Sorry… I did not understand ur question ![]()

![]()

Can u please simplify it for me

Sorry… I did not understand ur question ![]()

![]()

Can u please simplify it for me

Rallis India –

Notes from AR – 2022-23 –

Rallis India ( a TATA group company ) is one of the leading domestic agrochemicals company operating in the agrochemicals and seeds markets

Company has a branded domestic agrochemicals business selling herbicides, insecticides and fungicides. Company exports AIs ( technicals ) and is also engaged in contract manufacturing. Also makes – bio-fertilizers, Biopesticides, water soluble fertilisers for the domestic mkts

Seeds business – caters to field crops like paddy, maize, millets, cotton, wheat. Also caters to vegetables like – Chilli, Okara, Tomatoes, Gourds and Watermelons

Has a total of 05 manufacturing facilities – 03 in Gujarat, 02 in Maharashtra. Also has 02 R&D centers in Bengaluru

Product wise revenue break up –

Agrochemicals – 88 pc

Seeds – 12 pc

Geography wise revenue split –

Domestic – 63 pc

Exports – 37 pc

India is a major agrochemicals exporter and has been attracting global majors as they try and diversify their supply chains out of China. Rallis has been expanding its manufacturing footprint to encash such opportunities

Indian agri-exports topped 4 lakh cr in FY 22-23. With greater penetration of scientific agriculture, these figures can ramp up significantly. This is also a great opportunity for the agri-input providers

FY 23 outcomes –

Sales – 2967 vs 2604 cr

EBITDA – 221 vs 281 cr ( margins @ 7 vs 11 pc )

PAT – 92 vs 164 cr

FY23 profitability was adversely impacted by –

Impairment of intangible assets ( technical knowhow ) amounting to 31 cr wrt seeds development technology

Re-assesment of future sales potential resulted in company making provisions of Rs 53 cr wrt the slow moving seeds inventory

Company’s manufacturing capital –

14 AIs ( or technicals )

14 Formulations

77 pc capacity utilisation

Volumes sold –

9.1 k MT of herbicides

8.1 k MT of fungicides

12.6 k MT of insecticides

13.3 k MT of seeds

0.9 k MT of crop nutrients and other products

Disc : not holding, not SEBI registered

Not just DBJ but also the acquisition of Acemoney – banks of the likes of HDFC bank are losing retail deposits and increasing cost of funds.

Even though plenty of cashless transactions are being done daily and likely to increase further which can be negative for the company, but their onboarding of DJB business will be a masterstroke, because this segment has hardly any cashless transaction! Cash rule the Diamond Jewlery, Bullion segment.

Portfolio Benchmarking to discover your true opportunity cost.

An ideal option is to compare with the leading PMS’ with consistent long term compounding, who match your investment style and gestation. Your true opportunity cost lies there as you are unlikely to simply pick a Nifty index fund/ETF if not investing on your own.

As discussed on another thread,

I use an average returns index from the 3 funds

SageOne Small Cap

SEBI | Portfolio Manager Monthly Report

PMS: Sageone Investment Managers LLP

@aveekmitra’s Aveksat Equity

Aveksat Financial Advisory

@ayushmit’s Mittal Analytics

https://www.sebi.gov.in/sebiweb/other/OtherAction.do?doPmr=yes

PMS: Mittal Analytics Private Limited

Since many have requested for sources to track these, I am providing the links here as well.

3Q FY24 Few good Points in below article

Paytm’s parent company One97 Communications expects wealth management through futures and options (F&O) and equity trading to become a big part of financial services distribution revenue in the next 12-18 months, its president and chief operating officer Bhavesh Gupta told analysts on Saturday.

Read more at:

