VBL has Jan – Dec financial year, so there will be no quarterly results. Audited annual results can be declared within 2 months. Last year results were on 6th February.

Posts tagged Value Pickr

Monte Carlo Fashions-Branded Apparel Stock at Good Valuation (22-01-2024)

monte carlo has always had low PE due to the uncertainty in sales…

AGI Greenpac- on the cusp of growth? (22-01-2024)

The HNG acquisition by AGI is challenged by the Kenyan company – international sugar, who were number 2 in the bidding round of HNG. They quoted much less than AGI.

Their plea is on flimsy ground that CCI approval was given to AGI post facto.

They first filed their appeal in NCLT and subsequently in NCLAT – which they lost.

Now they have appealed in Supreme court in October.

SC is yet to hear.

My only point here is these delays on flimsy grounds defeat the very purpose of IBC wherein despite losing bids losers keep filing petitions to scuttle the process. In the end HNG, it’s employees and other stakeholders are big time losers.

Sukhjitstarch and chem (BSE CODE 524542) (22-01-2024)

My only observation is how does a company give such a high dividend when all financial metrics have deteriorated QoQ and YoY – PAT, EBIDTA margins, increasing debt…

and there is huge fluctuation in share price…

Cosmo Films – Diffentiated player in commodity business (22-01-2024)

All in all doesnt seem to be a good investment… lots of hype and no delivery…

Borosil Limited (22-01-2024)

Shares would have already been credited in your demat account with klasspack name, Zerodha/Groww would show them once they are traded…

Ascendant’s Portfolio (22-01-2024)

Are you comfortable with valuations of varun beverages? And also whats your returns expectations in next 5 years?

