I deleted the post beacuse of my mistakes in estimating the earnings and at the same time i also don’t want anyone to get the wrong post.Will correct my mistake soon.

Posts tagged Value Pickr

Yasho Industries (10-01-2024)

Yes we all are here to learn. Thank you for correcting my mistake.Look forward to learn from you as well as from others.

Creative Peripherals (now Creative Newtech) – Micro cap with big ambitions (10-01-2024)

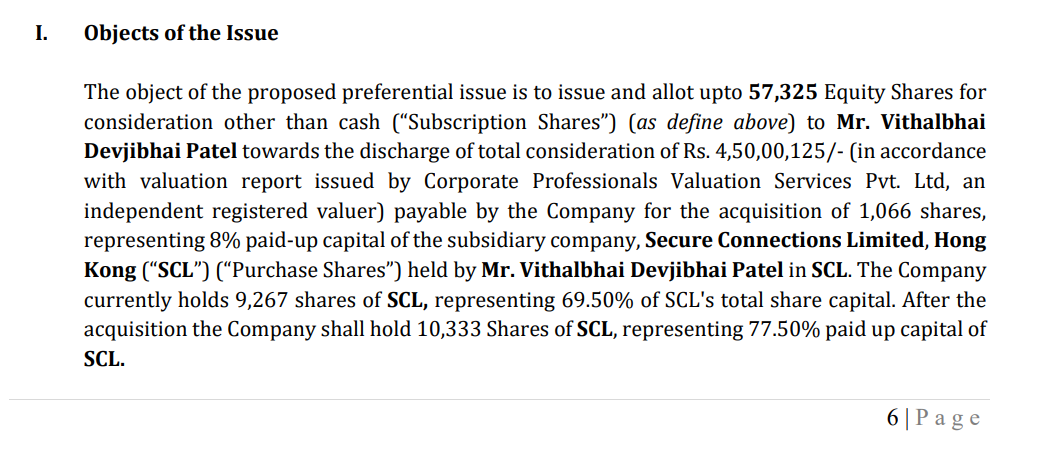

Company Has Entered into share swap agreement where the shares of subsidiary are swaped for 8% stake

Subsidiary is value at 56 Crores.

The Transaction seems fairly valued considering the whole business of Honeywell is Under the Subsidiary’s Name (I can be wrong)

FY-22 Hong Kong business did the PAT of almost 7 Crores (Couldn’t find data about 2023)

the implied multiple is mere 7-8x

The Subsidiary itself could be worth 25-30x Minimum

Seems Minority interest is taken care of in this transaction

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (10-01-2024)

Official statement. [[ will delete if doesn’t add much value ]

Pretty odd that company of such a magnitude will do such things to save 1000cr

Natco Pharma: Focusing On Complex Products (10-01-2024)

Just a cent: In my opinion, we will get better price if one waits for quarterly results. This will clear all the uncertainty.

Disclosure: Not invested. Keeping an eye.

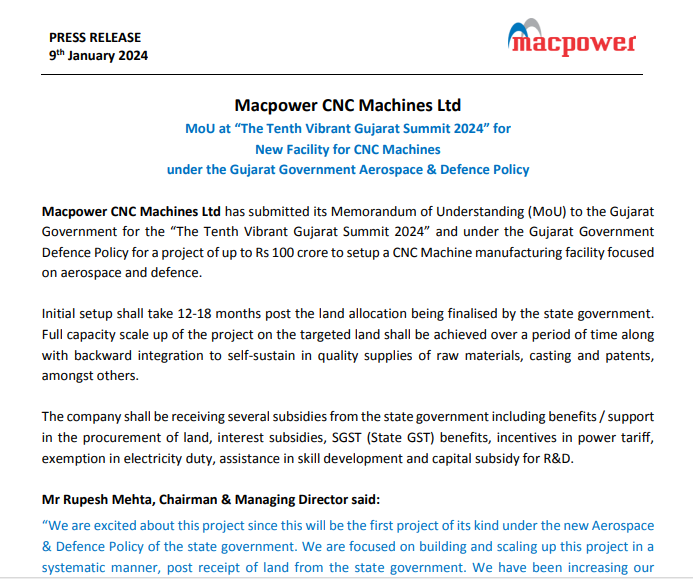

Macpower CNC Machines: Manufacturing a Strong Growth? (10-01-2024)

Coming up with a new faclity for aerospace and defence which will be 4 times of current capacity.

