Posts tagged Value Pickr

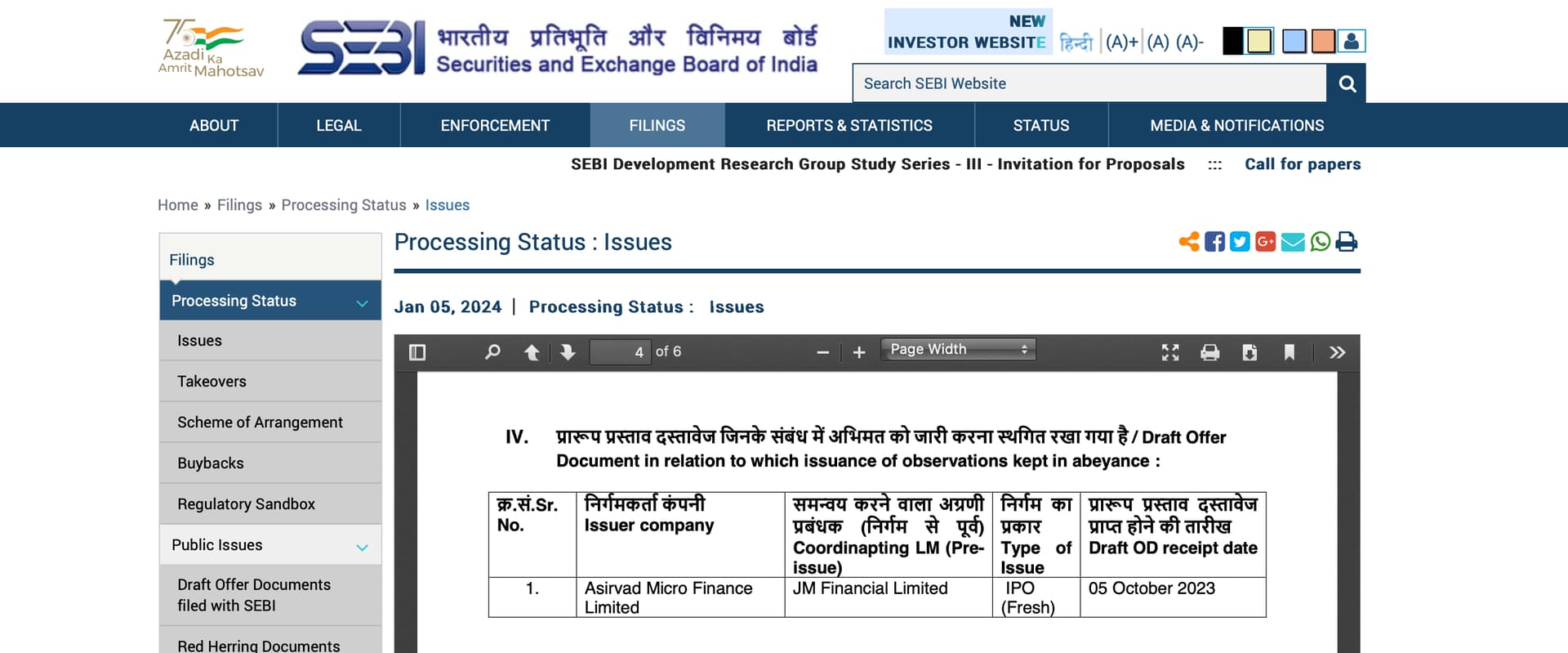

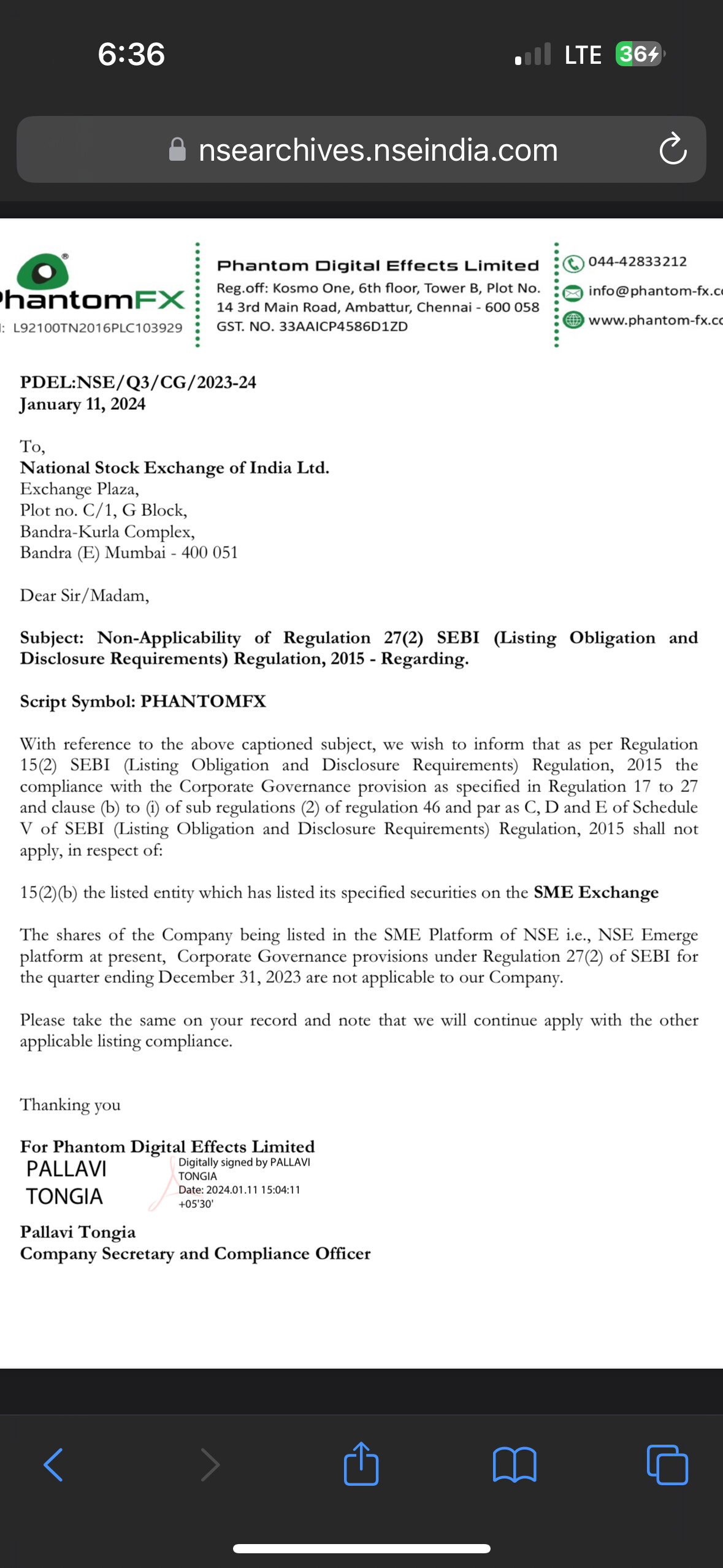

Phantom Digital Effects Limited (11-01-2024)

Hi, newbie investor here. Can anyone please explain what this notification means? Will they continue to be listed on SME Platform?

Another question I had was how long the company stays in SME platform normally before it gets listed on Main board?

Is it something that Board decides or the company?

Sorry for asking basic doubts.

Disc- invested, 6.4% of portfolio.

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (11-01-2024)

yes, kindly share management views as and when received, please

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (11-01-2024)

Ill like to hear from management before i take any decision and i wish people do the same before buying the dip!!

Power Mech Projects – Not a typical Power Infra Company (11-01-2024)

Failed Rising Wedge (or any Pattern)

The failure of the rising wedge pattern is evident in the technical charts. When analyzing price movements, it is crucial to consider both price and volume dynamics.

Observing the price action on up days, specifically on 29th Dec, 1st Jan, and 2nd Jan, it is notable that the trading volume was consistently high. Conversely, during the downward price movements on 3rd to 5th Jan, the volume was comparatively lower than that observed on the up days.

This discrepancy between volume levels on up and down days suggests a weakening of the rising wedge pattern. The failure of the any pattern becomes apparent when taking into account the mismatch in volume during upward and downward price trends.

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (11-01-2024)

Kapur ji

Ultimately all investments are If and Hope only…

You are also hoping that all your portfolio companies do good and they will take market share , you also hope that no corporate governance issue happens in your companies, You also hope that your company products dont become obsolete and some new threat doesnt wipe out your company… Investment totally depends on IF and HOPe, no matter how much logic and study and expertise we apply…Everything boils down to IF and Hope.

We all Hope that we dont die today, so we can enjoy returns of our portfolio, But IF we die then…

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (11-01-2024)

very good company of its sector. Valuations seem to be getting appropriated and good zone to buy here. will re-bounce once this period is over

Everest Industries – Multiple Drivers in place (11-01-2024)

My notes from AGM fy23

22/08/2023

Boards and Panels Division

-

The category is in nascent stages of development and management seemed quite confident of growth in size of the market.

-

The co. is building the market by creating awareness among influencers (Architects/Interior Designers) and training the technicians.

-

Cement, Silica and Fly Ash are important raw-material for manufacturing boards.

