At 1000 crore topline for 24-25 as per annual report its EPS can cross 30, with explosive growth PE can cross 100 so share price can cross 3000 Rs in a year and 6000 by 26 as management has aspiration to reach 2000 crore topline by 25-26. Already a mega multibagger and will create immense value ahead too

Posts tagged Value Pickr

Kamat Hotels (India) Ltd- A Possible Turnaround Story! (14-01-2024)

Management has delivered on growth promise by opening many properties, also have plan to reduce debt by half by q1 ,with this ESP for 24- 25 can cross 30 , will head to 4 digit in a year, hodling since lower levels and will continue to hold.

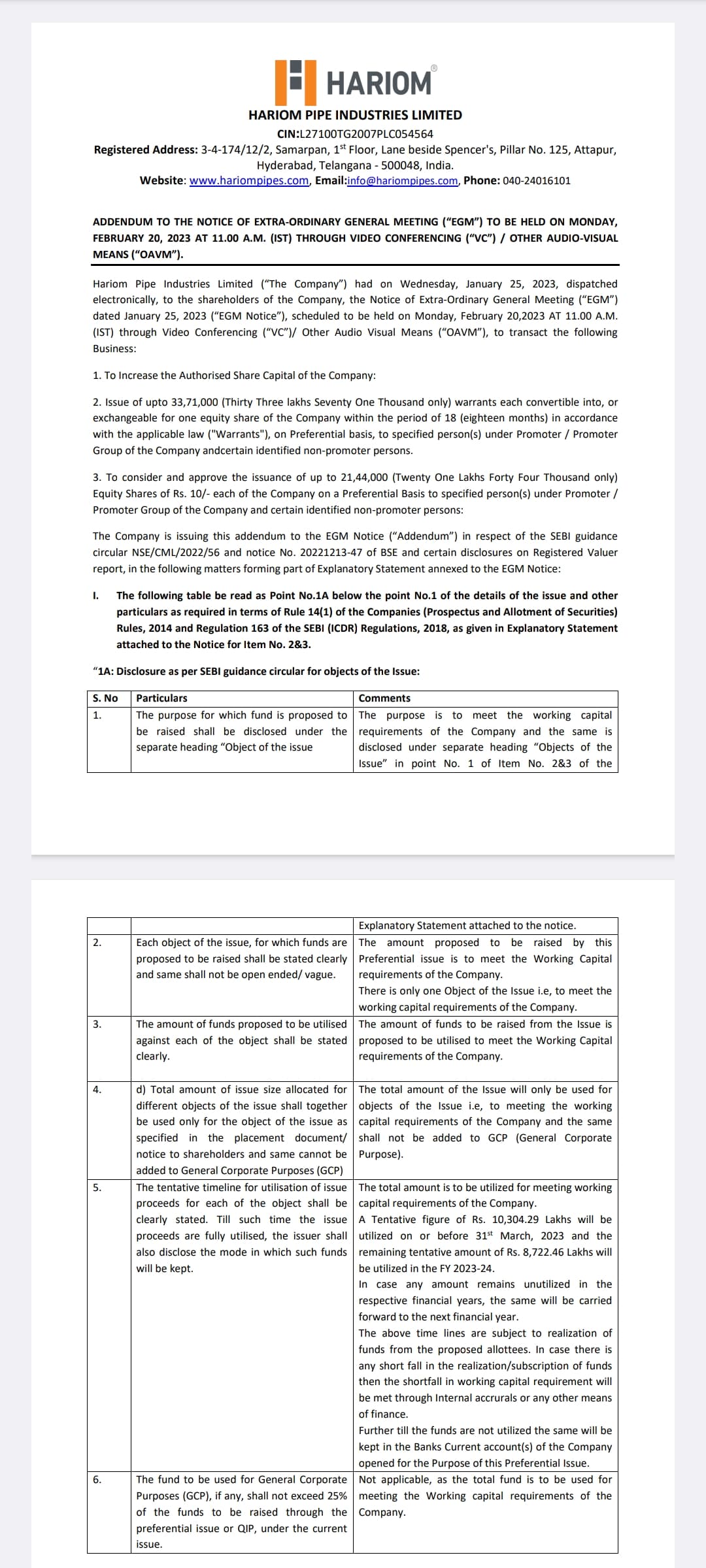

Hariom Pipes Ltd: A Capex Play! (14-01-2024)

Holdings were not sold… Warrants were issued to outside promoter entities leading to falling promoter holdings

Praj Industries (14-01-2024)

The entire ethanol space is subdued at present and praj is mainly linked to the same. So when the Ethanol story related stocks start moving, this will follow. Action in Ethanol space will begin post elections due ro sensitivity of the whole spectrum – sugar, rice, millets, husk, grain price + farmers who are biggest vote bank.

