Posts tagged Value Pickr

CreditAccess Grameen: Traditional MFI model, efficiently operating at scale (12-01-2024)

Best Small NBFC(10000-25000 Cr) Award

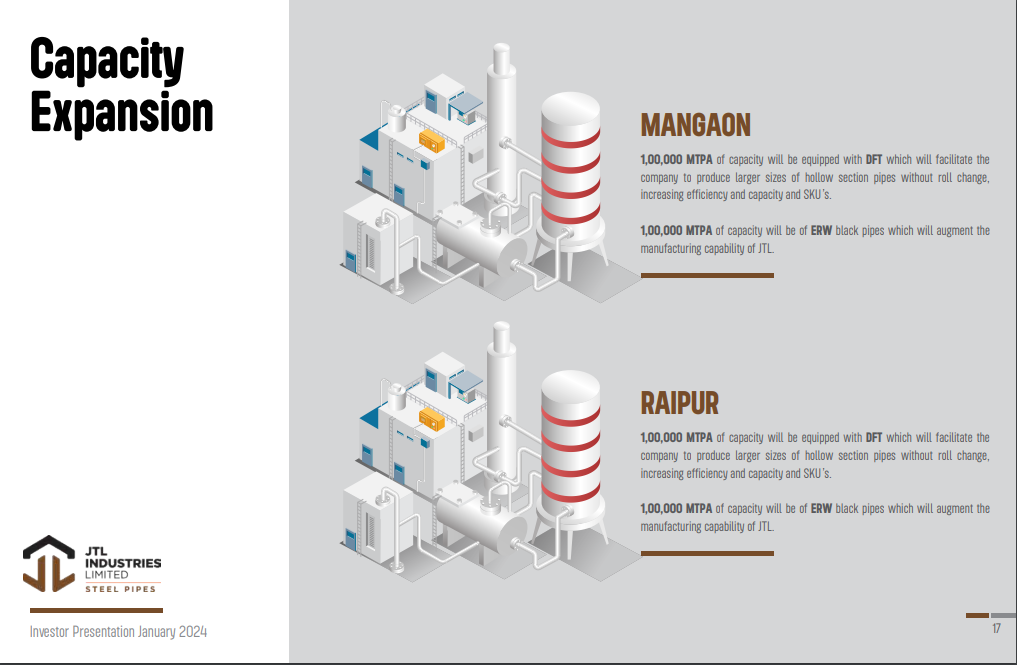

JTL Industries – Fast Grower at an inflexion point (12-01-2024)

The contribution of Value Added Products in the Quarterly Sales mix has been declining in absolute terms whereas the management is guiding to achieve 50% contribution of Value added products within the next two years.

The numbers seem contradicting the management guidance. Any idea why the contributions are declining? And if it should be a cause of concern?

Disc : Invested

JTL Industries – Fast Grower at an inflexion point (12-01-2024)

Detailed company presentation:

Telecom products – A way to play 5G, IOT, drones, connected cars, smart transport opportunity (12-01-2024)

Part -2 – Deep dive – FWA CPE

Let’s delve into some of the key telecom products:

5G FWA (Fixed Wireless Access) – touted as “killer app” for 5G

Fixed Wireless Access (FWA) uses 4G and 5G radio spectrum (the same as used for mobile phone services) to provide wireless broadband connectivity between two fixed points, for example a mobile network cell tower and a FWA device in a customer’s home. (Source: https://www.nokia.com/about-us/newsroom/articles/fixed-wireless-access-explained/#:~:text=What%20is%20FWA%3F,device%20in%20a%20customer’s%20home)

Market Size:

India: Addressable market size is 70 million households who are in the upper-mid income and high-income segments (over $8,500) which are expected to increase to 200 million households by 2030. Currently only 33 million households are connected to wireline broadband. Source: Jio ahead of competition in preparedness for 5G FWA deployment: Emkay, ET Telecom.

So as of today also there is gap of 50% owing to lack of fiberisation and related issues in many towns and villages in India. My estimate is that India is likely to have 50 million FWA customers by 2030 which means an opportunity size of 40,000 crores for domestic FWA CPE manufacturers.

Global: Ericsson predicts that globally there will be 330 million FWA connections by 2029 from over 130 million in 2023. This puts FWA devices revenue opportunity of 2.6lakh crore (over USD30 billion) globally, including India, by 2029.

