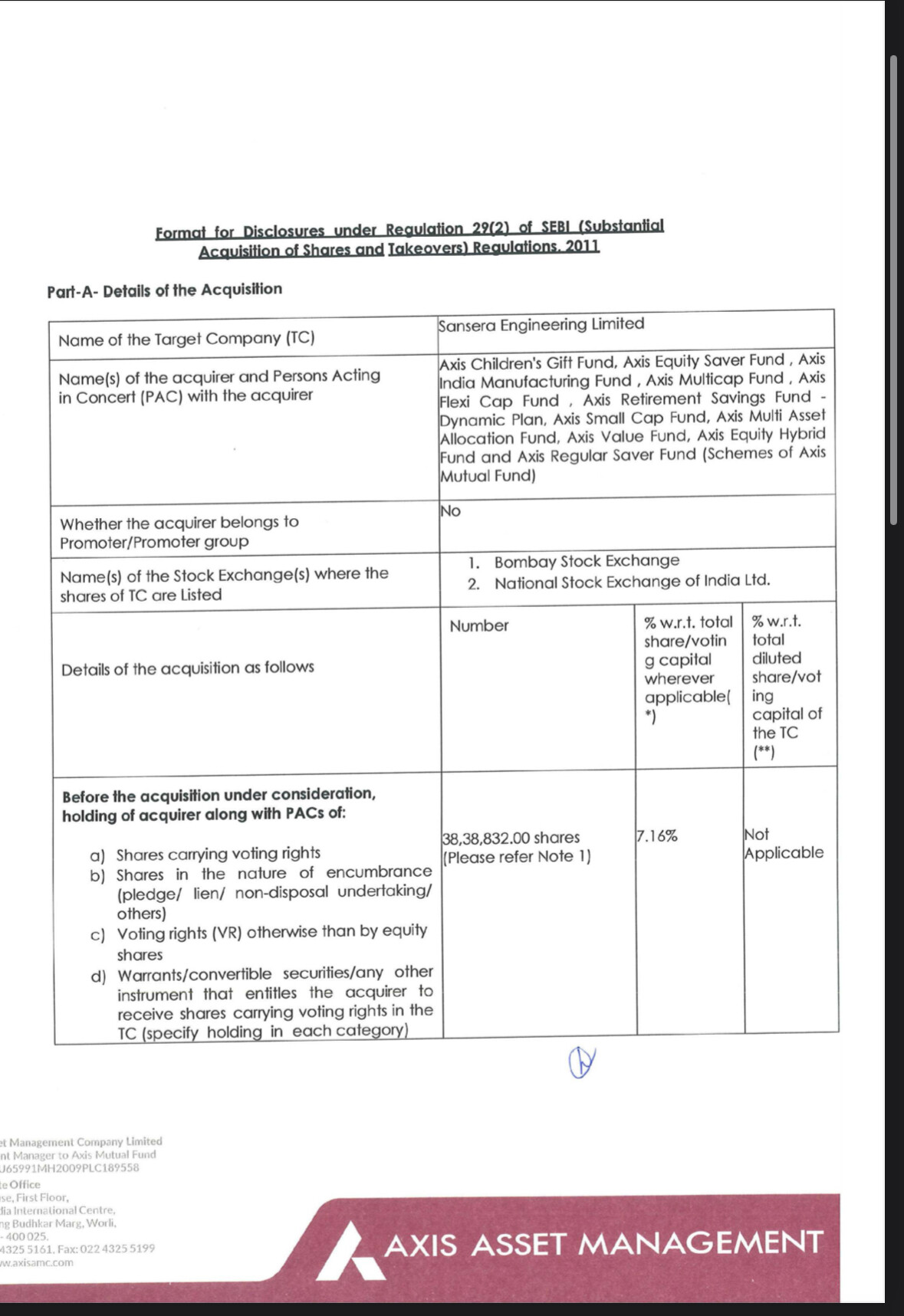

Axis Bank acquires stake in Sansera. Stock will most likely shoot up in coming weeks. Good news for us minority stakeholders.

