Single property was only for comparison purposes. Advani Hotels did have the upper hand as the property is based out of the most favoured holiday destination.

Posts tagged Value Pickr

Aster DM healthcare (03-01-2024)

* From an industry perspective, you could look at other similar companies (my review was EV/EBITDA is of the magnitude of 18-40). So on a relative basis looks fairly valued to undervalued (depending on what multiple you use). Once detailed historical financials for India business are available, should be possible to understand DCF basis

Narayana Hrudayalaya Ltd

EVEBITDA 21.5

Operational Beds – 6096

Founded – 2000 – 24 year ago.

Compared to Aster India

EVEBITDA – Valued more than NH post demerger

Operational Beds – 4080 (India – other than Kerala it is Asset light)

India operation started around 2014.

Key aspect is Aster yet to establish out side Kerala which enjoy its GCC brand recall.

My one cent is India business is unfavorable.

Pragnesh’s portfolio (03-01-2024)

Please go through this thread

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (03-01-2024)

A couple of points:

(1) On.Energy storage, batteries may be preferred for storage of small amount of energy… However for grid scale where large amount of energy to be stored, the emerging trend is to go for hydro pumping storage due to low cost , 50-100 years life cycle and no import content in construction where as lithium ion batteries are expensive with import content would be bulky for mega energy storage, batteries would require frequent maintenance and low life cycle of batteries.

(2) On electrolyser,/ fuel cell, a lot of developments taking place very fast and RO water may not be required.

SmallCap Hunter : Trying to find the dark horses with triggers (02-01-2024)

What’s the thesis behind the single property selection? Did you dive deep into Advani hotels?

Ambika Cotton Mills (02-01-2024)

Ambika Cotton Mills

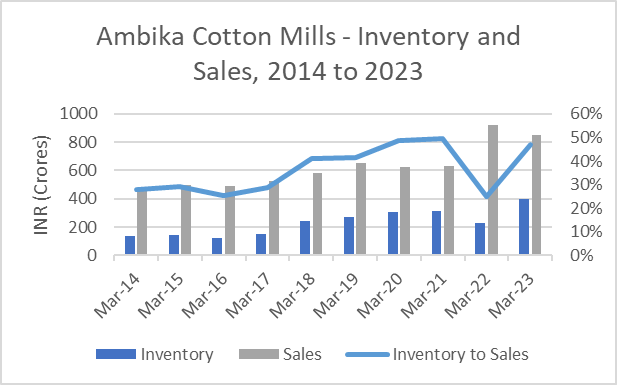

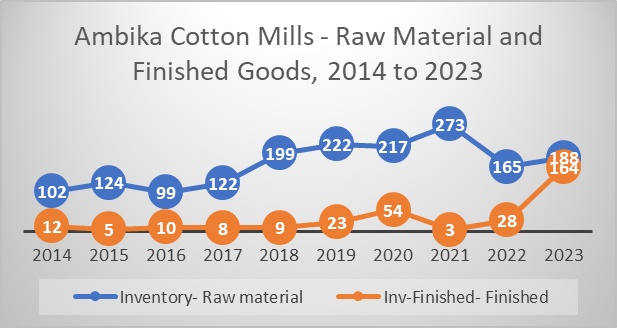

I have been looking at the charts of Ambika Cotton Mills and Cotton prices. Prices seem to be moving in perfect correlation with cotton prices except for a deviation in 2014. The company has been existence for a very long time and has gone through many difficult cycles. The company is known to have maintained inventory levels quite well in the previous cycles.

I tried to plot how inventory has changed with cotton prices. Just wanted to know how well the company has managed the inventory over the cycles. Inventory has increased over the years as sales has. So I plotted Inventory to sales over the years. Inventory to sales has remained the lowest in 2022 when cotton prices were at the peak point. Also to be noted the inventory especially raw materials were at the highest point in 2021 when cotton prices began to increase. However, one significant difference that I have noticed this time was the increase in finished goods inventory. Every year until now finished goods inventory was only a small share of overall inventory. However, the finished goods inventory has significantly increased this time around.

The company may be finding it difficult to sell its finished inventory. Noticed the chairman saying in the AGM that they are not selling at lower margins to increase the sales. Inventory has further increased in half year from 397 crores to 498 crores.

Inventory may go increase further going forward until the cycle reverses. Most of these inventory would be yarns and other related items which has a high shelf life. Similarly, the company doesn’t have to worry about the style or anything of that sort which should affect the selling price once cycle reverses. I think the strong cash position is one of the company’s competitive advantages. The company can still run business as usual, even if cotton prices fell further. The company is run like a traditional business with focus being solely on the core business. That could be one of the reason why company was not very positive on buybacks. The company never had a lot of cash on their balance sheet until 2022, and they are already in a poor cycle. So the next time cycle reverses the company may have to look for better utilization of cash. Also, the current market rates are good as well. The company had an interest income of 5 crores in the current quarter, so the return on the cash is not very bad either.

Jkil — jkumar infraprojects (02-01-2024)

https://www.screener.in/company/JKIL/

Agree. Some marquee names like Sunil Singhania Abbakus , Prashant Jain ex HDFC MF 3P Capital, HDFC MF with big 9% stake , Mukul Agarwal invested in it.

Double engine govt focussed like laser on infrastructure projects specially urban infra projects.

CLSA report is quite detailed one.

Jkil — jkumar infraprojects (02-01-2024)

As per my estimates, based on management guidance of Revenue and Margins, PAT will touch 700cr by FY27 from 275cr in FY23…

Despite all the negative news-flow over the years and sceptical perception which many have towards this company, it has continued to deliver solid, consistent numbers, with 15% YoY growth, over the last 12 yrs…thats why some of the best value investors and fund managers have sizeable stake in it. Porinju once called it the mini L&T 3 years back in one of the conference calls.

I feel current Mcap of ~4500cr should reach 10,500cr in couple of years (March 26) at which point the company will trade at 15 times forward (March 27) PAT of 700cr.

Eicher Motors (02-01-2024)

@laxman_sreekumar just like you, Eicher motor has one of the highest allocations in my PF.

- If some one is purchasing a motorcycle above 350cc, they are like an iPhone, if you don’t buy it, people ask, why not royal enfield when you were spending so much? The loyalty they command is amazing

- The new engines are likely to fork even more variants bringing economies of scale.

- They are slowly building muscles outside India

- Their apparel and accessory business if amazing