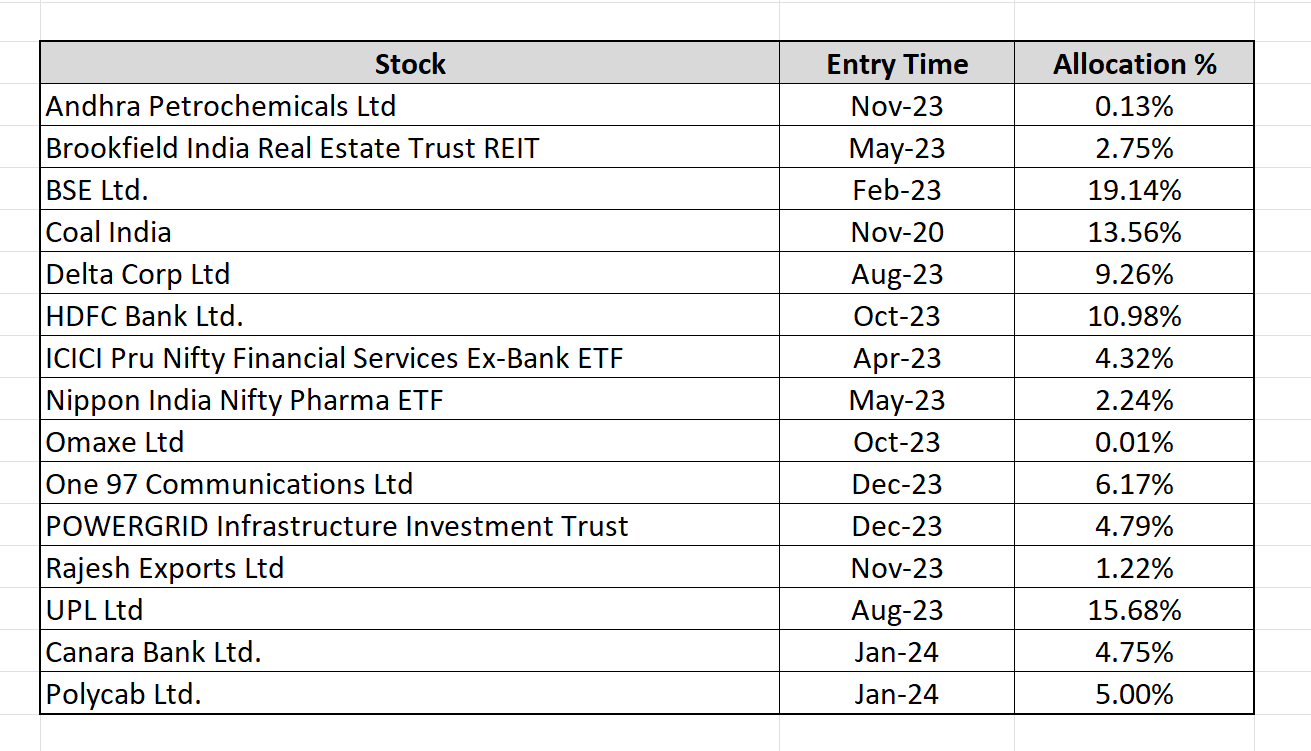

I would like to provide you with a comprehensive overview of the current state of my portfolio as of today. The following details the allocation of my portfolio holdings:

I would like to provide you with a comprehensive overview of the current state of my portfolio as of today. The following details the allocation of my portfolio holdings:

Can you elaborate on ur thesis for LTTS ?