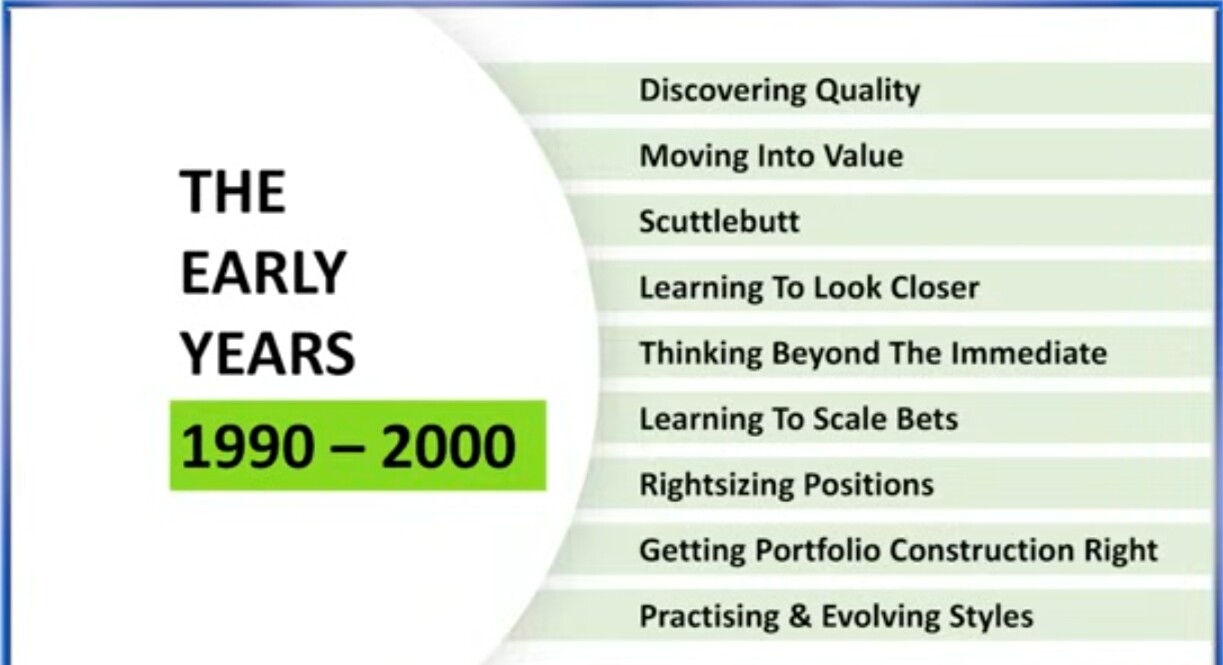

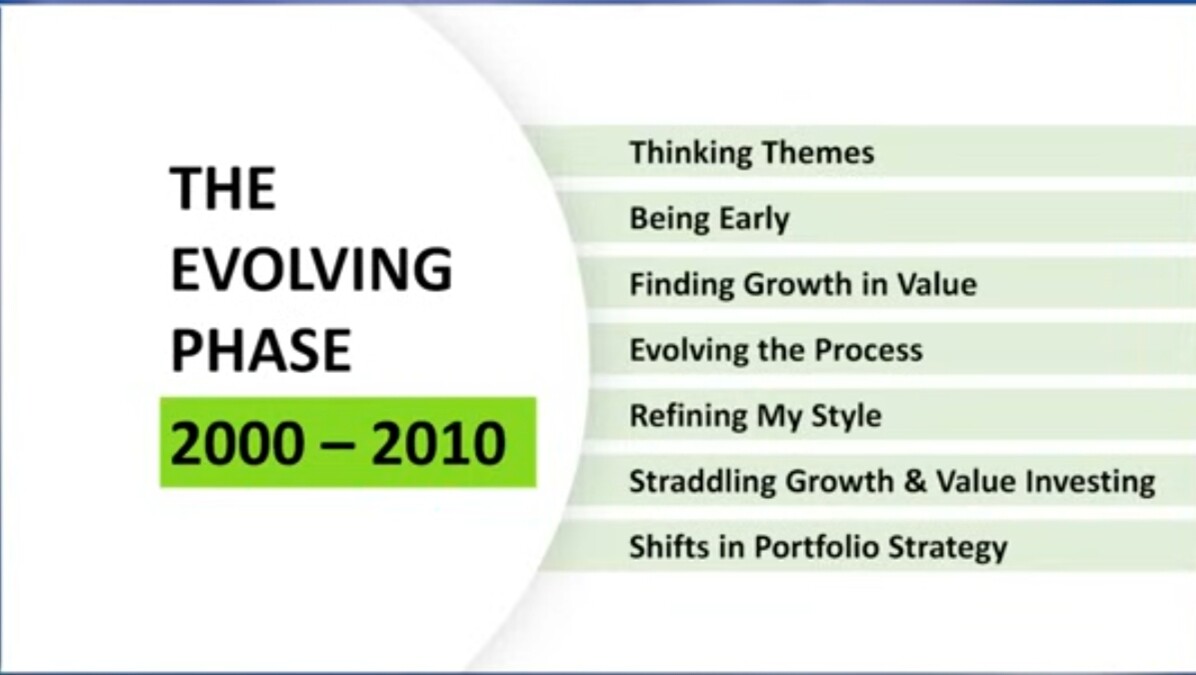

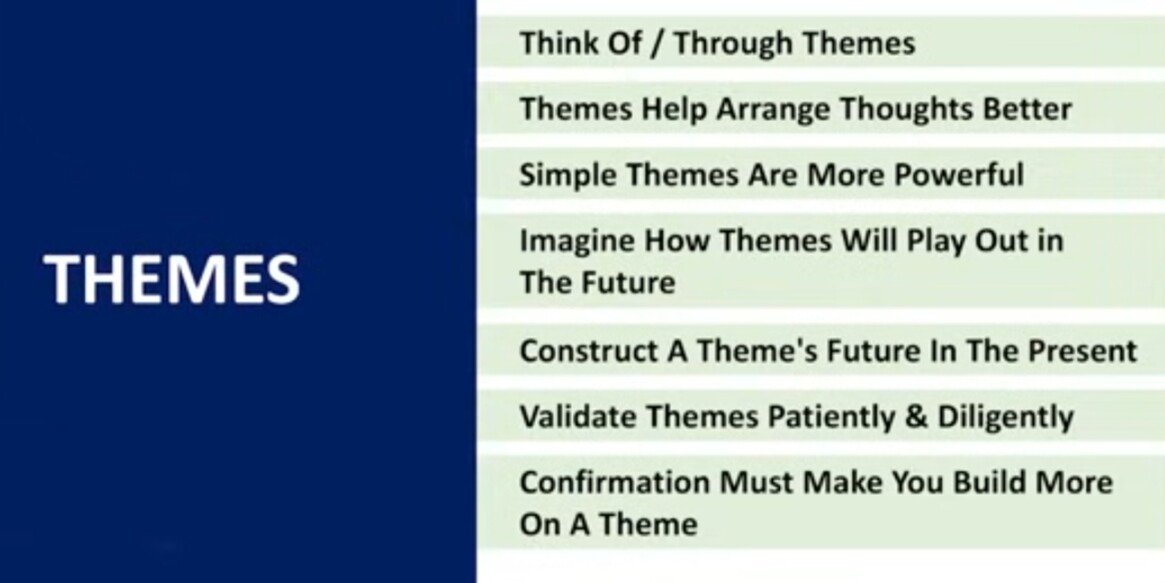

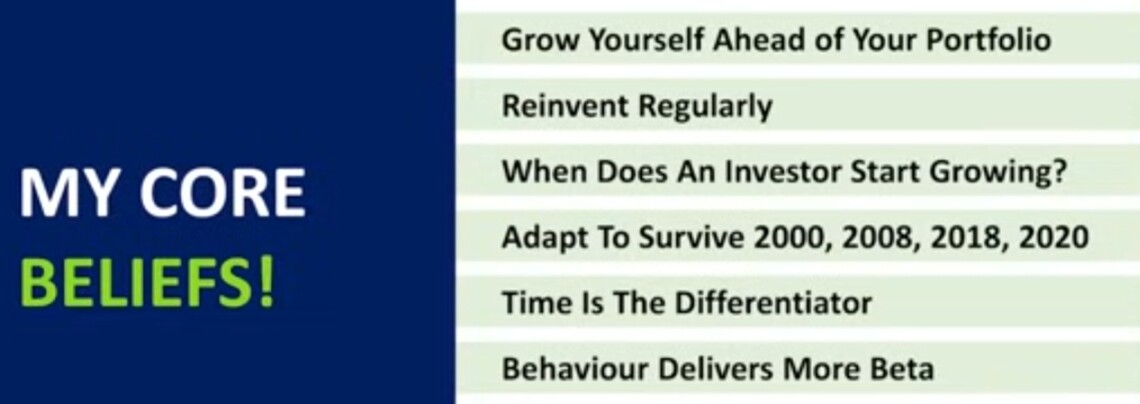

A great session from Shyam Sekhar on learning from the past cycles and over his 33 years of Investing in Indian Equities (1990-2023)

#VIPS 2023 – LEARNINGS FROM THE CYCLES | SHYAM SEKHAR |

Key lessons from past 3 decades

Key patterns to avoid during bull market

Key themes to look into:

Grow yourself ahead of the portfolio

Absolutely Agree with you results were quite bad last quarter. I hope they perform this quarter much better. And I Do See Almost Everyday people wearing campus shoes. in gyms, gardens and i have gone out to ask people about the product and have received positive reviews from many. Although i still also know that most of the people still do not know about the brand.

Disc: Invested

Note: This is not a buy/sell recommendation.