Disc- Invested, 5.3% of portfolio

Axis Bank acquires stake in Sansera. Stock will most likely shoot up in coming weeks. Good news for us minority stakeholders.

Disc- Invested, 5.3% of portfolio

At the right price, everything is investable, even Ukraine. The sensex is selling at a PE of 25, so a yield of 4%, add 4-5% of growth and you get 8-9%, on average.

The Hang Seng is selling at a PE of 8, so a yield of 12.5%, add a few percentage points of growth and you are at 15%! Something like Alibaba has a market cap of $180 Billion, they have 50B cash and a FCF of about 20B, so you can get it a FCF yield of 6 – if that’s not value, I dont know what is. Plus the FCF is growing.

Of course, there are risks, but I dont care too much about a US or China recession. These things will happen at some point and they are difficult to predict! And recessions today are global because of interdependency.

If there is war between China and Taiwan, stocks are the last thing to worry about becuase the world will go to hell in a handbasket. People also say, oh chinese demographics are poor. Well, their population is similar to India’s and women’s labor force participation is 60+% compared to India’s around 25%. They will have enough workers for a long time.

With a GDP/capita of $12k compared to India’s of 2.5k, people have got a taste of the good life. Whatever political purges that might happen, China is not going back to Mao’s era.

Also, not to forget, China is about 20% of global GDP and approximately 50% of all Copper is consumed there. If you look beyond the noise, things in China are ok, bit of a slowdown, nothing else. When China is truly in a recession, I expect Copper to sell at $3, perhaps even $2.5 – we are far from there.

Tata Consumer Products on January 12 said it will be buying 100 percent stake in Capital Foods, which markets its products under Ching’s Secret and Smith & Jones brands, for Rs 5,100 crore in an all cash deal.

.

The FMCG company added that 75 percent of the equity shareholding will be acquired upfront and the balance 25 percent shareholding will be acquired within the next three years.

.

Ching’s Secret is a market leader in Desi Chinese across its product categories – Chutneys, Blended Masalas, Sauces and Soups. Smith & Jones is a fast-growing brand catering to in-home cooking of Italian and other western cuisines.

.

Tata Consumer said this acquisition will enable it to expand its product portfolio and further strengthen its pantry platform. The overall size of the categories in which Capital Foods operates in is estimated at Rs 21,400 crore.

.

The founder of the company holds 9.45 percent in the company while the rest is held by private equity funds General Atlantic and Artal Asia. Ajay Gupta is the founder of the company.

.

Estimated turnover of Capital Foods for FY24 is approximately Rs 750 to Rs 770 crore. The same was Rs 706 crore in FY23, Rs 574 crore in FY22 and Rs 667 crore in FY21.

Wow; Those are a lot of numbers to crunch!

What would be your data source for installed capacity for renewables?

Anyways i think there’s growth happening for renewable energy sector, the capacity infact grew by almost 14-15 percent in 2021-22 from the previous year; so definitely we are making progress

This i need some elaboration on

Yeah sounds right , as policy is also mostly geared towards EV currently, but so is/was the case with ethanol

And now aren’t we waiting for TESLA

I must confess i do not know the technicalities of those vehicles

This is a commentary from Krishna Apalla of Capitalmind, not Abacus.

https://twitter.com/iKrishnaAppala/status/1745480110822818075

@harmeet_kumar Great

As I was reading a article it said that China just met its 50% renewable energy

Coal accounted for 56.2% of total energy consumption last year, versus 25.9% from renewables which includes nuclear energy, the NBS data showed.

