Posts tagged Value Pickr

Mann’s Portfolio (06-01-2024)

Hey i dont know about compuage info but yes redington is the distributor and not the Brand licensee of Apple

Creative is Brand licensee of Honeywell

Their Enterprise bsuiness is kind of overlapping with Redington but still Creative is National Distributor it passes down the product in Value chain

Where as redington sab khud karta hee

Tbh in electronics component there is literally no one doing brand licensing

Hence you’ll not find core competitor → To understand the business model go through Page ind or Jubiliant foods

If you see tradtional business model you can say 50% Overlap with redington

I’m sorry your intepretation about the Credit rating is wrong Creative has it’s chain of distributor network that follows the supply path for almost every products in their portfolio

And hence the customer conventration

Honeywell’s business is mere 10% of revenue

They have vision to scale upto 2500 – 3000 crores of revnue even by 2030

See the moat is simple – Honeywell wont come to india and sell this white goods – Investement chaiye, Forex Risk, Credit Risk, Operation ka karcha and much more.

Hence Brand licensee – The audit of honeywell and its clearence required 2 years for creative

Switching time is very very very High

This is the moat in my opinion

The board seems quite competent

PE Is percperation of growth in earnings

Is the blended margins become 2x from 2% to 4%

The Profit CAGR Is very Hugh and hence highh PE

Go through earnings call in my opinion

Disclaimer – Invested and Baised

Krsnaa Diagnostics – what is the diagnosis? (06-01-2024)

