So the takeover overhang is gone for now.

Posts tagged Value Pickr

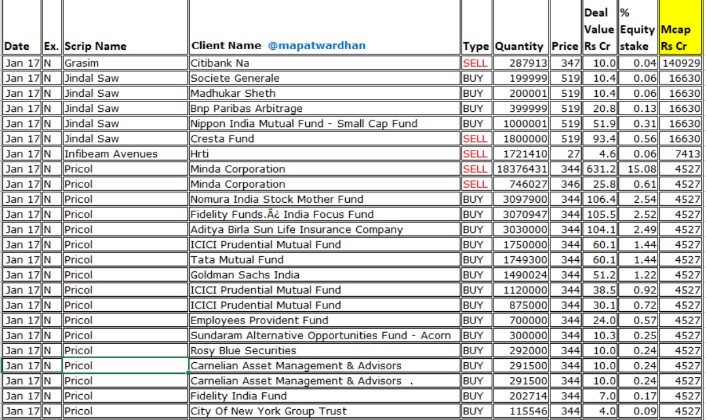

Pricol limited – OEM automotive (17-01-2024)

Exchange filing from Minda corporation

43ca032f-b264-4495-ad33-b214f3b61a1e.pdf (183.2 KB)

Stake sell details:

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (17-01-2024)

NFCSF CRUSHING REPORT AS ON 15012024.pdf (52.6 KB)

NFCSF report

Happiest Minds Technology (17-01-2024)

Recent Result Update (Q3 FY24):

Revenue Up YoY so does the expense…!

Margin getting a hit…!

Almost a Flat result…!

Ramit’s Portfolio (17-01-2024)

Hello everyone,

I started my equity investing journey in July 2023 with the goal of generating a long-term return of 20% or more. While I have previously invested in equity through ELSS mutual funds primarily for tax savings, I believed that, as an individual, I could have more flexibility in investing and potentially generate higher returns compared to mutual funds. Recently, my churn rate has been high, possibly as a result of a steep learning curve.

My filtering process is based on the following model:

- Margin Expansion due to company expanding into value added product

- Operating leverage playing out

- Develeraging thus lightening of balance sheet

- Product mix change i.e. increase in higher margin business

Exit Framework that I am currently following:

- Volatility based indicator showing exit

- Key Thesis Breaks

- Better opportunity available

Current Portfolio

| Instrument | Allocation |

|---|---|

| ARMANFIN | 10.31% |

| EQUITASBNK | 2.24% |

| GOODLUCK | 6.64% |

| ICIL | 3.82% |

| JSL | 3.09% |

| GMMPFAUDLR | 2.47% |

| MARATHON | 2.18% |

| NIFTYBEES | 37.82% |

| NUVAMA | 5.58% |

| PRICOLLTD | 4.10% |

| SENCO | 9.09% |

| SKIPPER | 4.37% |

| PENIND | 2.11% |

| SOUTHBANK | 6.19% |

Currently, the highest allocation is to NiftyBees. The goal now is to find more businesses that fit into my framework, thereby reducing my allocation to NiftyBees. If I am unable to identify any opportunities with a good MoS, I tend to transfer my funds into a Liquid Fund. This helps me to maintain sufficient cash when the opportunity arises.

This thread serves a double purpose: seeking feedback for process improvement, and documenting my decisions as an investment journal, both enhancing self-awareness and refining decision-making processes.

Disclaimer: The content provided here is not investment advice. It reflects solely my personal opinions, and I could very well be wrong about any of them. Before making any investment decisions, it is advisable to consult with your financial advisors.

Federal Bank – A Turnaround banking Story? (17-01-2024)

Federal bank is aggressively expanding its credit card business and have recently been the best credit card in terms of throwing offers at premium channels including Lifestyle, Amazon, MMT, Yatra…. Good times ahead it seems?

Megamind portfolio (17-01-2024)

January 2024

Infy

Tcs

Bajaj finance

HDFC Bank

Asian paints

Titan

Fine organic

Balkrishna industries

Sbi cards

Vedant fashion

Will continue to add more

A fix amount in each stock

Pricol limited – OEM automotive (17-01-2024)

Minda Corp sells 15.7% stake in pricol at 343.60 shares (1.91 crore shares)

News source – internet

Invested

Federal Bank – A Turnaround banking Story? (17-01-2024)

