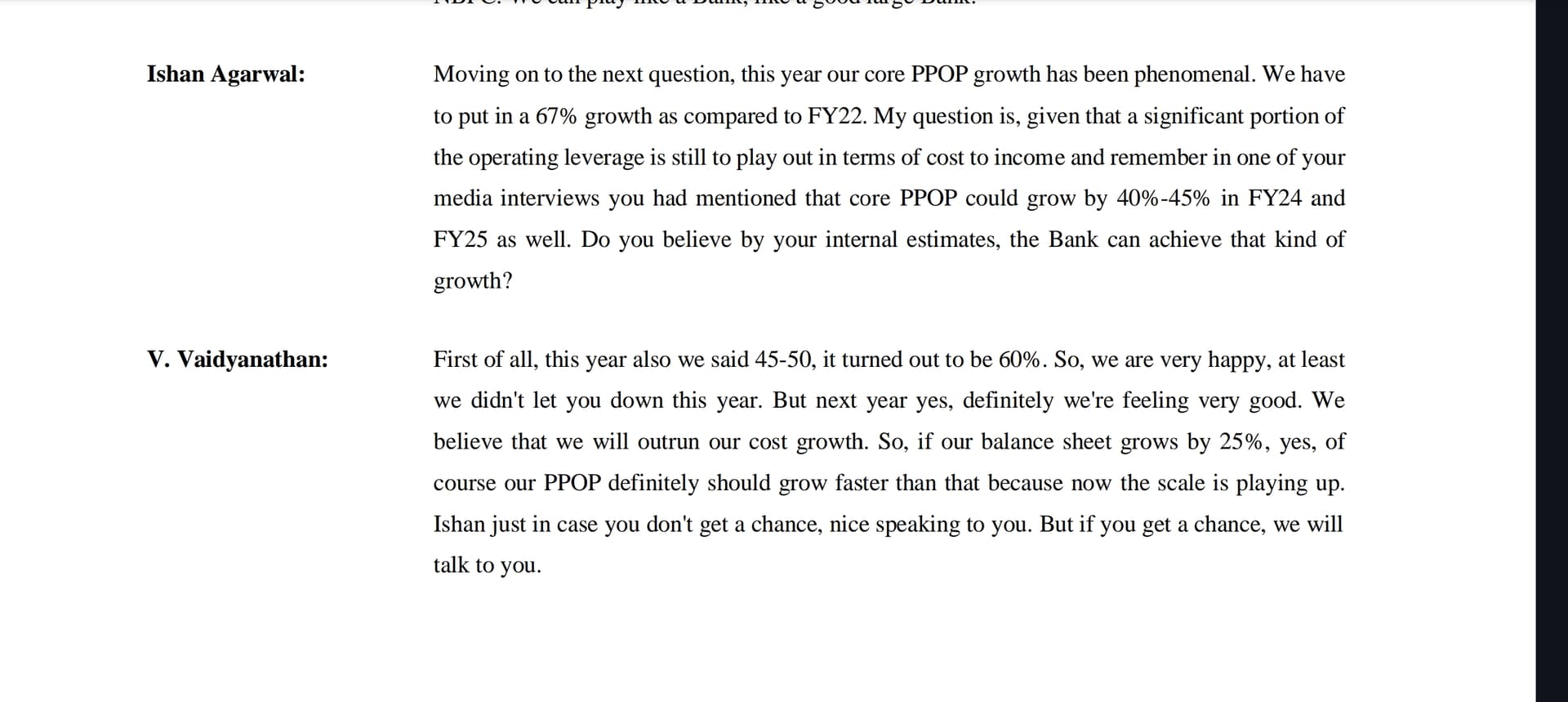

This is from Q4 concall on April 29th, 2023…Vaidya repeated same thing in many of his media interviews along with terms like ‘opening of the jaw’ and ‘J curve’ to signal that profits will grow significantly but in reality profits are declining from last 4 quarters along with dilution of equity.

.

Also comparing IDFC First with other established banks and saying that it has performed better than those does not seem to be the right way to looking at things imo, there is NO OPERATING LEVERAGE story at play in other good banks, they are already at a respectable number in terms of ROE, ROA and Cost to Income.

The problem is with management

over promising and under delivering and still trying to promise more in form of guidance 2.0

It’s not about judging it every quarter but about seeing the direction in which it’s going, bank’s performance is slowing down significantly QoQ and it will start showing in YoY number also from next quarter onwards.

First, thank you very much for the feedback!

Great suggestion! I have always been confused about allocation, particularly in terms of balancing my portfolio. I am learning everyday and trying to develop a clarity on allocation. I have been following my feelings, which is far from ideal. What is your suggested method for reducing allocation? Do I sell my positions to reduce allocation? I always thought that I would rather exit the stock completely if my thesis is invalid – for example, if there is a risk of losing money beyond what I can absorb or if the result of the uncertainty turns out to be unfavorable.

As you have correctly noted, my largest allocation is in a negative basket. The money comes from the sale of SBCL and MAPMYINDIA in September 2023 and therefore, it looks skewed. There will be another skewed allocation after I sell the railway sector stocks. I put in fresh cash every month to the value basket which slowly evens out the allocation over time.

Apologies for pinpointing, but it’s important to note that Vaidya never made promises of that nature. It’s a common understanding that neither he nor anyone else in the market can guarantee specific outcomes. provisions has increased this quarter, and the management, along with several members in this group, has already provided explanations for the reasons behind it.

I echo the sentiment of @Sanjeev_Bansal in acknowledging that we might be placing overly high expectations on the management, anticipating improvements every quarter, which may not align with the realistic dynamics of the real world.

It’s essential to recognize that Guidance 2.0 is just that a guidance not a dream. Whether IDFC First achieves it or not remains to be seen, and only time will reveal the outcome. Let’s stay informed and monitor their performance to better understand the trajectory we’re on.