What the company has lost is the integrity premium. A management without integrity can do many bad things than what has been discovered so far… So, market is just willing to remain on the safe side.

Disc: Just my opinion.

What the company has lost is the integrity premium. A management without integrity can do many bad things than what has been discovered so far… So, market is just willing to remain on the safe side.

Disc: Just my opinion.

Hi Ranvir, Curious why you call Bajaj Auto as cheap when its trading close to the highest EV/EBIDTA valuation since 2009! I feel Maruti in the 4 wheeler space seems to be a better pick in auto at current valuations…

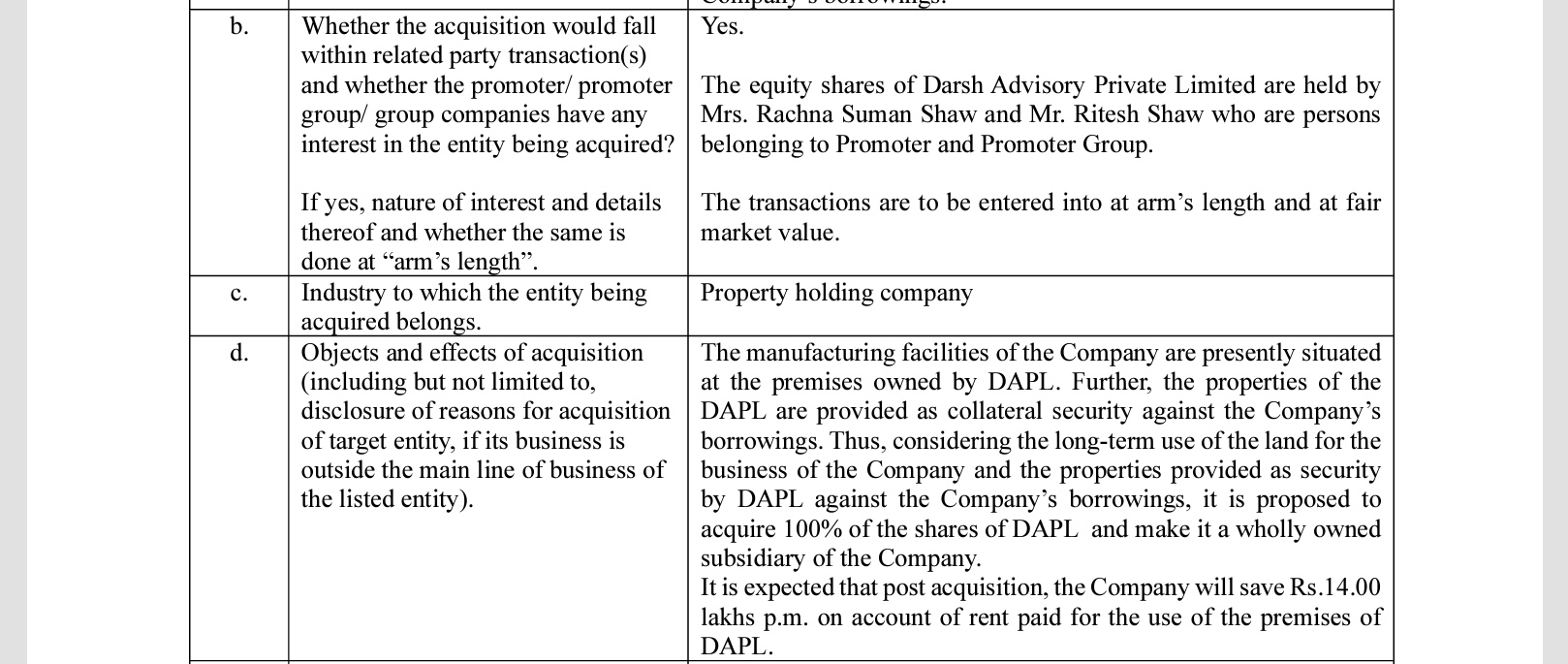

DAPL was owned by the promoter, Mr. Ritesh Shaw; the rationale for the acquisition was duly disclosed at that time. Hope this helps.

FundRaise 1.pdf (647.6 KB)

if media reports to be believed company did some 1000 crores sales in cash transactions.

If found guilty they need to pay tax plus some penalty.

On 1000 crores 10% net profit equals 100 cores and 30% tax is on net profit equals 30 crores.

Even if we assume 100% penalty company will be required to pay 60 crores. Assuming management learnt its lessons those unaccounted sales transactions will become part of sales from next reporting.

Stock has already lost 30% since the news and current market cap is at 60k crores. So for 60 crores impact company has lost 25k crores market cap??

Even if we consider that this transaction is done by management , still the amount is not substantial compared to the size of this business. Ultimately company is a market leader in cables and wires, and in FMEG also a leading player. That business will not vanish in thin air, neither its leadership in market is challenged by other players due to this fiasco. They why so much over-reaction?

