Have been holding Edelweiss greater china for 5 years now and bought a small quantity of axis greater china 1 year ago… day to day volatility of edelweiss is more but seems to capture the upside better… also as per morning star data the underlying JP.morgan china fund is tech heavy…

Posts tagged Value Pickr

PGINVIT impairment of investments in subsidiaries and book value (29-12-2023)

This assumes no asset addition on top of the 5 transmission lines they already have a 74% stake in.

PGINVIT impairment of investments in subsidiaries and book value (29-12-2023)

Why do you think its not sustainable given the current assets. Where will the money leak? the price of transmission will escalate with inflation if it not already built into the pricing. Secondly, even if they dont escalate Rs 12 dividend looks steady unless management says so. Last quarter the management had to dig in about few paisa ( i believe they took 10-15 paisa from reserve to meet their stated Rs 3 per quarter goal). I dont think management is smart in quoting a yield ahead of time when so many variables could impact cost. They should instead talk about long term PPAs etc so that investors get visibility into future cashflows.

As i see it, its a good place to park cash and get 9-12% yield and if govt bond rates go down then this stock will rally as it provides a much higher yield. So if govt rates stay put u get paid a good yield but if govt rates fall u get capital appreciation too.

Management quality is good since these are PowerGrid guys with experience. Holding for 20-25% gain in capital while collecting 12% yield.

Priti International Ltd (29-12-2023)

I didn’t understand why Priti’s margin should be less than its suppliers. Supplier is in a commodity business. Priti is selling finished goods b2b and b2c (online and retail outlets). Increase in B2C should only increase the overall margins.

What I see as a major differentiator between Priti and competitors is their ability to execute. Priti started in around 2007 and made its way in an area where differentiation is really difficult and where there were established players.

Also, handicraft products – They have handicraft products in their product mix. This segment is labour intensive and fixed assets are not required.

Rajasthan has a lot of companies which are in wooden handicraft business but most of them are not listed. Handicraft is a hit or miss business. Its about securing good buyers in Europe or America.

BEML – Disinvestment (29-12-2023)

Both stocks are up about 35-50% from last discussion. No news but just market run up. Not the time to be greedy. Time to take profit and get on the sidelines till it falls down or if new news comes.

Wockhardt: an NiCE story (29-12-2023)

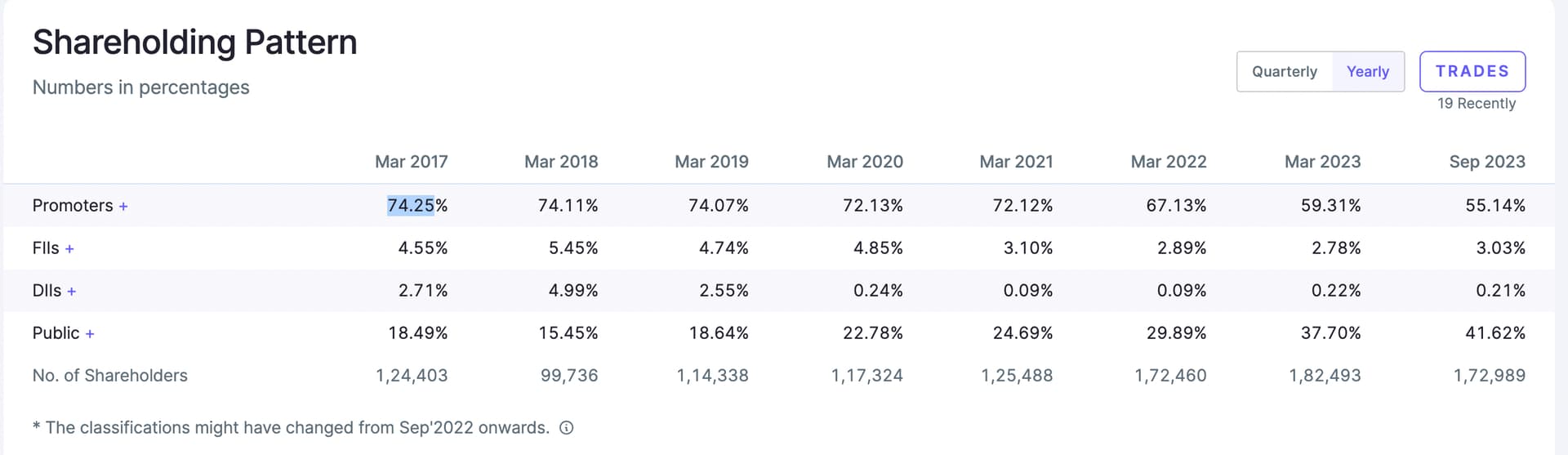

Why promotors are selling like crazy? Over the past 5yr the shareholding reduced from 75 to 55

KDDL (Ethos Watches) – Scalable business model at an inflection point? (29-12-2023)

Mohit Ji, May I request you to please share the link of above Transcript

Bhagiradha Chemicals & Industries Ltd – Growing AgroChemical Company (29-12-2023)

ABOUT

Bhagiradha Chemicals & Industries is an Agro Chemical Company in India involved in the manufacturing of insecticides, fungicides, herbicides, etc. It was Promoted by the late Sri S. Koteswara Rao, a former scientist of the Indian Institute of Chemical Technology, Hyderabad in the year 1993.

