The listing date has come… from today the aluminum casting division is going public.

SUNCLAY.pdf (1.5 MB)

Posts tagged Value Pickr

Sundaram Clayton (29-12-2023)

Atam Valves Ltd (AVL) (28-12-2023)

Q2 FY ’24 Concall notes

-

Infrastructure and Team:

- Multi-capability manufacturing infrastructure.

- Dedicated team of 500 professionals.

-

Clientele:

- Serving industries including oil and gas, refining, petrochemicals, marine, mining, and more.

- Over 300 clients, with top 15 contributing 80% of sales.

-

Market Presence:

- Actively planning expansion into the production of large-size valves.

- Presence in India, South Africa, USA, UK, and Indonesia (3% international presence).

- Expanding to the United Arab Emirates, Saudi Arabia, Tanzania, Kenya, Russia, and Canada.

-

Global Market Trends:

- Industrial valves market projected to reach $99.8 billion by 2028.

- Opportunities for growth driven by healthcare, pharmaceutical industries, smart cities, and connected networks.

-

Strategic Initiatives:

- Extensive distribution network across India.

- Pursuing opportunities in the US market through strategic partnerships.

- Forward integration into bathware items under the brand Daley.

-

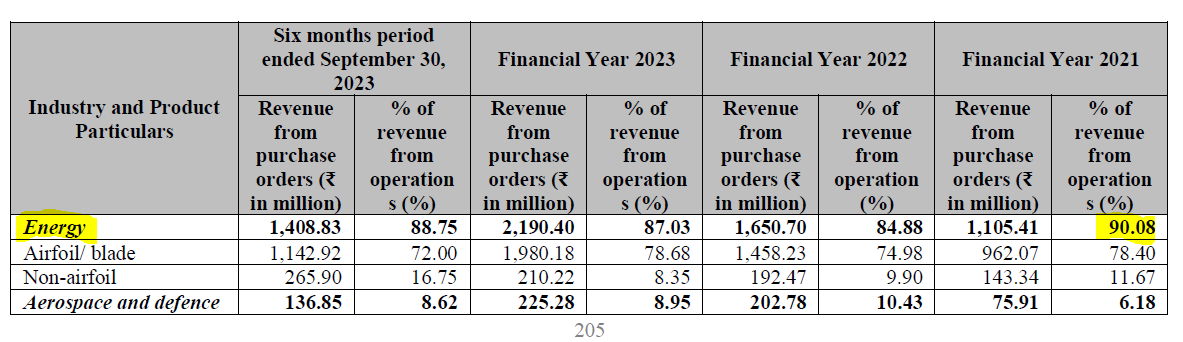

Financial Highlights Q2 FY24:

- Total revenue: INR12.76 crores.

- EBITDA: INR2.36 crores (EBITDA margin 18.70%).

- Profit after tax: INR1.30 crores (PAT margin 10.34%).

-

Financial Highlights H1 FY24:

- Total revenue: INR23.17 crores.

- EBITDA: INR3.89 crores (EBITDA margin 16.80%).

- Profit after tax: INR2.16 crores (PAT margin 9.32%).

-

Outlook and Future Plans:

- Optimistic outlook based on strong Q2 performance and strategic initiatives.

- Consistent growth and financial stability for continued success.

Revenue Target for FY 2030:

- Target: Achieving INR 1,000 crores by FY 2030.

- Caution against assuming a consistent 50% CAGR year-on-year.

- Acknowledgment of challenges due to new product launches and market expansions.

FY24 Revenue Guidance:

- Revenue target for FY24: At least INR 80 crores.

Working Capital and Receivables:

- Strategy: Developing new products and entering new markets.

- Reason for higher receivables: Offering credit to gain market acceptance.

- Working capital days: Expected to decrease by the end of the year.

- Positive market response.

Utilizing Indian Distribution Network for Global Expansion:

-

Canada Market Entry:

- Engaging with a prominent client in Canada.

- Awaiting API certification for their brand.

- Potential to penetrate the Canadian market and cater to petroleum industries.

-

Product Portfolio Enhancement:

- Planning a new plant for manufacturing larger valves.

- Aim to broaden the product range and cater to diverse industry needs.

Geographical and Sector-Wise Revenue Breakdown:

-

Geographical Focus:

- Strong presence in Gujarat with own warehouse and direct sales.

- Robust distribution network in Karnataka.

- Significant market share in Haryana, especially among boiler manufacturers.

-

Sectoral Contribution:

- Existing range and upcoming plant cater to diverse sectors.

- Emphasis on targeting industries like petroleum with the new product range.

Future Market Strategy:

- Focused expansion in Canada as a strategic move.

- Leveraging existing success in Gujarat, Karnataka, and Haryana to propel growth.