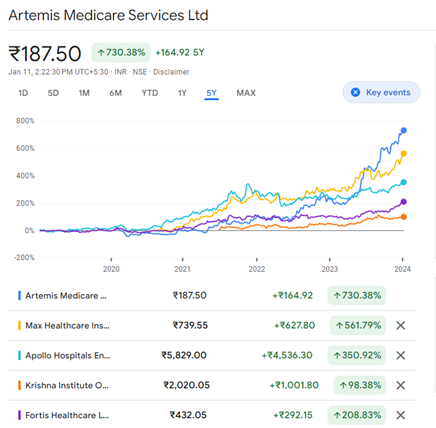

I have been tracking this Hospital since a year now and have some interesting insights on this name. Looking forward to interesting discussion on the company.

Artemis has been one of the silent and probably the best performer in this Hospital Rally:

The business growth and profitability has performed well over last 2 years. Company is growing at ~20%+ with strong margin expansion. The Stock has re-rated well from 8-10 EV/EBITDA to ~20x EV/EBITDA now (v/s. peers at 25-35x EV/EBITDA).

About Artemis Medicare:

Artemis Medicare, founded in 2007 (90 beds) operates as a standalone multi-specialty hospital with 541 (FY23) bed capacity (394 bed in FY21) spread over a 9-acre land bank. It currently generates ~95% of revenue (FY23: 691Cr) from its flagship hospital at Gurgaon and the remaining ~5% (FY23: 47Cr) from other asset light hospitals like Daffodils (Luxury Paediatric care), ACC (Artemis Cardiac care) & Artemis Lite (Secondary care Hospital). It is focused on the Northern region of India with its flagship hospital situated at Sector 51, Gurgaon (~6km away from Medanta Medicity and ~5km from Fortis, FMRI). It is at par with the top listed hospitals in terms of Equipment, Doctors, Occupancy (80% over FY18-20 and ~70% after expansion of 150 beds at tower-2), ARPOB (75K per day) & ALOS (3.7 days). Artemis generates ~35% of revenue from international patients which is highest vs other listed peers in Indian Hospital Industry.

**The Story that I understood:**

Expansion of beds at Flagship Hospital led to the significant growth in business and subsequently the Stock price:

• Artemis was pre-dominantly a 400-bed hospital running at peak capacity until FY21 (Peak Topline of Rs 550Cr in FY20 with 80% Occupancy). After running at peak capacities for a decade, the company expanded its bed capacity by ~150 beds by opening tower-2 adjacent to its Tower-1 at Gurgaon during FY22 (Thus, a brownfield expansion, which is very lucrative in the Hospital Industry). This took the total bed capacity from 400 beds to 540 beds starting FY23.

• This expansion scaled up successfully with company doing 70% Occupancy on ~430 operational beds. This led to a Revenue growth of ~23% CAGR over FY22 (528Cr) to H1FY24 Annualized (~800Cr). This led to an incremental Revenue of ~290Cr over FY22 to H1FY24 Annualized. Being a Brownfield Expansion, the operating leverage kicks in, as the key head doctors remain same and other operational costs get distributed to a larger base. Thus, EBITDA for the Gurgaon Hospital almost doubled from ~Rs 63Cr in FY22 to ~Rs 130Cr in H1FY24 Annualized, a CAGR of 44%. The EBITDA Margins expanded by ~500 bps during the same period.

•

• Interesting to note that on incremental basis (between FY22-H1FY24 Annualized), company is poised to generate ~280Cr of Incremental Revenue and ~Rs 67Cr Incremental EBITDA, thus generating 23% EBITDA margin on incremental sales.

•

What can be the story ahead:

• While showcasing a strong execution during FY23, the company was in process of building tower-3 in the same vicinity of Gurgaon Hospital, and this time with a larger bed capacity of 200 beds. This would take the total bed capacity 750 beds. The tower-3 is expected to commercialize from Q1FY25 onwards and will drive the next leg of growth for Artemis.

• Ballparking the current execution, I believe the economics look very interesting for the company:

o With a capacity of 750 beds, there would be 600 operational beds (usually 15-20% beds are reserved for government patients).

o The current ARPOB for the company is ~76K per day and it can grow at ~3-5% CAGR.

o The Occupancy for the company is currently at ~70% which will be a little depressed in FY25 due to addition of new beds. In the initial year the tower-3 (with 250 beds) can do ~35% Occupancy followed by ~60% in Year 2 and ~70%+ in Year-3.

o Thus, the Blended Occupancy for the company on ~600 beds can be somewhere between 70-73% over FY26/FY27.

o Thus, the Revenue potential from the Gurgaon facility can be of ~Rs 1200-1400Cr (Assuming 600 beds * 72% Occupancy * 80K ARPOB per day * 365 days = ~Rs 1,250Cr)

o Since it is a complete brownfield expansion, the EBITDA margins can further see some improvement and can improve by ~300 bps from ~16.7% currently to ~20%. This can generate an EBITDA of ~250-280Cr during FY26/27 vs Current EBITDA of ~130Cr in H1FY24 Annualized.