Indian players are already exporting some network equipment so they seem competitive.

This is just one product puts overall opportunity of USD30 billion until 2029/30 growing at ~20% globally. While India domestic market shall grow in folds not in %.

Where: This can be used in remote places where fibre network is not available. In my personal opinion the product sounds so convenient (no cables required) this can even be successful in fibre dominated areas.

Why: Being wireless, it can reduce the massive upfront cost and time needed to secure permissions, dig trenches, lay last-mile fiber, and deploy technician-installed equipment at households and businesses. Moreover, operators can often roll out FWA using their existing mobile wireless networks and fiber backhaul infrastructure, further reducing costs. These factors have opened up markets for broadband services in places where it was previously unavailable, as we have seen in the Philippines, South Africa, Sri Lanka, and Turkey. (source: Fixed wireless access market growth | Deloitte Insights)

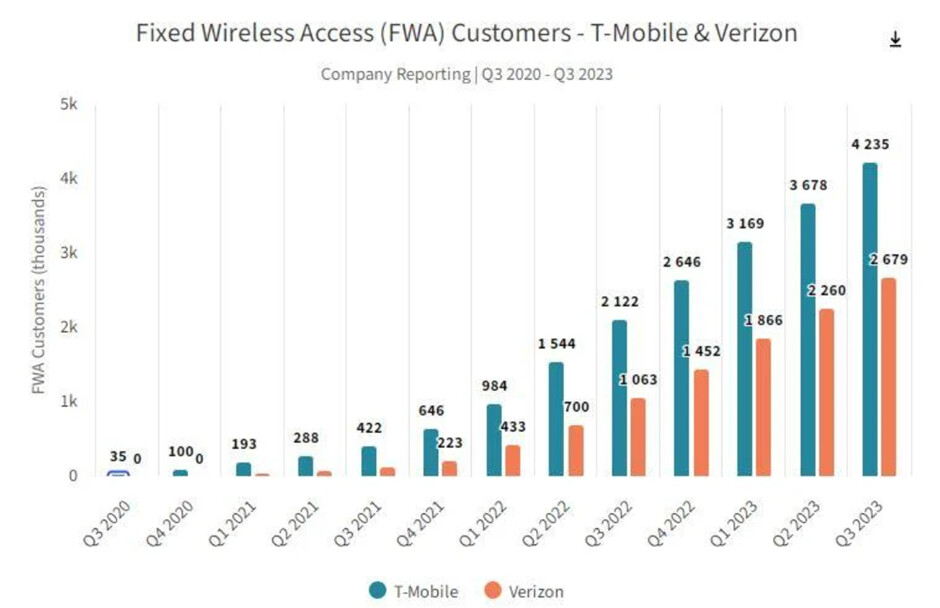

Growth? What happened when FWA implemented by two large telco players in the USA?

Source: Ookla: T-Mobile and Verizon lead in U.S. 5G FWA – Technology Blog

Verizon and T-Mobile had combined FWA customers at 35K in Q32020 by Q3 2023 it was ~7 million customers. A 200x growth in last 3 years and likely to continue to grow at over 30% until 2030.

In India AirFiber is launched by Jio and Airtel in last quarter of CY2023.

5G FWA is likely to grow at 90% annual growth rate from 2022 to 2025). (Source: #ET5GCongress: 5G FWA a huge opportunity in India as fixed broadband penetration is low: GSMA’s Peter Jarich, ET Telecom)

Beneficiaries:

Equipment makers (Frog Cellsat, HFCL, MNCs like Qualcomm, Ericson Nokia etc.), integrators (HFCL, Kore Digital, and MNCs), Network operators (RJio, Airtel), Tertiary beneficiaries – OTT and content providers/owners (Netflix, Youtube, Saregama, Tips), Digital marketing (Connected TVs, Affle), IOT, drones and maps providing companies.

Who is likely to be disrupted?

Internet service providers, Cable/DTH companies, Satellite networks (Nelco? Though I am not very sure on this), broadcasters (TV channels like Zee, CNBC etc.), traditional advertisers?

I welcome industry experts to share the knolwedge.

Disclosure: invested in HFCL, Tejas and Frog Cellsat. Transacted in these in the last 30 days.

