This is actually a very positive news for psus . Since the mistrust in psus was only because of this babu attitude of their management. If management is kept in line then they are all gems with very good income generating asstes.

Posts tagged Value Pickr

Use of Large Language Models For stock research (21-01-2024)

Also for test would require some people help to test the functionality.

As everything is dockerized so by using just postman a person can question , put pdfs etc in it.

I know making a cool UI would make things easy but firstly I am a back end first person and testing with a front end will only delay this at the end

SmallCap Hunter : Trying to find the dark horses with triggers (21-01-2024)

It looks like the company is looking to delist – offering price of Rs 155. Interestingly the book value of Shardul Securities is close to double that of its market price. Hence I expect that the promoters will likely not get to 90% at the price they are currently offering.

MTAR Technologies – A wager on innovation meeting economies of scale (21-01-2024)

MTAR Technologies – is trading at a market capitalization of INR 6,600 CRORE at a P/E ratio of 64 times (approx). This is after a recent correction in the stock – however the stock still looks expensive for an entry point.

After reading the latest Q2FY24 earnings call transcript, here’s my summary:

Cons

- Revenue guidance was reduced from INR 860 Cr to INR 700 Cr for FY24, due to deferral of shipments to Bloom Energy. This just goes on to highlight how dependent the company is on ONE customer. Any adverse impact in the business of Bloom, will directly impact the topline / bottomline of MTAR

- EBITDA guidance has been reduced from 29% to 28% to 26% (+/- 1%) now for FY24

- Borrowings have increased by INR 108 crore, no commentary from the management in the Q2 call on ^

- Cash flow from Operations were negative, due to significant decrease in payables.

Pros

- Expecting domestic sales to be 3x in H2FY24. In H1, domestic sales was INR 50 Cr, expected to be INR 150 Cr in H2 with higher margins

- Expecting Order book to close at INR 1,500 Cr for FY24 end

- Received order from NPCIL (defence business), revenues of which should flow from FY26 onwards

- In the pre-qualification stage for SSLV technology – would be interesting to see if any revenue drivers can emerge from this

- Added more companies in the Clean Energy space, but didn’t reveal any names. It is imperative for the company to de-leverage from Bloom Energy to built a robust business model

- Could capitalize on import substitution opportunity for ball screws, roller screws, actuators. No additional Capex would be required for this.

I’ve written a DETAILED article on MTAR – Betting on Space [Part 2]: Centum Electronics and MTAR Technologies

Disclosure – Tracking, not invested. Waiting to see defence / space revenue drivers to kick in.

NMDC-Value or Cyclical? (21-01-2024)

Any idea, what was the issue? The article just says, unethical behaviour.

Hitesh portfolio (21-01-2024)

And the way things are, in all probability, there would be political stability and continuity at the centre even after general elections. – Neeraj Kumar, Group CEO and

Whole Time Director – Jindal Saw Concall

Smallcap momentum portfolio (21-01-2024)

It depends on the methodology, the parameters, the system etc. While one can look at single stock’s performance, looking at the whole group over a period of time will give a better picture. It is about designing a system that performs, which consists of a group of stocks, whose selection is based on certain criteria, one of them could be allocation as per certain parameters.

Not invested in any smallcase currently, interested and learning about such systems.

52 week highs and all time highs strategy (21-01-2024)

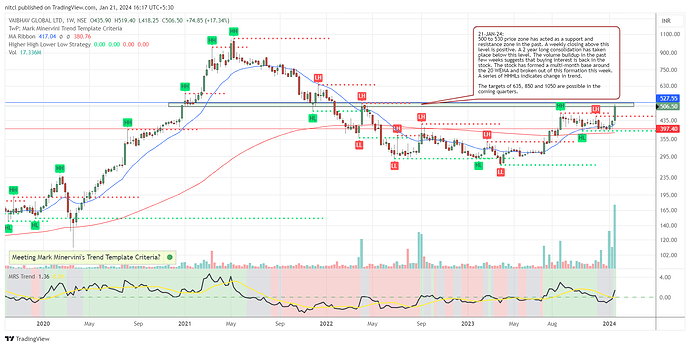

Vaibhav Global – Looking good after this week’s price movement.

- Stock is on the verge of a 2 year long consolidation break out.

- Volume build up in the past few weeks is encouraging and suggests that buying interest is back in the stock

- The price has formed a nice base near the 20 WEMA since Aug, 2023. It broke out of this base this week.

- The zone from 500 to 530 has acted as a multiple support and resistance zone in the past. A weekly close above this zone will be very positive.

- Indicators such as the Mansfeld Relative Strength and Minervini Trend Template are positive and suggest that the stock is in Stage 2 up trend. The runway to the previous ATH is long and provides possibility of decent returns in the coming quarters.