-

The division has started contributing to profits and profitability will go up as scale increases.

-

Margins for VAP are around 50% more than commoditised products.

-

A greenfield expansion worth 187 cr is under way in Karnataka. The same will be completed by end of 2023. 72000 MT.

-

There is a decent opportunity in export markets with higher margins. The co will focus on the same after new capacity comes up.

-

The co was able to pass on rm inflation in this segment.

PEB Division

-

The co is among Top 5 players in the country.

-

The co has turned around this segment by undertaking complete overhaul of processes and focusing on marquee customers.

-

A projects takes 3-6 months to complete, from finalisation to execution.

-

The co is buffered from steel price fluctuations and 8% type EBIT margins are sustainable. Margins can improve going forward, high probability on account of extracting efficiencies.

-

The co is focused on Factory and Warehousing market and is seeing a lot of repeat orders from customers.

-

The co has undertaken capacity expansion in South at the cost of 125 cr.

-

This segment is witnessing strong tailwinds.

Roofing

-

The market will grow at a meagre 2% on volume basis. The co maintained its market share in spite of tough times. Increases in prices of asbestos fibre (25% of total cost) hurt profitability. The co was unable to pass on rm inflation. Focusing on reducing cost by developing alternate sources of supply and innovation. High rm prices persisted even in q1 of fy24 (Verify).

-

Roofing is a seasonal business. March-June. Inventory peaks in March and bottoms out by June, almost halves in size. The co is taking efforts to reduce inventory days and improve WC.

General

-

Past few years were focused on plugging performance gaps, becoming efficient and building management team. The stage is set for growth and co is entering an investment phase. 100-150 cr deployment every year foreseeable for next 4-5 years (Verify).

-

Chairman, despite being of non-executive designation, appeared to be shaping the course of the co and keeping an eye on execution. The board has set high standards for the management are excited about future of the co

-

The co reduced Tax Liability by 80 cr in the fin year gone by.

-

FCF in q1fy24 is at 143 cr.

Disclosure: Invested

Everest Industries – Multiple Drivers in place (11-01-2024)

My notes from AGM fy23

22/08/2023

Boards and Panels Division

-

The category is in nascent stages of development and management seemed quite confident of growth in size of the market.

-

The co. is building the market by creating awareness among influencers (Architects/Interior Designers) and training the technicians.

-

Cement, Silica and Fly Ash are important raw-material for manufacturing boards.

-

The division has started contributing to profits and profitability will go up as scale increases.

-

Margins for VAP are around 50% more than commoditised products.

-

A greenfield expansion worth 187 cr is under way in Karnataka. The same will be completed by end of 2023. 72000 MT.

-

There is a decent opportunity in export markets with higher margins. The co will focus on the same after new capacity comes up.

-

The co was able to pass on rm inflation in this segment.

PEB Division

-

The co is among Top 5 players in the country.

-

The co has turned around this segment by undertaking complete overhaul of processes and focusing on marquee customers.

-

A projects takes 3-6 months to complete, from finalisation to execution.

-

The co is buffered from steel price fluctuations and 8% type EBIT margins are sustainable. Margins can improve going forward, high probability on account of extracting efficiencies.

-

The co is focused on Factory and Warehousing market and is seeing a lot of repeat orders from customers.

-

The co has undertaken capacity expansion in South at the cost of 125 cr.

-

This segment is witnessing strong tailwinds.

Roofing

-

The market will grow at a meagre 2% on volume basis. The co maintained its market share in spite of tough times. Increases in prices of asbestos fibre (25% of total cost) hurt profitability. The co was unable to pass on rm inflation. Focusing on reducing cost by developing alternate sources of supply and innovation. High rm prices persisted even in q1 of fy24 (Verify).

-

Roofing is a seasonal business. March-June. Inventory peaks in March and bottoms out by June, almost halves in size. The co is taking efforts to reduce inventory days and improve WC.

General

-

Past few years were focused on plugging performance gaps, becoming efficient and building management team. The stage is set for growth and co is entering an investment phase. 100-150 cr deployment every year foreseeable for next 4-5 years (Verify).

-

Chairman, despite being of non-executive designation, appeared to be shaping the course of the co and keeping an eye on execution. The board has set high standards for the management are excited about future of the co

-

The co reduced Tax Liability by 80 cr in the fin year gone by.

-

FCF in q1fy24 is at 143 cr.

Disclosure: Invested

Mangalam Organics Ltd. – A promising Pine chemistry story (11-01-2024)

Tried all the products, the products appears nice with the signature fragrance of camphor

This new line will re rate the stock

Margin expansion

Top line expansion

Improvement in roce

And more drivers

Invested