You may have entered DBOL at higher price but be patient. You can check the volumes and delivery based buying here.

https://web.stockedge.com/share/dhampur-bio-organics/105671?section=deliveries&exchange-name=Both

You may have entered DBOL at higher price but be patient. You can check the volumes and delivery based buying here.

https://web.stockedge.com/share/dhampur-bio-organics/105671?section=deliveries&exchange-name=Both

Good one Brijwanth. Am of the same opinion, we just need to wait for the right price discovery after selling is done. If polycab hadn’t given this kind of returns in very short time, This wouldn’t be the scenario. Probably market would have shrugged off this after a while. General psychology, if you have already made 4x kind of returns, 90% of the folks wouldn’t think twice to cut down their holdings or even sell off completely on the bad news. I guess that’s what happened so far. My take is once you see good results from the company in the near future, market will eventually forget this giving them a chance to correct governance isssues. Look at hero motorcorp, Manappuram, shree cement they gave very good returns after IT raids issue. Problem with Polycab was it’s hyper valuations. Overall, it’s a buying opportunity for me it it comes to 3600-3800 Zone.

Some light is thrown by Ajay Rotti, a well-known taxation lawyer on Twitter

What is the collective opinion on this forum on how Symphony is growing? Below are some of the questions i am pondering –

(1) The market size is unquestinably big. With electricity costs rising, high humid climate every year, with 50% market share, I would assume that Symphony can grow easily by 20-30% or so each year in India, but that has not happened in the last 10 years… why?

(2) Their foray into International markets has not seemed to have gone well. Australia was a disaster in a way. They are recovering but in retrospect, was it a good bet and why they could not succeed? They did okay in Mexico but not in Australia.

(3) They are not having high debt which is good. Relatively decent inventory turns. How is their overall capital allocation strategy in your view in the absence of seemingly slow growth over a long term?

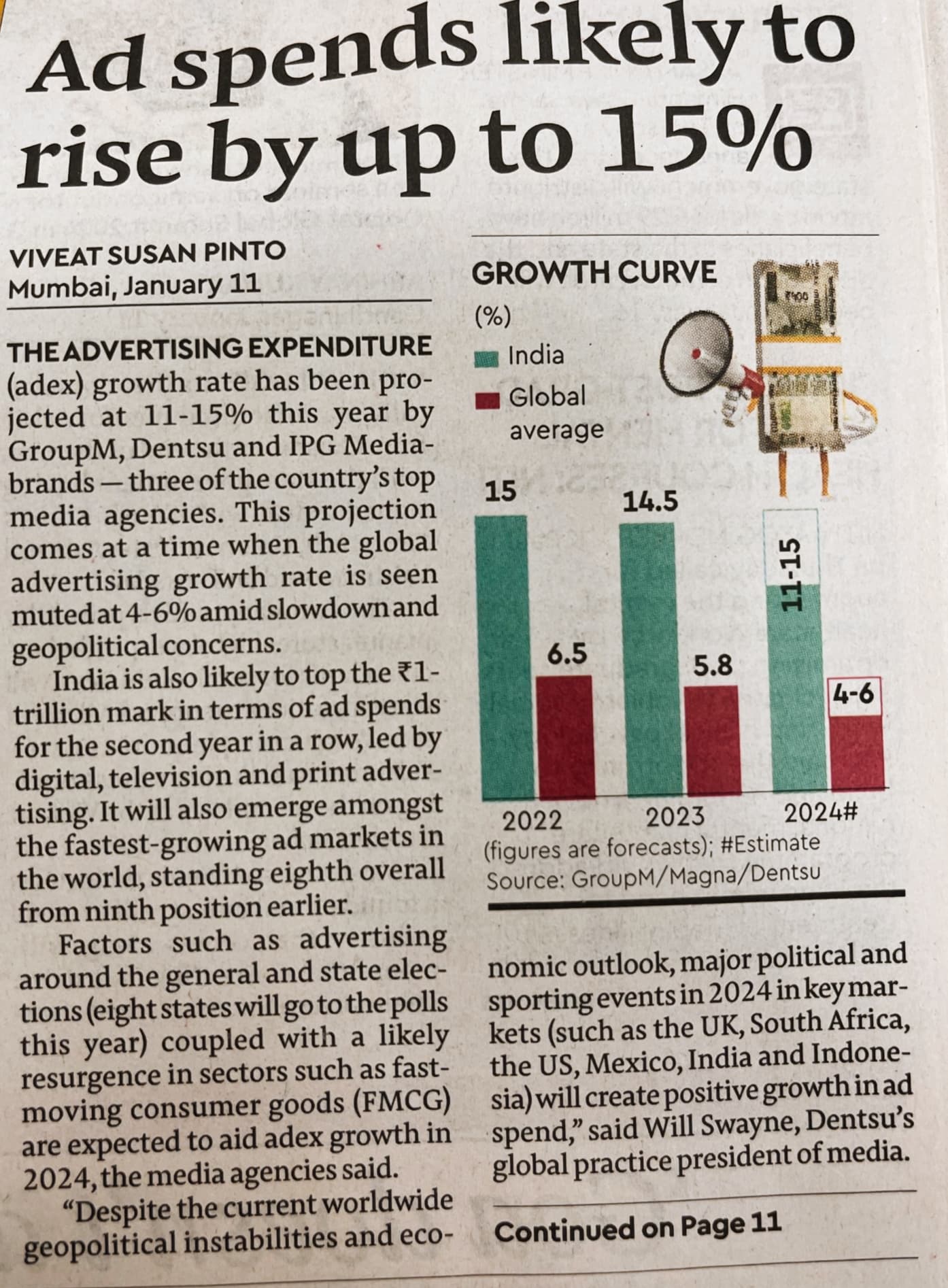

Advertising industry in focus

Strong Quarterly growth update from Ugro, However fluctuations in collection efficiency remain baffling as always…

Let’s think pragmatically and please go through my 2 min. read.

There will be overhang on the stock price till a payment is made by the Company or the issue is resolved.

What does IT Dept. tell us 1000 Cr. Sales + 400 cr. Cash payment +100 cr. Expenses so total problem currently Est. 1500 Cr. Max Tax impact 50% so Rs. 750 Cr.

Can be paid with 2 qtr profit (Last yr. Profit Rs. 1600 Cr.). This is subject to Company not contesting and all the legal procedures. All this takes time.

If promoters are not arrested and the amount is limited to Rs. 1500 Cr. Then above scenario plays and the company will not go bankrupt.

Now the problem is simple – shareholders who are selling particularly FII’s and DII’s. How low can they make the price fall and who will buy when they sell. Surely price will settle at equilibrium.

It is our job to find that equilibrium. Why? You are getting India’s largest wire manufacturer intact(Factory’s are not sealed) at a discounted price.

That’s my 2 min read of the situation.

Disc: Invested. I’m not a SEBI RIA. Please consult an RIA before investing.

Does anyone have a current-status update on DCX ?

Any new triggers / partnerships etc?

What is the guidance on CAGR for the next 3 years?

Thank you

Finolex has its own issues related to ownerships. Otherwise it would have never traded at such low multiples to its peers.