Sumitomo Chemicals India Ltd –

A leading agrochemicals company in India

Current number of manufacturing facilities @ 05 in Maharashtra, Gujarat

Manufacturing 15 Active Ingredients, 200 + brands. Company has 15000 + direct distributors and 60 Depots. Employee strength at 1600 + over 1500 + field development officers ( contractual )

R&D team comprises of 75+ dedicated engineers, 10 + Phd’s with experience > 15 yrs

Product wise revenue break up –

Insecticides – 40 pc

Herbicides – 30 pc

Plant growth regulators – 10 pc

Fungicides – 7 pc

Metal Phosphides ( used as fumigants against insects and rodents in stored grains ) – 7 pc

Animal nutrition – 6 pc

Geography wise revenue break up –

India – 89 pc

Exports – 11 pc

Breakdown of domestic sales –

Branded – 82 pc

Bulk – 18 pc

Breakdown of export sales –

Branded – 39 pc

Bulk – 61 pc

Future capex plans –

Regular maintenance capex @ 70-75 cr / yr

Additional capex of Rs 120 cr over 2 yrs for 05 new products ( Active Ingredients / Technicals ). These AIs shall be supplied to the parent SCC, Japan. These products have a revenue potential of 200-250 cr / yr at present. These products are also reporting healthy growth rates across the world

Company is focussing on manufacture of additional off patent products for India, LATAM, Africa and Asia pacific. This will entail additional capex and the same is under consideration

Last 5 yrs –

Revenue CAGR @ 13 pc

EBITDA CAGR @ 25 pc

PAT CAGR @ 28 pc

Company enjoys great parentage. Has access to parent’s global supply chain, R&D

Q2, FY 24 highlights –

Weaker monsoon in June, Aug affected the demand for agrochemicals. El-Nino also played a spoilsport

Revenues – 903 vs 1122 cr

EBITDA – 188 vs 278 cr, Margins @ 21 vs 25 pc – margin drop primarily led by operating de-leverage. High cost inventory also had an impact

Net Profit – 144 vs 202 cr

Export sales adversely affected due to channel overstocking due aggressive dumping of generic products by Chinese players in preceding 6-9 months

Company has consumed all the high cost inventory and is now back to normal. This should help profitability in q3, q4

Working capital cycle shrunk to 70 days from 91 days in Q2 FY 23. Company has seen improved collections vs previous years thus maintaining better sale hygiene

Launched 06 new products in Q1, Q2

Company’s new launches ( in speciality segment ) in last 1-2 yrs have been received very well in the Mkt. Consumers response has been overwhelming. Its just that due to the unfavourable mkt conditions this yr, the same could not translate into better sales / financial outcomes

Due to exhaustion of high cost inventory and general drop in RM prices, margins are expected to see some recovery wef Q3

Global demand scenario for agrochemicals Industry looks better for H2 vs H1

Long term Capex guidance @ 15 pc of EBITDA / yr

Company’s animal nutrition business is in nascent stages right now. Is growth fast on a small base. Can be a significant growth driver going forward

Business de-growth in H1 has been 15 pc. 3 pc has been due to price, rest due to volumes de-growth

Don’t see high channel inventory related problems in Q3, Q4 wrt Domestic Mkts. However, the situation is still not normal in the International Mkts. Normalcy in global mkts may resume only after Q4 / Q1 FY 25

There is no problem wrt demand for agrochemicals in the export Mkts. The whole issue is about overstocking in the channel and steep cuts in the prices of the inventories held. Its across the board / across companies kind of phenomenon

Company is virtually debt free. Cash on books > 1400 cr. Looking out for small / bolt on kind of acquisitions

Company expected to spend 200-300 cr towards fresh capex at Dehej wef FY 25 , for next 2-3 yrs

Have launched a new plant growth regulator for Apple in India. Rapidly gaining market share

Avg margin losses due high cost inventory in Q1 was around 12 pc and around 5-6 pc in Q2. In Q3, the margin loss is expected to be around 1-2 pc

Disc: not holding, may buy in future, not SEBI registered

Hi. How is this heavy promoter selling?

Can you share in percentage terms how many shares have been sold by the employees and promoters? In absolute terms the amount seems small.

And also all of the selling in the screenshot has been done by employees and not promoters. Your thoughts?

I did watch it on Friday. Overall occupancy was around 20%(morning show). It was released without much publicity compared to other big tamil( captain miller) and telugu( gunturu kaaram) movies released on the same day for Sankranthi. First half was impressive but second half turns out to be average. Overall I think it is getting getting good word of mouth publicity reflecting in better occupancy over weekend. If we look at the no of ticket sold it is at par with other tamil movie like captain miller.