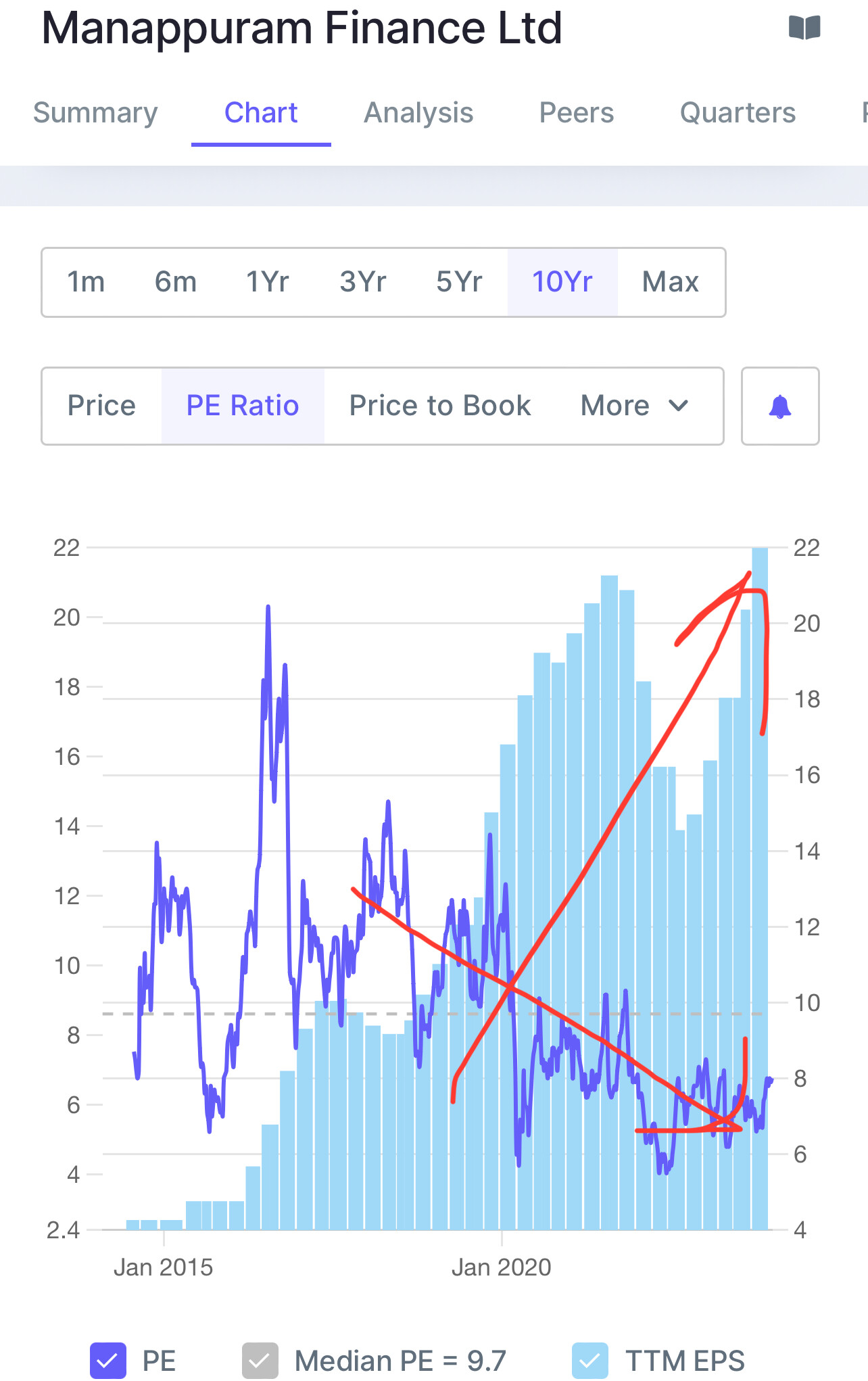

Manappuram Finance (22-01-2024)

Well, mostly market looks at Pure Price and there hes been a good increase. There should be a are rating now that promoter issues is behind and business continues to do well.

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (22-01-2024)

Govt. doesnt want to take a chance – as the production could be lower and so closing stock estimates can end up being wrong and sugar prices can shoot up. Only when Maharashtra mills stop crushing in Feb/ March when decision on ethanol will be taken.

As far as farmers are concerned they are quite content as SAP has been increased by Rs. 20 (industry was expecting Rs. 25) and sugarcane is the most profitable cash crop today.

Regarding Dhampur Bio – the stock has reacted negatively because the numbers are not presented well. Points to note for Q3 numbers:

- Recovery has increased by 0.82% – this is big jump. I was expecting a 0.5% improvement this year and 0.5% next year. Company has done very well on this front.

- Cane crushed is higher by 3%. Hopefully this will increase to 10% by March.

- Sugar production has increased by 35%. Ethanol has come down.

- Sugar realisation is > Rs. 40 per kg (at this price sugar has higher margin than ethanol)

- Sugar and ethanol stocks are higher than last year. Sales was lower as per quota alloted. This could turn out to be better as prices are expected to increase going forward due to higher cane prices and expected early close of crushing in Maharashtra.

(I think the CFO should do a better job at presenting numbers – that too after they have appointed a Investor relations advisor !!) Information on C Heavy ethanol is missing. (there is lots of info which not captured…)

Recovery rate is the best metric to analyse a sugar company as that is what contributes to margins. Other factors like plant efficiency does not matter much now as all the mills have upgraded or are in the process of doing it over next year.

As per my estimates, Balrampur Chini, Dhampur Bio, Awadh will perform better as there is room for improvement on recovery and also efficiency. Sugar-ethanol mix for these companies are ideal ad also the single plant sizes are in the range of 7,000 to 10,000 tpa (crushing capacity). Companies like Dhampur Sugar, Triveni are already fairly valued and there is low scope on improvement on either valuation or financial / operation performance. Even ethanol capacity for these companies is on higher side.

Manappuram Finance (22-01-2024)

Fascinating chart: EPS is rising, yet the price-to-earnings is decreasing. Similarly, book value is increasing, but the price-to-book is declining. Unsure if I’m overlooking something or if it’s a market oversight.

It’s unexpected to find such a paradoxical chart during a bull run. Curious to see how long the graph will maintain this paradoxical trend.