Disclaimer: I am not a financial advisor and nor a SEBI registered Analyst. The content shared here is only for learning purpose. All the names mentioned here are for example purpose. I may buy more, exit or partly sell the stock/bonds without any prior intimation.

Dreamfolks services limited( DFS) (12-01-2024)

I think for dreamfolks the metric to track is growth of airport lounges, in terms of sq feet and also number of lounges, the devaluation of credit card reward was bound to happen, this kind of business is much more stable for everyone. I think I will rule out the possibility of a competitor getting in this business as GM should be stable around 10% atleast.

I wanted to understand how much banks are paying for lounge access, if on an average it costs around Rs 200-300 it can be sustainable with every year 5-8% escalation.

Devesh’s Portfolio Strategy and Construction (12-01-2024)

Both the stock picks I wrote about here in November have done well, as have the broader markets. But there is a set of learnings I want to share from these two picks which I am trying to articulate for my portfolio as a whole.

Styrenix: Since stock picking is a probabilistic sport, when you see multiple factors moving together along with a certain kind of pessimism because of surface level reasons, it is probably time to load up on the stock. Here, the demand scenario is still in favour with the auto industry restarting its performance, the management change brought a lot of efficiencies as demonstrated by the results, and there are additional capacity plans which are always interesting.

The surface level pessimism here was because of the promoter pledging and past governance issues. Remember a promoter has to take money from somewhere to get operating control back of a business they sold to an MNC and the governance transgressions happened at the time of the MNC promoters. Added to this was the smart money cornering. I think this stock hasn’t seen its potential yet, a better picture would emerge as the results for the company come back which can see re-rating here.