Federal Bank –

Q3 FY 24 Updates –

Deposits – 2.39 lakh cr, up 19 pc

Advances – 1.99 lakh cr, up 18 pc

Gross NPAs – 2.29 vs 2.43 pc

Net NPAs – 0.64 vs 0.73 pc

PCR @ 71 vs 69 pc

Total branches @ 1418, added 65 branches in FY 24

Cost/Income @ 51.9 vs 48.9

Yield on advances @ 9.37 vs 8.78 pc

Cost of funds @ 5.81 vs 4.71 pc

NIMs @ 3.19 vs 3.55 pc

RoA @ 1.39 vs 1.33 pc

RoE @ 14.80 vs 15.91 pc

Profit and Loss parameters ( standalone ) –

NII – 2123 vs 1957 cr, up 9 pc

Fee Income – 642 vs 543 cr, up 18 pc

Operating profit – 1437 vs 1274 pc, up 13 pc

Provisions – 431 vs 471 cr

Net Profit – 1007 vs 804 cr, up 25 pc

Segment wise growth in advances –

Retail – 65k cr, up 20 pc

Agri – 25.1 k cr, up 27 pc

Business banking – 15.97 k cr, up 18 pc

CV / CE – 2.7 k cr, up 66 pc

MFI – 2.3 k cr, up 160 pc

Commercial banking – 20.7 k cr, up 26 pc

Corporate banking – 71.9 k cr, up 14 pc

High margin products for the bank include – CV/CE, Personal, Credit Cards, Micro Fin and MSME loans – this cohort now forms 24 pc of Bank’s book vs 21 pc LY

Slippages for Q3 @ 480 cr ( within limits )

CASA + Deposits < 2 cr @ 81 pc of total deposits vs 88 pc LY

One of the large accounts worth 70 cr slipped in Q3 due factory fire at client’s factory. Likely to become standard in Q4

Bank is carrying 20 pc provisions on the restructured book. Current size of restructured book at 2200 cr

Aim to take the unsecured book to 10 pc of the total book from aprox 5 pc at present

Bank holding onto its advances growth guidance of 18-19 pc for FY 24. Aim to maintain the deposits growth rates in a similar band

Capital market investments / SIPs etc are also increasingly competing with banks for saving deposits. People are becoming more tech savvy and are managing their saving accounts more actively. Term deposits are relatively insulated

41 branches out of 75 opened LY have turned positive. Bank is very particular about location while opening a new branch

Disc: holding, biased, not SEBI registered

Ranvir’s Portfolio (17-01-2024)

Federal Bank –

Q3 FY 24 Updates –

Deposits – 2.39 lakh cr, up 19 pc

Advances – 1.99 lakh cr, up 18 pc

Gross NPAs – 2.29 vs 2.43 pc

Net NPAs – 0.64 vs 0.73 pc

PCR @ 71 vs 69 pc

Total branches @ 1418, added 65 branches in FY 24

Cost/Income @ 51.9 vs 48.9

Yield on advances @ 9.37 vs 8.78 pc

Cost of funds @ 5.81 vs 4.71 pc

NIMs @ 3.19 vs 3.55 pc

RoA @ 1.39 vs 1.33 pc

RoE @ 14.80 vs 15.91 pc

Profit and Loss parameters ( standalone ) –

NII – 2123 vs 1957 cr, up 9 pc

Fee Income – 642 vs 543 cr, up 18 pc

Operating profit – 1437 vs 1274 pc, up 13 pc

Provisions – 431 vs 471 cr

Net Profit – 1007 vs 804 cr, up 25 pc

Segment wise growth in advances –

Retail – 65k cr, up 20 pc

Agri – 25.1 k cr, up 27 pc

Business banking – 15.97 k cr, up 18 pc

CV / CE – 2.7 k cr, up 66 pc

MFI – 2.3 k cr, up 160 pc

Commercial banking – 20.7 k cr, up 26 pc

Corporate banking – 71.9 k cr, up 14 pc

High margin products for the bank include – CV/CE, Personal, Credit Cards, Micro Fin and MSME loans – this cohort now forms 24 pc of Bank’s book vs 21 pc LY

Slippages for Q3 @ 480 cr ( within limits )

CASA + Deposits < 2 cr @ 81 pc of total deposits vs 88 pc LY

One of the large accounts worth 70 cr slipped in Q3 due factory fire at client’s factory. Likely to become standard in Q4

Bank is carrying 20 pc provisions on the restructured book. Current size of restructured book at 2200 cr

Aim to take the unsecured book to 10 pc of the total book from aprox 5 pc at present

Bank holding onto its advances growth guidance of 18-19 pc for FY 24. Aim to maintain the deposits growth rates in a similar band

Capital market investments / SIPs etc are also increasingly competing with banks for saving deposits. People are becoming more tech savvy and are managing their saving accounts more actively. Term deposits are relatively insulated

41 branches out of 75 opened LY have turned positive. Bank is very particular about location while opening a new branch

Disc: holding, biased, not SEBI registered