• Another Kicker which the company can have is earning fee via O&M model. Artemis has Bagged O&M contract with 200 bed Mauritius hospital which can directly contribute to the topline and bottom line.

• Artemis is expanding via smaller format Hospital:

o There are 3 types of small format hospital which the company currently operates under:

I. Daffodils: 30-40 bedded Luxury Paediatric Services

II. Artemis Lite: 50-100 bedded secondary care hospitals bridging the gap between a family physician and multi-specialty hospital.

III. Artemis Cardiac Care (ACC): Operating Cath labs with partnered hospitals. ACC is a JV between Artemis (holding 65%) and Phillips medical system.

o At mature state, these spokes can contribute 20%+ EBITDA margins and 16% ROCEs with 4-5Cr of investment and ~12-18 months of breakeven period.

o These spokes act as a referral point to the Flagship hospital and help lever the Artemis Brand in and around the region.

o Currently the scale of these 3 formats combined is ~80Cr on H1FY24 Annualized basis. Currently it is not EBITDA positive (just breaking even), but the With newer centres to be opened every year, this part of business will take 2-3 years to stabilize. It can become a Rs 200Cr Franchise with ~15% margins by FY26/27.

o Potentially Artemis can generate a EBITDA of ~30Cr from here after next 2 years.

o Although this business is margin dilutive currently, this can turn out to be a decent investment for Artemis over the next 3-5 years. Considering it is a small part of the business, this should not affect the aggregate business.

• All these business plans point towards the willingness to grow and create Artemis a global brand. Lastly, the company appointment Dr Devlina Chakravarthy as the MD & Whole-time director in FY21 (previously only WTD since inception) and awarded 69.7L shares as ESOP (~5% of the company) in FY21.

• Valuation:

• Assuming the company can deliver ~250-280Cr EBITDA just from Artemis Gurgaon Facility over FY26-27, at current Enterprise Value of Rs 2,800Cr , it trades at just 10-12x FY26/27 EBITDA.

• Basis on current Industry valuation, the peers trade between 25-35x EV/EBITDA.

Additional value can be generated from successful execution in the smaller format Hospital and O&M fees from Mauritius.

Disclosure: Educational purposes only, Not a buy recommendation, I am not SEBI registered analyst or advisor an I am invested in it hence my views may be biased.

UTI AMC Q2 FY 24 concall updates –

Company inaugurated 29 new UTI offices across the country on 29 Sep taking the total tally to 195 offices

Company focussed on driving its presence in B-30 cities ( ie tier -2,3 cities ). 135 of company’s branches / offices are in B-30 cities

Launched their mobile app in Q2 for their customers and distributors with state of the art technology

Total AUMs at 16.9 lakh cr, up 17 pc yoy

Domestic MF AUMs at 2.67 lakh cr, up 14 pc yoy. UTI’s mkt share in MF industry at 7.8 pc at the end of Q2

Equity AUM at 78k cr, up 9 pc

ETFs AUM at 98k cr, up 35 pc !!!

Total live MF folios at 1.22 cr

Avg SIP/month at aprox Rs 540 cr with avg SIP size of Rs 3150 / month

23 pc of UTI MFs AUM are contributed by B-30 cities vs the industry avg from B-30 cities at 17 pc

Launched 04 new NFOs in H1

Consol revenues @ 404 vs 435 cr

PAT @ 220 vs 262 cr

Company has got the permission from SEBI to start their US operations

Company was following the growth strategy in equity MFs whereas the Mkt has been rewarding the value strategy offlate. Hence there has been pressure on equity MF mkt share. Company is making course corrections ( a key matrix to track )

Company holding an investment book of around Rs 3900 cr

Company has increased its mkt share in the Hybrid schemes

Likely to lunch 3 more ETFs in H2, FY 24. Not launching any active equity schemes as of now

Effective tax rate for full FY to be around 21-22 pc

Disc: hold a small tracking position

Stock is under stress today because of Polycab saga. Any views?

I couldn’t find it on SEBI website

But almost all news Channel has the same news so must be correct

Any how it’s just a delay /hold which is not unusual with IPO

Manappuram was due for rapid correction given one way upside move

Need a break before next move

Continuing on this post- my estimates say they reach about 900 crs in FY25 and 1200 odd crs in FY26. Question only remains can they find optimal capacity utilization becasue the costs of capitalisation are going to skyrocket starting FY25.

Additionally, I would really appreciate if someone shared the macro outlook on rubber and lubricant chemicals if they have access or sector knowledge. Macro info is a little hard to track