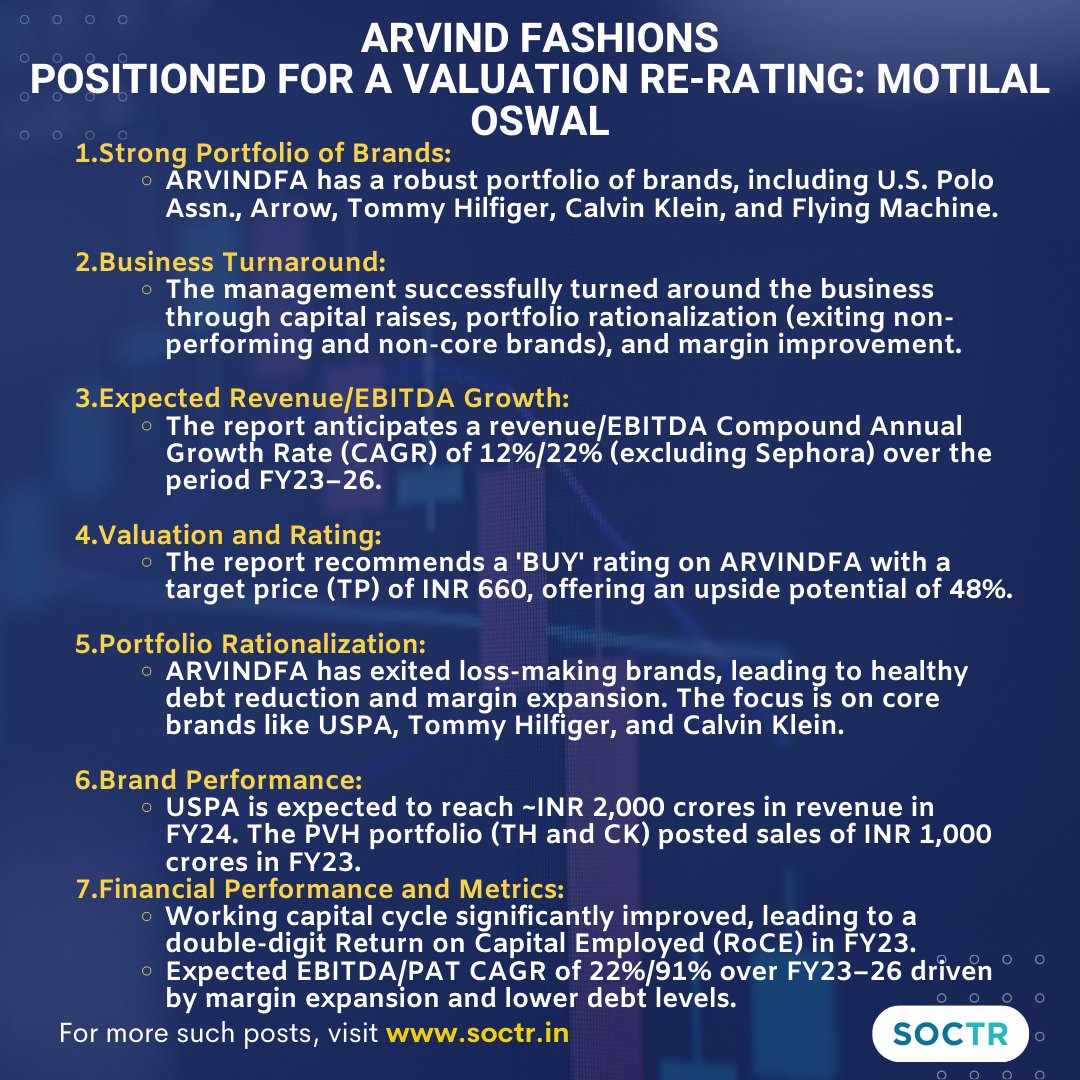

Arvind Fashions: Good investors were here, it was a recognised value stock always as I pointed in the write up above, all it needed was an event to change its perception to being the high growth company. The Sephora deal happened and still for some reason many people were skeptical, but this is where opportunities exist for investors like me.

Institutions take time to get to the bottom of events, for the people working there it is a job which pays you to do a Mon-Fri 9-5. For opportunity seekers, the motivations are completed different.

Now there is greater institutional coverage and research coming out on the stock, but I believe the results would be the main driving factor here. If the results are good, it can see good valuations, if not it will go back into a longer period of consolidation.

I’m slightly more skeptical of Arvind Fashion than Styrenix, but I’m sure that even through this there will be a learning I’ll have as the markets are the best teachers.

Attaching a note I saw on Arvind here.

Again the important thing is that this isn’t a buy or sell recommendation, higher equity prices make me scared about whats to come and I’ve done adjustments at the portfolio level accordingly. Also with a high interest environment all around us, it is very plausible to meet our financial goals through other instruments. Let’s not get overtly optimistic or keep expecting something which has a very low probability of happening.

Hitesh portfolio (12-01-2024)

Allocation in general is a very subjective aspect. It depends upon the comfort level and mindset of the investor. But speaking for myself, whenever I am sure about a sector having tailwinds, I allocate anywhere between 10-30% by creating a basket of stocks from the sector. So a conservative guy can take it up to around 10-15% and aggressive person can take it up to 25-30 % or more.

It will also depend on the prior experience of the investor while playing this kind of game. If someone like me who has enjoyed rides in these sectoral runs has to allocate, I would be aggressive, as I would not have too many inhibitions and I know a big about the game. Same may not be true about someone who has been burned while playing this game, or someone who is playing it for first or second time. After a point it all boils down to experience and skill.

Krsnaa Diagnostics – what is the diagnosis? (12-01-2024)

Today’s news in Himachal:

Krsnaa has closed around 650 labs in Himachal as the government has not paid an amount of 50 crore to Krsnaa under national health mission.

Due to this Krsnaa has not been able to pay salary to its employees working with them.

Disc: Invested

Source: Punjab Kesari

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (12-01-2024)

Lots of very well known companys do the same . Otherwise NIkon and Canon DSLRs would not sell without documentation/ warranty in kolkata metro gully .![]() . Its a case of Promoter using the company resources to run his side business off the record. Not good by any means but not uncommon either .

. Its a case of Promoter using the company resources to run his side business off the record. Not good by any means but not uncommon either .

IT department probably is sending the communication by runners so it might take time . Jokes apart, probably they are not sure about what all they can prove . Why else would the PIB notice have no company name ? This indicates they have not finished their invetsigation yet .

Regarding the questions…

- In my useless opinion , you are right. The charges and fine should be on the promoters head and not on the company .

- Same things were alleged about Munjal of Hero Motocorp last year …it was PMLA case . He is decidedly political and his party is not in power for a while . Was he arrested ?

Disc. Still invested and confused but sold half yesterday since that ensured that I have taken out my capital and same amount of profits . I intend to let the rest alone and probably add back some more if it indeed falls below 3300.