- Continued efforts to diversify and strengthen the product portfolio for sector-wise growth.

Expansion and Commencement Delays:

-

Reason for Delay:

- Delay in starting the bathroom faucet plant.

- Shift from Q2 to Q4 of FY24.

-

Decision and Strategy:

- Focus on expanding existing product range first.

- Concentration on the Canadian market opportunity.

- Opting for an asset-light approach for bathroom faucets.

Capex and Expansion Plans:

-

Capex Confirmation:

- Capex required for the new factory for bigger valves.

- Working capital needed for importing bathroom faucets.

- Expansion shift from bathroom faucets to larger valves.

Margins and Sustainable EBITDA:

-

Margin Pressure Explanation:

- Margin reduction due to market penetration and increased marketing expenditure.

-

Sustainable Margin:

- Anticipated sustainable EBITDA margin: At least 12% to 13%.

- Expectation of improvement in EBITDA.

Revenue Growth and Pending Orders:

-

H2 Revenue Growth:

- Expectation of substantial growth in H2, typical for the industry.

- Confidence in achieving the INR80 crores target.

-

Pending Orders:

- Ongoing process with dealers contributing to a regular flow of orders.

- Approximately INR60 crores in pending orders.

Dealer Network and Top Clients:

-

Dealer Network:

- Current dealer network: 750 dealers across India.

-

Top Clients Contribution:

- Top 15 clients contribute 80% of sales.

- Continued strategy with an 80%-20% ratio (Top 20 client, 80% sales)

Product Launch and Marketing Strategy:

-

Bathroom Faucet Launch:

- First shipment expected in January.

- Initial launch in Gujarat and Karnataka.

-

Marketing Strategy:

- Targeting contractors and builders.

- Focusing on those already dealing with plumbing segments.

- Premium segment faucets with an estimated 25% margin.

Return on Investment (ROI) for Capex:

-

New Unit for Bigger Valves:

- Anticipated breakeven in three to four years.

- Certification process completion crucial for engaging larger clients.

Navigating Challenges and Leveraging Opportunities:

-

US Market Strategy:

- Secured a Canadian client’s brand for manufacturing and selling.

- Utilizing their established brand recognition in the US market.

- Leverage existing partnerships to gain entry into other markets.

North American Market Strategy:

-

Manufacturing Model:

- Products to be manufactured in India.

- Canadian brand to act as the sole customer for North America.

- Marketing in North America to be done through the Canadian brand.

Risk Factors and Growth Outlook:

-

Perceived Risks:

- No significant risks identified in the valve line.

- General market downturns and currency fluctuations acknowledged.

-

Growth Outlook:

- Optimistic about growth due to the introduction of innovative products.

- Over 25 years in the industry without significant setbacks.

Product Focus for North America and Saudi Arabia:

-

Product Line for Target Markets:

- Initially focusing on industrial valves for both North America and Saudi Arabia.

Working Capital Requirements:

-

Additional Working Capital:

- Anticipating the need for INR30 crores for both new unit capex and importing bathroom faucets.

API Certification and Market Entry:

-

API Compliance for Market Entry:

- Working towards API certification for compliance.

- Expected certification completion in approximately two months.

- Plan to start supplying to the Canadian brand in Q4.

Sales Order and Market Interest:

-

Initial Sales Order:

- First order expected to be around $2 million.

- Aiming to build trust and satisfaction for future collaborations

Export Margins:

-

Expectation:

- Anticipating better margins in exports compared to the domestic market.

Timeline for Increased Export Revenue:

-

Target Year:

- Aiming for 23% of revenue from exports in two years.

- Projected achievement in FY ’26.

IDFC First Bank Limited (28-12-2023)

Can you share specific calculations on how you came to about the 10-11% arbitration value gap? My calculations resulted in about a +35% gap.

MTAR Technologies – A wager on innovation meeting economies of scale (28-12-2023)

Azad business is entirely different from the MTAR.

Azad supplies components for Turbines and Aerospace OEM’s. Turbine components business contribute 90% of their revenue with high customer concentration as there are only few turbine makers globally.

Easy Trip Planners (Easemytrip) – An outlier in OTA (28-12-2023)

I don’t think that there is any need of fund raise, management claim that they are cash rich company but still diluting the equity.

KPIT – CASE (connected, autonomous, shared, electric) – Focused Automotive Play (28-12-2023)

Jubilant, PG health, Gillette, Bajaj Finance, Asian paints and Titan (has been largely above 40). There quite more. But you have to make a good entry to be on a safe side. And as I said I entered before many and will ride till trend bends.

Ronak’s Portfolio – building it slowly (28-12-2023)

Thank you VP members for all the help and guidance through out the year.