Disclaimer: Not invested yet. Planning to buy above 530.

The harsh portfolio! (21-01-2024)

I have made a few changes to the model portfolio which are summarized below. My thought process at this point is to reduce allocations to stocks trading at higher end of their valuation band, and also reduce allocation to very small cos, especially without any clear triggers. Market has been excessively rewarding, and in the past my major mistakes have come in these times. Lets see how many mistakes I make in this cycle.

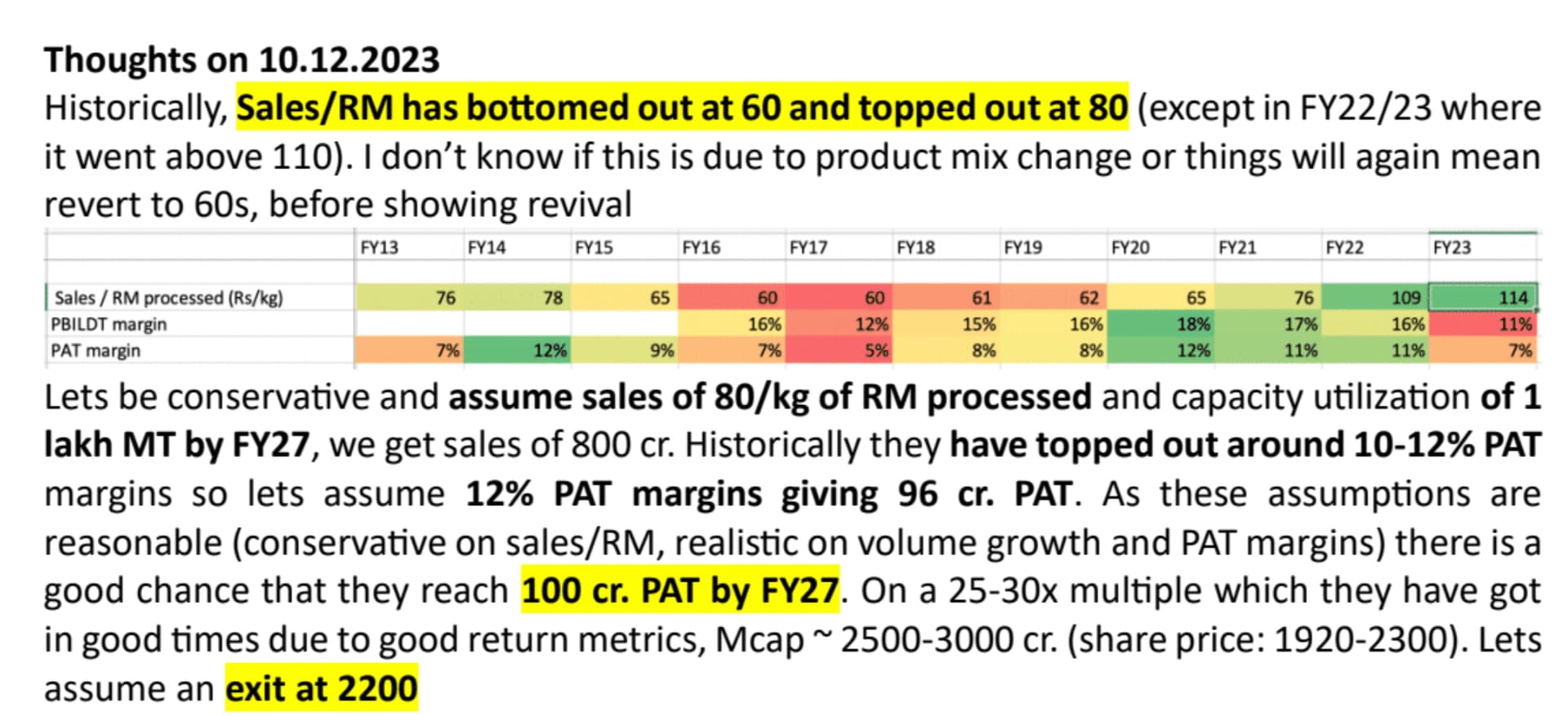

- Added 2% allocation in Fairchem Organics. I am looking to add chemical companies which have done capex, have good unit economics, and whose prices are down a lot. In Fairchem, logic is quite simple. Their new product (stearic and isostearic acids) are 2.5x realizations vs Dimer acid, has limited competition, and a large market size. Fairchem’s margins are at life lows. So there are two clear earning drivers (mean reversion in margins + new product growth). I feel they can reach 100 cr. PAT over the next 3-4 years. My detailed speculation around their future nos are below.