I may be wrong completely but thats what its playing out right now. Government flip-flops also indicate the same as they are treading extremely cautious lines and changing goal post at slightest of hint of things going in undesirable direction.

Sound sleep providers ..CYCLE is on HOTELS (14-01-2024)

ITC including Russell Credit: 16.13%

Sound sleep providers ..CYCLE is on HOTELS (14-01-2024)

Some key Highlights and answer by management on Concall 06.11.2023

Question: any updates on upcoming projects?

Answer and thread of the answer is interesting:

Mr. Vikram Oberoi – MD and CEO, EIH Limited: Actually, I just wanted to I think I saw a question from Sanjay as well, I will take that question now, Sanjay’s comment was on the strategy for 2030. And what I would like to mention is we have a vision EIH vision for 2030 which is at a very minimum 50 more hotels with about 4500 additional keys and we are focused on achieving that. You will see there will be some hotels that you will see in our annual report, more recently we announced a Trident Hotel in Tirupati which is done with Mumtaz Hotels and with EIH Associated Hotels in Vizag. As and when we announce projects we will as per stock exchange guidelines inform the stock exchange but we have a number of hotels that are coming to fruition and we will be able to make announcements I hope on an ongoing basis.

Mr. Amit Agarwal – Participant:

You said 15 or 50?

Mr. Vikram Oberoi – MD and CEO, EIH Limited:

50.

Mr. Amit Agarwal – Participant:

50 in the next 7 years?

Mr. Vikram Oberoi – MD and CEO, EIH Limited:

That’s correct.

Mr. Amit Agarwal – Participant:

How many will be managed and how many will be owned?

Mr. Vikram Oberoi – MD and CEO, EIH Limited:

It will be a combination of owned and managed.

Question 2

Mr. Saurabh Patwal – Participant:

-

Yeah. Yeah. So, thanks a lot for highlighting the big picture of your expansion. I just wanted your thoughts on two things. One is, our strategic partnership with Mandarin, which is the past you have highlighted, and also Reliance Industries announced three hotels in partnership with EIH. What would your thoughts and what’s EIH contribution to that partnership?

-

Mr. Vikram Oberoi – MD and CEO, EIH Limited:

-

So, would you like me to answer for both?

-

Mr. Saurabh Patwal – Participant:

-

Yeah.

-

Mr. Vikram Oberoi – MD and CEO, EIH Limited:

-

Okay. Yes, that’s correct, there was three hotels Reliance had made a press release and those details are in that and we look forward to developing those hotels and also other hotels with Reliance, I hope, in the future. As of now, it’s only those three hotels that Reliance had announced. As far as Mandarin goes, really the objective was to bring benefit to our guests and Mandarin guests, to bring benefits to our colleagues. So, there would be learning opportunities from each other. And those were really the two objectives and we continue to work on those fronts so that we can offer greater value, greater experience to Mandarin guests and vice versa and also enrich the experience of our colleagues, both for Oberoi group and for Mandarin.

Pidilite Industry : Fevicol ka Jod (14-01-2024)

Their main cash cow business is facing stiff competition from a player who probably has the deepest pockets currently. While they are more interested in trying to compete with market leader in another industry. This should logically mean that they commit very high capex in Paints business, while they feel competition in their cements business.

For me, it could be a potential case of mis-allocation of capital, because for them to gain market share in Paints, under-cutting the existing price points or giving higher margins to distributors would be the go-to way which would ensure they are not making much money for sometime, maybe like the Jio entry in telecom. But the difference here is, we do not have a 2-3 player market in Paints or Cements industry.

Paint industry is attracting players like never before- Astral and JSW too have joined the bandwagon and they also possess the same advantage (at least on paper) of having an established brand name in Infra material segment. But these many players, with reasonable willingness and ability to spend money is only going to cause pain in terms of margins and lower return ratios (because of high capex!)

Disclosure: Invested in Asian Paints, Pidilite and Astral. In the decision making process of selling Asian Paints, depending on how Grasim and JSW Paints perform in the next 6 months

Action construction equipment ltd (14-01-2024)

Thnx. Helped to clear concept.

However here in case of ACE they purchase under employee welfare trust and therefore as it is not ESOP trust my understanding…

Current purchase is not for ESOP purchase.

Is that right to concude?

Tata Consumer Products Limited (TATACONSUM) (14-01-2024)

So two large acquisitions as expected by the market. Key Aspects i wanted to analyse and drive deeper.

Chings Secret is bought out at 5100 Mcap with approx. 150 cr Ebitda for 2024. Thats 32-34x editda multiples. Looks fair but depends on TCPL to turbocharge growth by pumping the products across its distribution network.

Organic India not yet sure what to make of it. Will take a year to figure out. Overall not excited by the portfolio.

Gokaldas exports — cup and handle/rising channel (14-01-2024)

Haven’t attended any concall after recent acquisition after Atraco group, here is the latest [Rating Update] from Crisil (Rating Rationale)