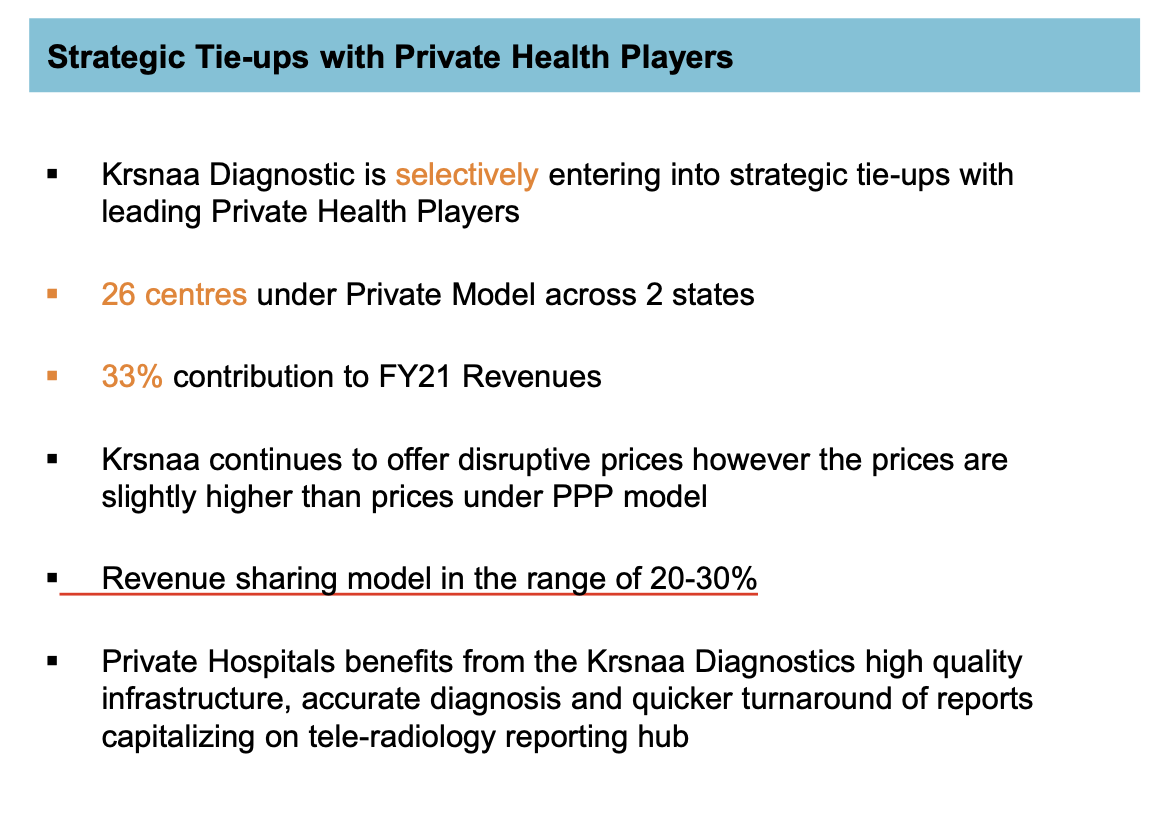

Yes, it includes two things. 1) the revenue sharing with these hospitals 2) they work with the local partners in remote areas on revenue sharing model. Management had clarified this in one of the calls. I suspect that out of INR 80-100 crore, second portion (revenue sharing with partners) would be more than revenue sharing with hospitals.

On this accounting policy, i think it’s standard across diagnostics companies. Even for franchisees, they recognise the revenue on gross basis and record the revenue shared with them as ‘Fees to channel partners’ or something like that. Krsnaa also has similar revenue recognition policy for hospitals and business partners channel.

Krsnaa Diagnostics – what is the diagnosis? (06-01-2024)

this is what their accounting policy states about the same, cant quite understand what fees would Krsnaa be paying to hospitals!

Krsnaa Diagnostics – what is the diagnosis? (06-01-2024)

Yash bhai, there is an expense line item of ‘payment made to hospitals’ if you see – which has been in the range of 80-100 crore over the past 4 years. What would this be for?

Krsnaa Diagnostics – what is the diagnosis? (06-01-2024)

Good point on the teleradiology. Yes, it’s essentially x-ray (they mentioned x-ray against teleradiology in DRHP and later changed to ‘teleradiology’ in presentations but it remains the same). Agree on the view that this will not move the needle for them. They recently aligned the reporting so now the CT/MRI centers and no. of machines are the same. It’s good that they made it easy to understand now.

On the sharing with hospitals, I think it’s basis revenue (they have mentioned in one of the presentations). Their pricing for private hospitals also go up by 20-30% to cover this revenue sharing.

ValuePickr- UAE (Dubai) (06-01-2024)

Hi,

Thanks for taking this initiative. I am also based in Dubai and interested in joining the group. I have investment in Indian equity market and have passion for direct investment in equity. Appreciate if you please include me in the group. Thanks. Samir Ghosh.

Mann’s Portfolio (06-01-2024)

Read its credit rating looks like 60% revenue will be coming from honeywell business, (correct me if my interpretation is wrong),

I was going through the DRHP and found its two listed competitors .

Looks like compuage infocom is facing serious headwinds attaching its credit rating and redington has historically traded at PE around 10-15 so Creative Newtech’s PE at around 35 is maybe because of their changing business model from low margin distribution business to contract manufacturing of honeywell business.

Their brand share seems to have evolved as in 2017 in their RHP majority share was of Sony, Samsung and LG, I see they have brands which are niche which could command better margins IMO.

The promoter is an IIM bangalore Alumni and has good experience but do they have the capability to do contract manufacturing for more brands is my question. Currently reading about the history of the company and trying to understand their MOAT would appreciate your input.

Krsnaa Diagnostics – what is the diagnosis? (06-01-2024)

Also, if you compare the number of CT/MRI machines owned and the number of CT/MRI Centers operated theyre the same. Hence, Teleradiology to my interpretation is essentially XRay machines installed at Primary/Community health centers wherein these scans are sent to the hub in Pune. Also, teleradiology realizations of 90-100/test point toward that. And something I believe, will not be the needle changer in this story

Krsnaa Diagnostics – what is the diagnosis? (06-01-2024)

@yashrachh could you help me also understand this expense that Krsnaa shares with hospitals? Is it basis/test or is it as a fixed fee or a fixed %age of revenue?