-

Added 2% allocation in Garware hi-tech. Garware’s VP thread is amazing to understand what differentiates them vs other packaging/polymer cos. Their PPF scaleup has been quite good and I feel if they can reach 2,500 cr. sales/ 500 cr. EBITDA by FY27, they will get atleast 10,000 cr. Mcap. I somehow missed buying it last year when their valuations fell to 10x, but I still feel there is good potential from current prices.

-

Increase allocation to Manappuram from 2% to 4%. I should have added to it when price had dipped below 100 but somehow failed to act. Business is clearly recovering and valuations are quite cheap. The Asirvaad IPO should also create some excitement around the stock. I feel its one of the best, yet one of the most misunderstood managements. Their capital allocation and scaleup since 2015 has been spectacular. @maheshkumar does an amazing job in sharing everything there is to know about the co.

-

Reduced allocation to Gufic biosciences, from 4% to 2%. Their stock price has moved up significantly in anticipation of growth from their large capex, as a result Mcap/sales is towards the higher side. I want to reduce my risks here.

-

Exited newspaper companies (DB Corp, Jagran). The idea of mean reversion in valuations is so simple, yet somehow unloved. Since I invested in 2021, DB Corp has returned 20% of my initial capital as dividends, and share price is close to 5x. Jagran has been a bit disappointing vs DB Corp, but it has been reasonable (7% dividend + 2x price). I am unwilling to pay 20x PE for slow growth newspaper cos like they are valued now. But single digit multiples on depressed earnings is something I am happy to bet on, especially because these companies are paying out earnings to shareholders.

-

Exited CV cycle plays (Ashok Leyland, Sundaram Finance). Both have been very rewarding but recent CV sales data suggests some slowdown and I am unwilling to go into a bad market with CV companies at their top.

I find that cyclical and value investing jells very well with my personality, its possible to make 3-5x by buying into a bad cycle and waiting for recovery. CV cycles are really predictable and one can make good returns by just betting on leaders during downcycles. E.g. I started buying Ashok Leyland in 2020 when its price had dipped below 50, since then it has been a decent journey.

Sundaram Finance is a CV lender with an amazing track record, and it got sold in 2022 and reached cyclical low multiples. One could see CV revival in monthly sales data, and it was a 2.5x in quick time, despite being a leader and being well followed. However, valuations now are closer to their upper end, thats why the exit.

Updated folio is below and cash stays low at 1%.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| Aegis Logistics Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| HDFC Bank Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Godfrey Phillips | 4.00% |

| P.E. Analytics Ltd | 4.00% |

| Gufic Biosciences | 2.00% |

| Ajanta Pharmaceuticals Ltd. | 2.00% |

| NESCO Ltd. | 2.00% |

| I T C Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| Aptus Value Housing Finance India Ltd. | 2.00% |

| Shree Ganesh Remedies Ltd – PP | 2.00% |

| Garware Hi Tech Films Ltd | 2.00% |

Cyclical (45%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Manappuram Finance Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 2.00% |

| Stylam Industries Limited | 2.00% |

| Ashiana Housing Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| ANUH PHARMA LTD. | 2.00% |

| Dharmaj Crop Guard Ltd | 2.00% |

| MAYUR UNIQUOTERS LTD. | 2.00% |

| Godrej Agrovet Ltd. | 2.00% |

| Chaman Lal Setia Exp | 2.00% |

| Fairchem Organics Ltd | 2.00% |

| KSE LTD. | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (8%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 2.00% |

| Worth Peripherals Ltd | 2.00% |

| Sharat Industries | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| RKEC Projects | 1.00% |

Its called Pareto chart, you can find it on excel.

No idea, sorry these are too complicated concepts for me.

Dont know how to think about these things. Promoter selling in isolation doesn’t provide any insights.

There is a lot of buzz that finally the battle will settle this year. For the kind of nos they are reporting, current prices are capturing a lot of downside already. But I dont know how to think of it, its been going on since 2019.

Cyient – Exposure to ITeS minus commoditized body shopping (21-01-2024)

This is further to our disclosures made on 2 May 2023 and 21 April 2022.

In relation to the associated civil class action antitrust lawsuit filed by plaintiffs in a U.S District Court, we wish to inform you that Cyient Limited’s US Subsidiary, Cyient Inc. has entered into an agreement dated20 January 2024 to settle, and dismiss with prejudice, the said civil class action antitrust lawsuit for an amount of US$7.4 million. Cyient Inc. will utilize the insurance amounts available to it towards payment of the aforesaid settlement amount.

The settlement is without admission of any liability and the plaintiffs have agreed to release and discharge all claims associated with this lawsuit against Cyient Inc. and its affiliates. The settlement is subject to approval by the presiding judge and the timing of this process is at the discretion of the court.

May I request the expert tracking this business can throw some light on the above please