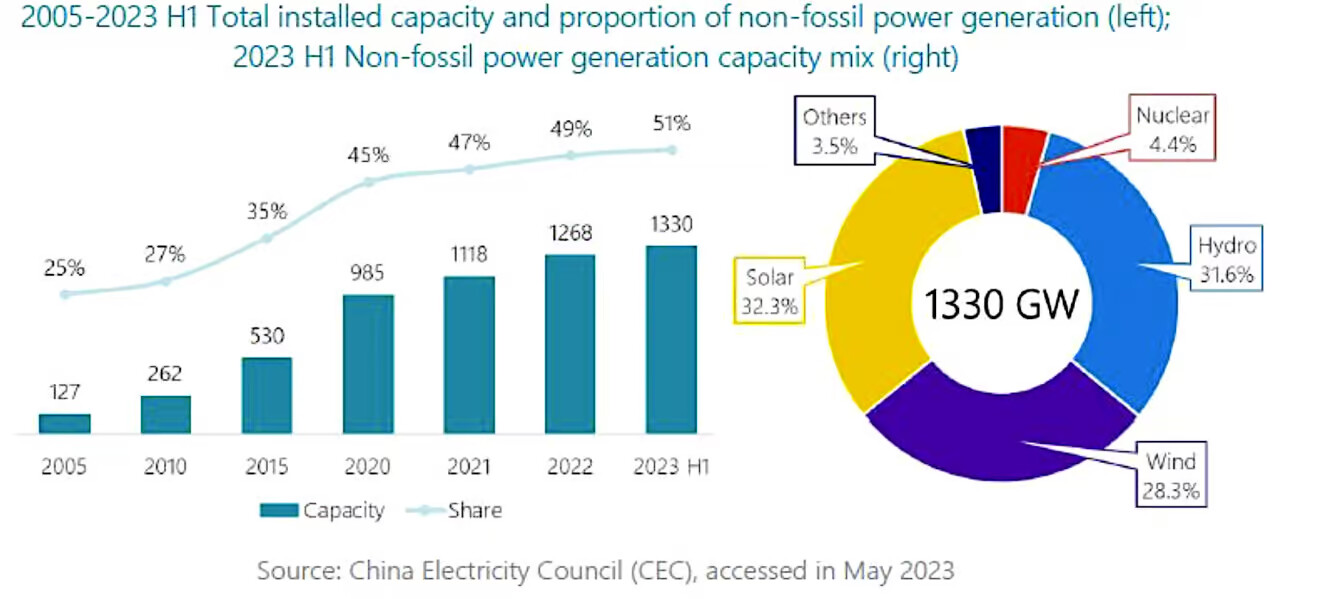

China’s national renewable energy power installation will exceed 1.45 TW, with wind and solar power installations surpassing 1 TW

China is leading the global renewables market

China’s estimated installation is more than double the number of U.S. and Europe installations combined

China’s wind and solar project investment is expected to reach $140 billion for 2023

Coming to our end – As of Nov 2023, we have a combined installed capacity of 179.57 GW.

The following is the installed capacity for Renewables:

The main reason was because China invested 6.5% of GDP value approx. value to renewable

India spent about Rs 13.35 lakh crore (Rs 13.35 trillion) in 2021-22, just over 5.5% of its GDP, on climate adaptation and expects to incur another about Rs 57 lakh crore (Rs 57 trillion) over the next seven years for this purpose, New Delhi told the UN Framework for Climate Change Convention (UNFCCC).

So that concludes that they did spend a lot on Renewable & Real Estate wherein now the Real Estate had filed for Bankruptcy.

Now China is leading on Renewable and on another if you notice 50% of their power is met via Coal and all of their industries are sweating : that’s the major concern as the AQI is over and above 200

The next growth where all are hoping towards is on Sustainability, Eco Friendly and Green Chemistry.

My thoughts

The advantage we have is low cost, sustainable future – as most of our industry are using green chemistry.

Now raw material is something that we need to source for which we had breakthrough in Iron-ion, Sodium-Ion – if this gets implemented, we will have a chance.

Now coming to your question.

See Amaraja, Exide, Panasonic, Eveready – all should do well : The main factor behind them all driving depends on the marketing and sales.

EV is rapidly catching up but Bio Diesal, Ethanol – all will have to wait because there is sugar shortage.

If you think Bio Fuel is sustainable – to a limit yes but also sugar degrades the soil and this inturn has its own complications.

I feel Sodium, Aluminum batteries, Bio Gas, Hydrogen – should all do well… its certainly not now.