Phantom has done good work with VFX effects in the movie.

Looks like movie will be released in Hindi in near future.

Disclosure: Invested

Happy New Year to you too …

Most of the recent buys are in the previous post …

Amara Raja,HLE glasscoat , Sona Comstar are good companies trading at lower valuations than they usually did .Good businesses with upcoming revenue boost due to capex or aquistions soon.

MSTC … read the article by fundoo professor . The first auction thingy is reason enough .

Other than those bought …

Wockhardt … read its threads in VP . Seemed good times are ahead.1% of portfolio …so not much to lose anyway .Thinking of increasing but it has run up a bit since I bought .

Danlaw Tech … Makes TCU’s .Verified creds in linkedin and by articles in tata elxsi site . Good results in past 4 quarters .Again. 1.2% only.

Valiant Communication … very small company but with good hi tech product for network security and grid security . Already sales to US and european gov organizations and is the only approved vendor for Power grid security in India. 1% allocation.

These three are risky but hoping for high rewards if it works out .

Almost all are trading higher than where I bought except HLE .I am not a scuttlebutt guy so there might be bad things I missed or ignored about these .Please do not curse me later if you buy any of these and lose money .

![]()

I started buying ~120-130 in smaller chunks. But suddenly went upto ~220, so not adding now. I’ll wait for this to correct for fresh buy. This is by long term micro cap bet, no path to profitability atleast for next 3-4 years until all capex is done. All my other investments are in stable ones, so ok to take this bet. I dont have good stock picking skills , so doing direct investments either during heavy correction or fmcg/companies having business that any layman can understand.

Yes you first need to create your particular screen and save it. It will appear in your profile under ‘custom ratios’. Once that’s done you can go to watchlist view and click on edit columns (it will be under user ratios) to insert your screen that you just saved.

Tarachand infra logistics CMP-175 ( 14/jan / 24) MKT CAP – 248 crore P/E -21 Promoter holding – 73.3%

![]() It serves India’s infrastructural & industrial

It serves India’s infrastructural & industrial

needs through Warehousing,

Transportation, Equipment Rental, &

Turnkey Infra-Project Execution. With 35+

years’ experience, we’re a top Steel

Warehousing & Transport entity, handling

10M+ tons of Steel annually.

![]() Our fleet of 300

Our fleet of 300

Machines includes Heavy Cranes (up to

800MT), Hydraulic Piling Rigs, Steel

Processing, & Concrete Equipment. We’ve

contributed significantly to High-Speed

Bullet Train & Metro Line projects across

cities like Ahmedabad, Delhi, Mumbai,&

more

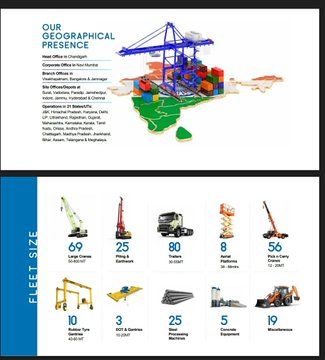

![]() Our team of experts & modern

Our team of experts & modern

equipment serve sectors like Power, Oil &

Gas, Renewable Energy, & Urban & Rural

Infrastructure. We cater to 52 diverse

customers, spanning PSUs to Indian

multinationals, operating in 21 states &

even internationally in Mauritius.

![]() Our capable team of 627 members, plus 300 contract workers, manage operations across 50+ cities Sectoral service offering Railway infrastructure Oil & gas Power Road & highway Cement.

Our capable team of 627 members, plus 300 contract workers, manage operations across 50+ cities Sectoral service offering Railway infrastructure Oil & gas Power Road & highway Cement.