Some rough calculation on Macpower CNC:

-

Their average blended realization is 19 Lakh per machine which is likely to increase as they sell more high value machines (4 axis and 5 axis machines).

-

Jyoti CNC (recent ipo) has an average realization of 27 Lakh.

-

Macpower realization can also increase to 21-22 Lakhs.

-

Hence at peak utilization, macpower can do 440 Crore of revenue (22 Lakh * 2000 Machines). I assume they can do the peak revenue by FY26.

-

At 15% margins they can generate ebitda of 66 Cr (FY26) vs 21 cr in FY23

Now let’s look at the bigger picture

-

The new facility will be 4x of current facility (i assume new facility will have the capacity of 8000 machines)

-

Jyoti CNC has an order book of 3300 cr, primarily into Aerospace & Defence which required 4-5 axis machines.

-

Jyoti CNC mentioned this new order book will have blended realization of 50 Lakh (as Aerospace & defence are a higher realization segments)

-

Macpower’s new facility will also cater to aerospace & defence. I assume the blended realization for macpower will increase to 40 Lakh (assuming less then Jyoti).

-

At peak utilization Macpower will be able to do the revenue of 4000 cr (10000 Machines * 40 Lakh).

-

Assuming 20% margins due to operating leverage. It can do EBITDA of 800 cr.

-

Even we estimate lower PAT growth then the EBITDA growth due to higher depreciation or interest cost.

-

PAT can be 500-600 Cr (Current market cap is 700 Cr)

Now the only question is when?

Note: These are my rough estimates, actual estimates could be very different from this. I could be biased, please make any decision as per your analysis.

https://x.com/Alazyinvestor13/status/1744762935988384207?s=20

Ranvir’s Portfolio (10-01-2024)

Some interesting opportunities in an otherwise ’ not so cheap ’ market –

Bajaj Auto – Pulsars, 3-Wheelers, Chetak ( EV ), KTMs, Triumph JV – all doing well. Exports are holding steady. Company is likely to come out with revolutionary – CNG motorcycles in CY 25

Have cash on books > 26000 cr !!!

Have announced a stock buyback for an amount of Rs 4000 cr @ stock price of upto Rs 10,000 / share

ABSL AMC, UTI AMC – both are non capital intensive, cash rich businesses. With monthly SIPs showing no signs of a slowdown … these stocks can easily get re-rated upwards

Supriya Lifesciences – Have done well in H1, FY 24. Company is extremely positive wrt its sales outlook in Latin America as these countries are openly preferring India for incremental supplies of APIs over China. Likely to do a sales of around Rs 550 cr this yr. Confident of doubling their sales inside next 4 yrs

Disc – holding all, biased, not SEBI registered

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (10-01-2024)

Of course, which company will accept by themselves and agree to tax evasion? Nevertheless, Som Distelleries share price has stuck in the same range for a long time. Investors certainly don’t like uncertainty ![]()

Still, I can make no predictions about the share price, nor if the company actually will get any major penalty. Many promoters have done insider trading in the past using their in-laws, and still got away with that.

I am invested but ready to hop off at the first sign of trouble. But not rumors!

Hitesh portfolio (10-01-2024)

You can ask chatGPT about it, if it is difficult to comprehend on your own

Polycab India ~ Connection Zindagi Ka – W&C, FMEG and EPC Player (10-01-2024)

https://x.com/sahilbhadviya/status/1745117515628613681?s=20

BIG BREAKING Polycab – Income tax confirms Polycab has made unaccounted cash sales of around Rs. 1,000 crore which are not recorded in the books of accounts. Evidences of unaccounted cash payments of more than Rs. 400 crore made by a distributor, on behalf of the flagship company towards purchases of raw materials, have also been seized.