One of the portfolio threads i consistently read.

If you dont mind answering, how do you crop as whatever happens a single stock doesn’t impact portfolio to much extent. Same on adding a stock.

One of the portfolio threads i consistently read.

If you dont mind answering, how do you crop as whatever happens a single stock doesn’t impact portfolio to much extent. Same on adding a stock.

Can you please explain, you put 20+ documents of conf calls, what prompt you gave & how it performed?

Look at these shares and and number of shareholders you will see massive delta between 2022-23 and today.

But in agreement on massive divergence between stock move and fundamental results. Is manipulation probable. Maybe. It is more of Retail Fomo. I beleive in next two years it will diverge again to the downside.

Large part of India is humid and as such coolers don’t work well. Secondly, air conditioners have become cheaper over time. Thirdly, the competition is fierce in the cooler space and customers are more price conscious.

It is difficult to make a case for large sustained growth in the segment by any company in India.

Indusind’s QoQ PAT is in growth trajectory with consistent tax rate.

I think the main point with PSU rally is operational improvements and increased Profits… like NPA cleanup in banks have led to increased profit … same case with management changes in other psu’s… have created the rally… so now the question is until when it will go on ![]() … i think the profits increasing is good thing … the issue comes with top line growth… psu’s will have very minimal top line/revenue growth compared private ones… and if profits are appropriate, prices will sustain but wont rally further if top line is not growing… thats the time to sell or take out initial investment atleast and leave the rest for dividend

… i think the profits increasing is good thing … the issue comes with top line growth… psu’s will have very minimal top line/revenue growth compared private ones… and if profits are appropriate, prices will sustain but wont rally further if top line is not growing… thats the time to sell or take out initial investment atleast and leave the rest for dividend ![]() …

…

Watch out small space satelites and radar space

This market is going to expand and companies like avantel if they get 150cr order , its more than sufficient for them to grow at decent rate

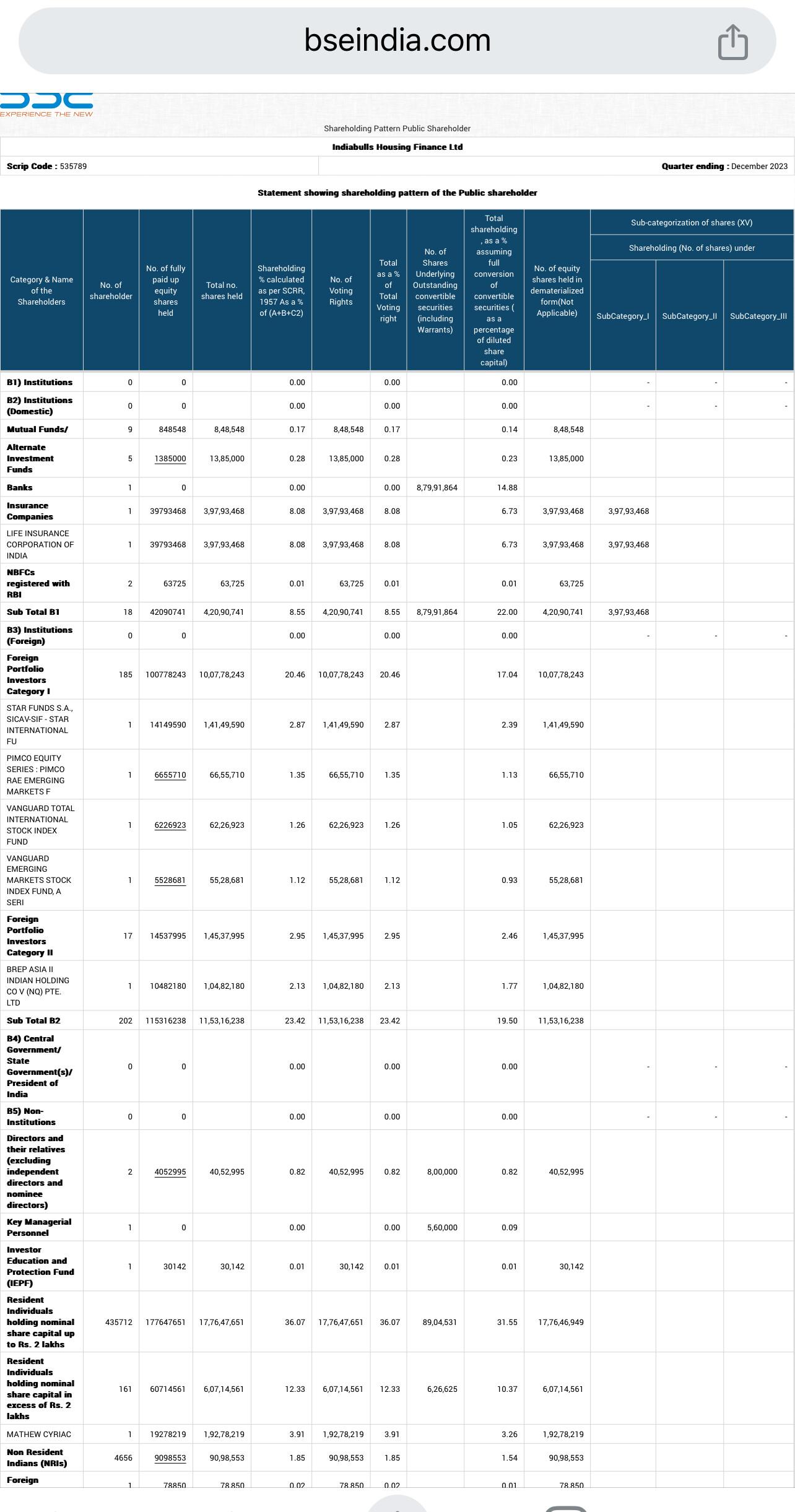

Mathew Cyriac raised his stake from 1% to 3.91% in this stock as per December Shareholding pattern update.

Hi, valid point.

Yes, pyrolysis process is simple enough in theory.

The company has done a lot of experiments, and done trial and errors with several permutations and combinations to arrive at the optimum reactor settings (which includes differential temperatures in different zones of the rotary kiln, differential horizontal velocity as the tyre passes through the reactor and gets decomposed, and the rotation speed of the kiln) so as to give the highest quality output depending on the quality and chemical composition of the waste tyres. Which differs by geography (tyres from USA for eg, have lesser silica content than European tyres), quality for CV, PV and other tyres are different etc.

The company started with lab scale input and then progressed to commercial scale at lower capacities starting from 1kg and moving higher till they reached 100 tpd capacity. At each stage, the plant and machinery underwent several modifications which was made possible because their own group company was manufacturing it.

One can search on Youtube for batch pyrolysis plants (eg. https://www.youtube.com/watch?v=pvbfOQHlP50) to realise how energy intensive and inefficient such process is. So there is no comparison of continuous process with batch process.

Within continuous process, the edge of the company is the above efforts they have taken and their own in house manufactured machines which have been designed to produce high quality rCB (recovered carbon black) most economically.

I have been adding on dips.

Don’t know the status of HNG acquisition.

Portfolio is down by 15%

Looks like catching a falling Knife.

I don’t see this HNG drama settling soon.

Does anyone think there is a chance that it might not go in AGI’s favor?