![]() Growth strategy

Growth strategy

Focus on acquisition of large tonnage cranes & higher capacity pillingrigs & aerial platform,cont capacity addition, cont pursuing opportunities to take up EPC projects, civil & mechanical construction of building

![]() Birds eye views insight One of the largest steel logistics services provider in the country with handling of 9.45 million tonness fy 22-23, Introduce first of its kind ZOOMLION ZCC5800(500MT),crwaler crane with highest configuration of 84+84 with superlift Derrick

Birds eye views insight One of the largest steel logistics services provider in the country with handling of 9.45 million tonness fy 22-23, Introduce first of its kind ZOOMLION ZCC5800(500MT),crwaler crane with highest configuration of 84+84 with superlift Derrick

![]() Expanded steel logistics vertical with addition of nagpur stockyard under 7 year contract with rashtriya ispat nigam ltd

Expanded steel logistics vertical with addition of nagpur stockyard under 7 year contract with rashtriya ispat nigam ltd

expanded operations to the j&k, Assam ,Kerala Odisha

![]() Highest ever dispatch of 121 rakes steel by rail from central dispatch yard of vizag steel in march23( you can get idea also how steel demand is)

Highest ever dispatch of 121 rakes steel by rail from central dispatch yard of vizag steel in march23( you can get idea also how steel demand is)

![]() Leadership Mr Ajay Kumar is whole time director of tarachand, since inception,varoius client relationship & manages finance in his 30 years of experience, Himanshu Agrawal is excutive director &also currently chief financial officer,associated with company since 2017

Leadership Mr Ajay Kumar is whole time director of tarachand, since inception,varoius client relationship & manages finance in his 30 years of experience, Himanshu Agrawal is excutive director &also currently chief financial officer,associated with company since 2017

![]() Mr vinay kumar managing director,he also associated with company since inception ,he is pioneer in getting a number of innovative features implemented in material handling equipment,he is real driver behind the company for think new act now

Mr vinay kumar managing director,he also associated with company since inception ,he is pioneer in getting a number of innovative features implemented in material handling equipment,he is real driver behind the company for think new act now

![]() You can watch video of this giant https://youtu.be/1ryXQKm26lg?si=ZrFUCLfaYXblegXf… Another video of tarachand delivery https://youtube.com/watch?v=CFpnHeFdC1A&feature=shared…

You can watch video of this giant https://youtu.be/1ryXQKm26lg?si=ZrFUCLfaYXblegXf… Another video of tarachand delivery https://youtube.com/watch?v=CFpnHeFdC1A&feature=shared…