This is the commentary from Abacus who sold full stake in Polycab today!!

For starters, Polycab (which was part of our Focused portfolio with an allocation of 5.5%) is currently in the spotlight for the wrong reasons. Just jotting down our thoughts on the current fiasco.

What actually happened?

Polycab had an IT raid on December 22nd. On January 9th, rumors circulated that there were around 1800 Cr of sales booked in personal records and another 200 Cr of tax evasion. The price started to react to this (down 9%) on that day. Post-markets, the company released a press release denying the claims.

Two days later, on the evening of January 10th around 8 PM, there was a press release from PIB (a media agency of the Government under the Ministry of Information & Broadcasting) indicating that the claims were true.

Why didn’t we exit on December 22nd on the news of the IT raids?

IT raids are rare but not uncommon. They keep happening regularly for companies (Manappuram, Astral, Shree Cement, etc, to name a few in the recent past). A raid alone shouldn’t be an issue. The findings & outcome of the raid are what matter. This press release at 8 PM yesterday has kind of clarified it, confirming the lapse in corporate governance.

Why didn’t we exit on January 9th when the rumors started to pour in?

In the current state of social media, it is difficult to distinguish between a rumor and news, and more importantly, the authenticity of it. Polycab was one of our core holdings, which we have held for the past three years (entered in February 2021). Technically, it is not feasible to react to every rumor and move the position in & out of our portfolio. So, we waited for a day to see how things unfold. Our eyes were on the price action. In these kinds of uncertain news, price action gives an early indication of the magnitude of the event. The stock was down 9%, and the next day, it kind of stabilized. So, yes, we waited for some clarity to emerge before making any decision. After yesterday’s press release, the news has become official.

Will there be another Polycab kind of event in our portfolio?

Honestly, I would be lying if I said that there will not be any more such events going forward. Because, fortunately, or unfortunately, we as outsiders have only a certain amount of information to deal with. And for the remaining unknowns, we have to rely on the company’s history, management background, publicly available numbers, and, more importantly, a certain level of trust (both in our process & the management). We have to live with it, and that’s where our risk management & position sizing comes into the picture. We usually don’t allow any single position to go beyond 10% of the portfolio, no matter how confident we are about the company. Even in the case of Polycab, we trimmed our position from 9% to 6% in September 2023, not because we anticipated this fraud, but because we were not comfortable holding large positions in a single stock.

Also, given the state of our bureaucracy and the system our promoters deal with for their day-to-day business operations, we have to accept it. Unfortunate to say this, but that is what it is. Everything is shades of grey, and it all depends on how you would like to react to it, and that’s how businesses grow. To an extent, the market has also accepted it. In fact, there was an instance (almost a decade back, and I heard from a senior investor) where a consumer appliance company, the promoter, went too clean and was not ready to pay a bribe to commence his new factory operations. This delayed the production and impacted its sales. The market didn’t like it.

Coming back to Polycab, it was a false communication from the company and a corporate governance failure. Having said that, three months from now, the stock can bounce back to its previous highs and move on. But that’s ok. That is the process we follow. For example, we exited Manappuram last year due to a similar kind of IT raid issue. We exited at 110/- levels, and the stock is now at 170/- levels. The same thing can happen with Polycab also, I don’t know. In fact, 4 out of 5 of our such exits may bounce back, but our process will save us from that fifth one.

Closing thoughts: This is not the first, and it will not be the last. We learn from our mistakes, implement them in our investment thesis & take it from there.

This is the commentary from Abacus who sold full stake in Polycab today!!

With the increasing fish meal prices and low supply from Peru, China increases fish meal prices, and disruption in global markets on fish meal supply due to adverse wheather conditions will Vistar Amar get any benefits ?.

Not holding any positions. Looking forward to make some positions

One of my family member is planning to take kidzee franchise. I just came around its financial health. Would you recommend taking some other franchize for a pre school other than it please tell. I know its a personal question but would be thankful for your replies.

Is this QIP beneficial for existing shareholders and sudden spurt in prices related to this in someway