KEY POINTS

Product Portfolio

The company’s product portfolio includes a wide range of insecticides, fungicides, herbicides, and specialty intermediaries –

a. Insecticides: Chlorpyrifos, Diafenthiuron, Fipronil, Buprofezin, etc.

b. Fungicides: Azoxystrobin

c. Herbicides: Imazethapyr, Clodinafop-propargyl, Cloquintocet-mexyl

d. Specialty-intermediaries: R-HPPA, 2,6-Dichloroaniline, etc

Product Concentration

The co. has over twenty products and expertise in other processes, the revenue streams of the co. however, are concentrated on four products which together contributed 84% of the gross sales for the co. in FY22.

Export Presence

The co. exports its products to various countries viz. USA, Brazil, Columbia, Argentina, Mexico, Costa Rica, Germany, UK, France, Portugal, Italy, Israel, Turkey, Iran, Indonesia, Taiwan, Malaysia, New Zealand, and Australia. In FY23, exports accounted for ~11% of overall revenues v/s 24% in FY22.

R&D Capabilities

The co. has an established R&D division located at the factory premises, which the Ministry of Science & Technology (GOI) also recognizes. BCIL spends about Rs 1.50 crore for R&D every year (Rs. ~4 cr in FY23). It has successfully commercialized three insecticides, namely, Fipronil, Pymetrozine, and Dinotefuran. During FY23, two Indian patents have been granted to the co.

Manufacturing Capabilities

The co. is operating its manufacturing facility in Cheruvukommupalem, Ongole, Andhra Pradesh. More than 60% of the 71.68 acres of factory land is an open area covered with a green belt and its three production blocks cater to five process lines, utilities, a quality assurance block, a warehouse, an R&D facility, etc. It has a capacity of 3250 MTPA of chemicals.

Capacity Utilization

During FY22, the co. achieved a capacity utilization (CU) of ~80% compared to ~70% in FY21.

New Facility

The co. had signed an MOU with the Government of Karnataka for setting up a manufacturing unit in Kadechur industrial area, Yadgir Dist., Karnataka, through its WOS- Bheema Fine Chemicals. The project is expected to be completed in three phases at an estimated cost of Rs 350 crore. This new unit will roll out commercial production by FY25.

Strategy

The co. is aiming to have registration approvals in place during FY24 for a couple of products that have commercial potential and also focusing on improving its overseas footprint with new strategies.

Sales are increasing

EBITDA margin is stable

EPS is growing

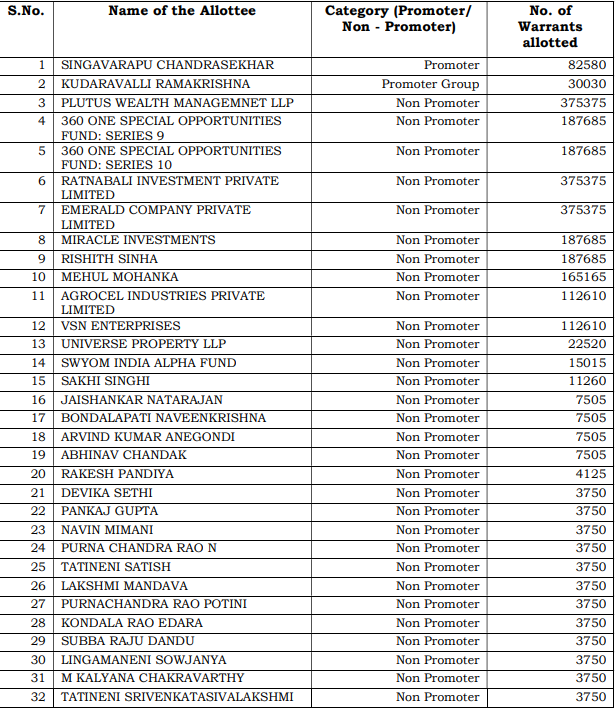

In a recent company do allotment of 25,61,425 Convertible warrants for the company’s expansion

-

In this allotment MEHUL MOHANKA who is MD of TEGA INDUSTRIES also invested.

-

In this expansion company says that they will achieve 1200 cr revenue in three years(the recent highest revenue was 500 cr in FY23)