![]() Profit & loss

Profit & loss

OPM margin is v good

EPS growth is fantastic

![]() Recently company gives presentation at alpha ideas sme 2023

Recently company gives presentation at alpha ideas sme 2023

2023 Alpha Ideas SME Stars -Tara Chand Infralogistic Solutions Ltd

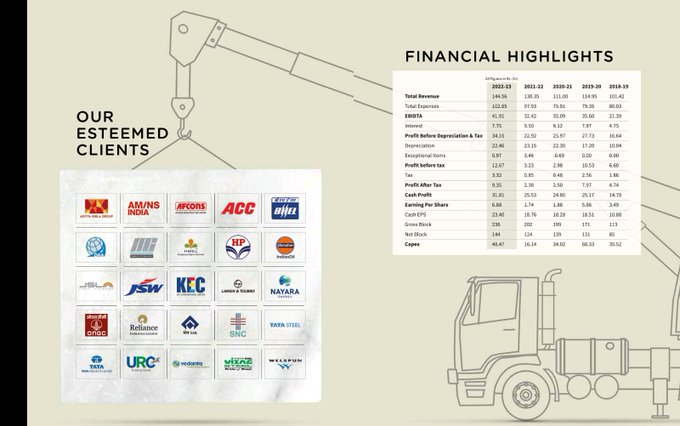

![]() Financial highlight and esteemed customer

Financial highlight and esteemed customer

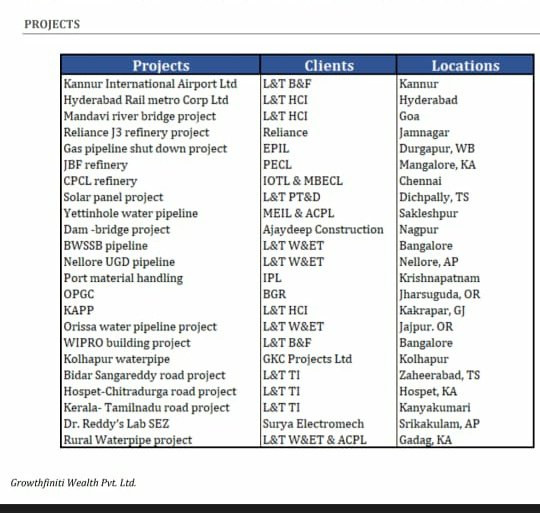

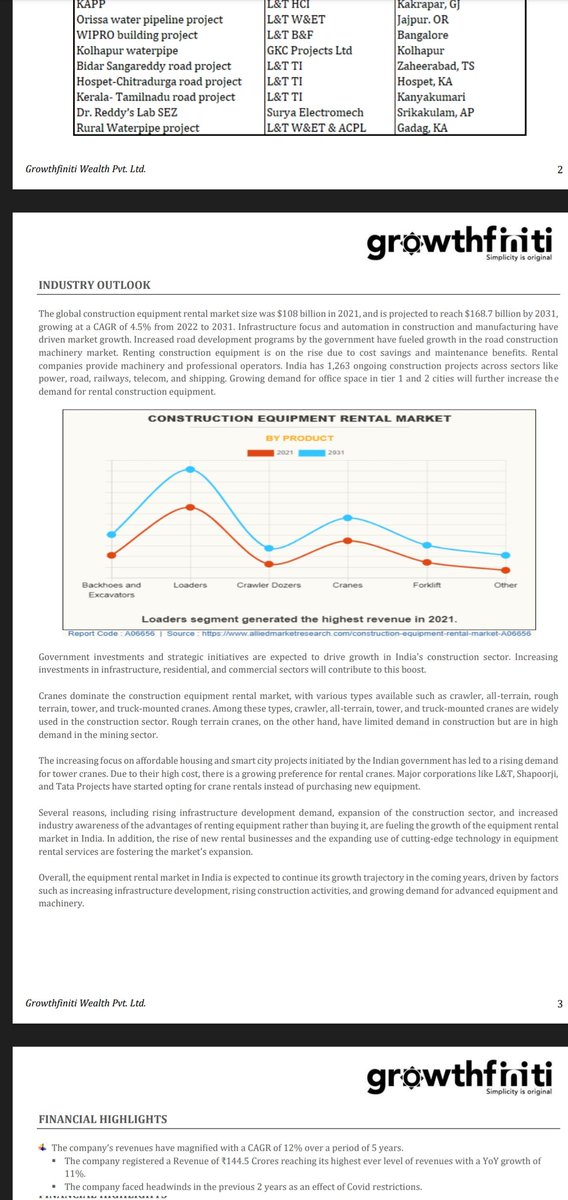

![]() Running project, client,& city, fleet size , geographical presence.

Running project, client,& city, fleet size , geographical presence.

![]() Industry outlook

Industry outlook

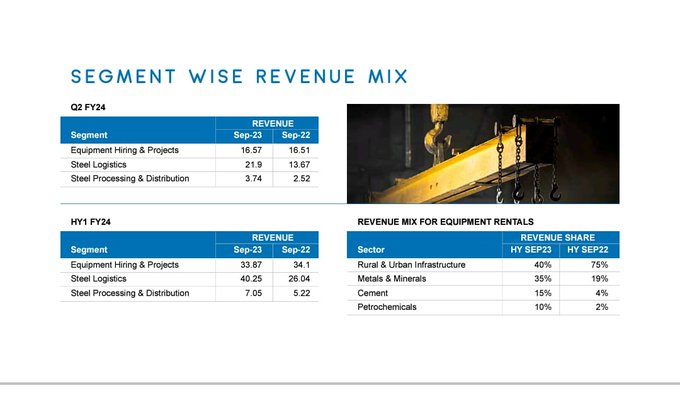

![]() Segment wise revenue mix

Segment wise revenue mix

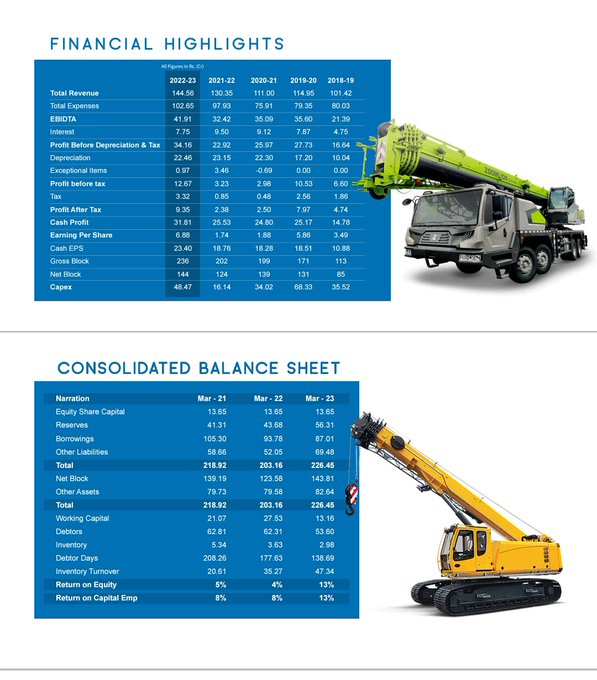

![]() Financial highlight with B/S

Financial highlight with B/S

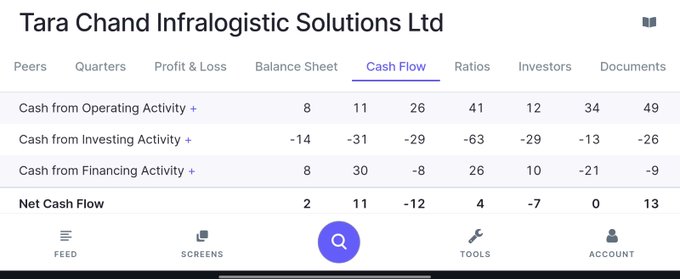

![]() Cash flow Is continuously increasing

Cash flow Is continuously increasing

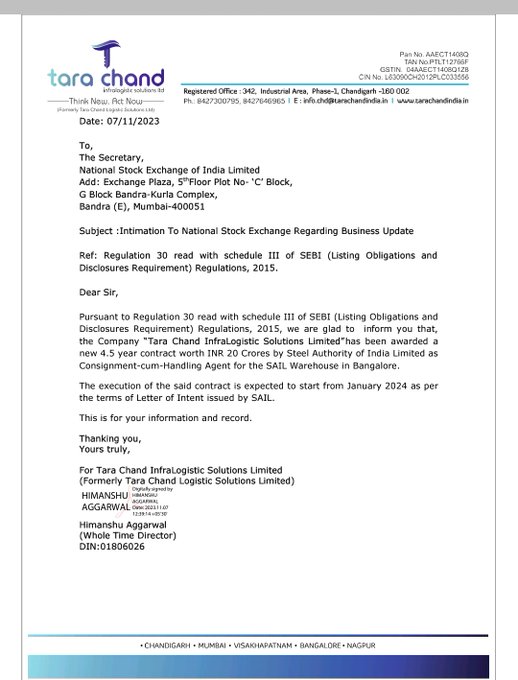

![]() Recently bag order from SAIL for 4.5 Years of 20 crore

Recently bag order from SAIL for 4.5 Years of 20 crore

![]() Peer comparison

Peer comparison

!Sanghvi mover is available at good valuation , good OPM ,

ACE construction

![]() Thesis If you bullish on infra capex than this type proxy can good play, heavy investment & construction , it’s at present fairly valued, first’ time concall

Thesis If you bullish on infra capex than this type proxy can good play, heavy investment & construction , it’s at present fairly valued, first’ time concall

![]() Anti thesis

Anti thesis

Demand of industrial production if someone down cycle comes it’s become heavy affected, other also some very good brands than tarachand can able to get to capture higher market share leading to loss, client concentrate L&T

![]() Disc I m not sebi registered

Disc I m not sebi registered

Pl consultant your financial advisor before investing,

No buy & sell reco,

Invested & biased

first investment at dec 23

no transcation last 15 days

Added Polycab to Portfolio 5%