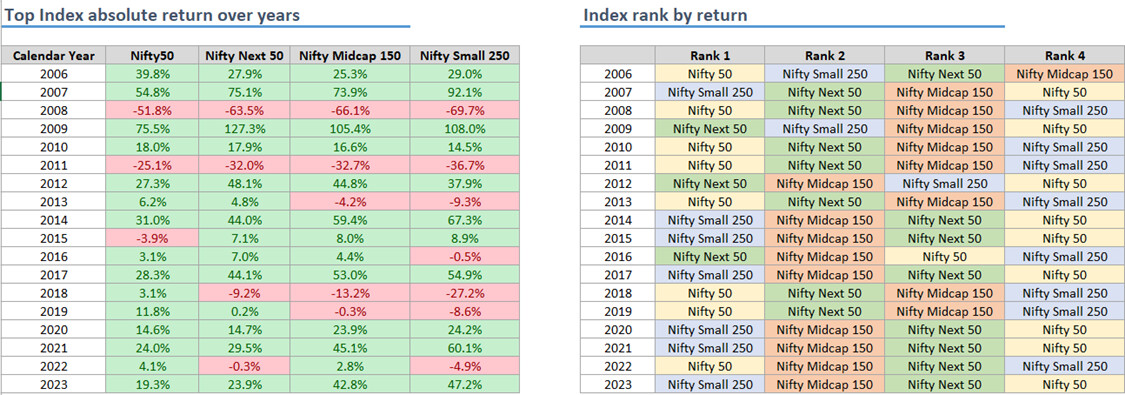

All the index performing well this year. After 2011 , this is almost 12th year where nifty end the year on positive note. Midcap and Small cap leads the overall performance.

| Category | Percentage |

|---|---|

| Stock | 19% |

| Equity MF | 16% |

| Debt MF | 36% |

| FD | 7% |

| Gold | 3% |

| Cash | 7% |

| Other | 13% |

I haven’t made any major changes in allocation, continuing my SIP and allocating additional funds to a Debt fund while increasing cash holdings.

This year I was focusing on consolidating everything be it MF or portfolio. Still not seeing too many opportunities in the market hence going slow but at the same time don’t want to sit outside completely as well.

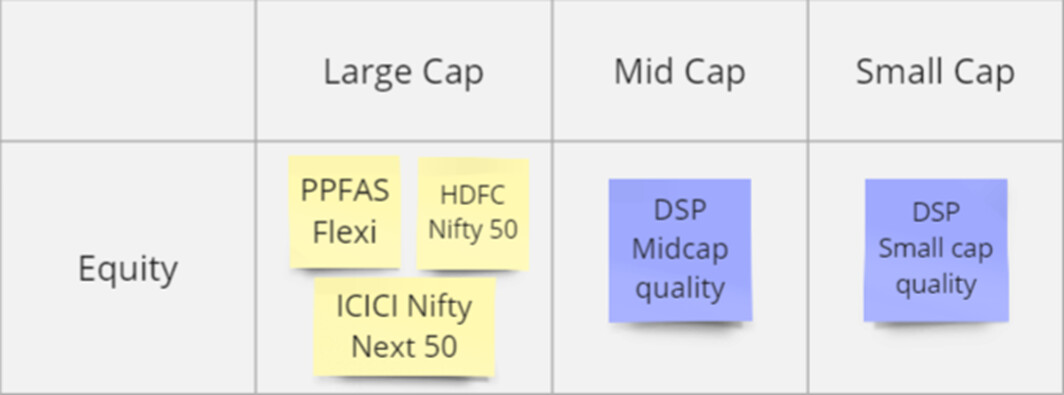

MF Portfolio:

DSP launched quality small cap fund and at the same time Pankaj Tibrewal quits Kotak. So I have booked all the profits in small cap of Kotak, HDFC & DSP. Anyways I am more comfortable with index fund for long term so moved into DSP quality small cap fund

Equity Portfolio:

I exited positions where the allocation was too low or targets were achieved, reducing the number of stocks to only 11.

I made several exits, even in cases where conviction was high but allocation remained low. Other reasons for selling included reducing exposure in specific sectors, promoter groups, or due to high valuations. The stocks involved in these exits were Devyani, LTTS, UBL, USL, Apcotex, RBA, TTK Prestige, Syngene, Bajaj Finserv, TCS, Dr. Lal, and HDFC.

Make a lot of exits even though in some cases where conviction was high but allocation was low. Some other reasons are to decreasing allocation in sector or promotor group or valuation. Such names are Devyani, LTTS, UBL, USL, Apcotex, RBA, TTK Prestige, Syngene, Bajaj Finserv, TCS, Dr LAL, HDFC.

Although no major changes in core holdings, in fact increased position in those stocks.

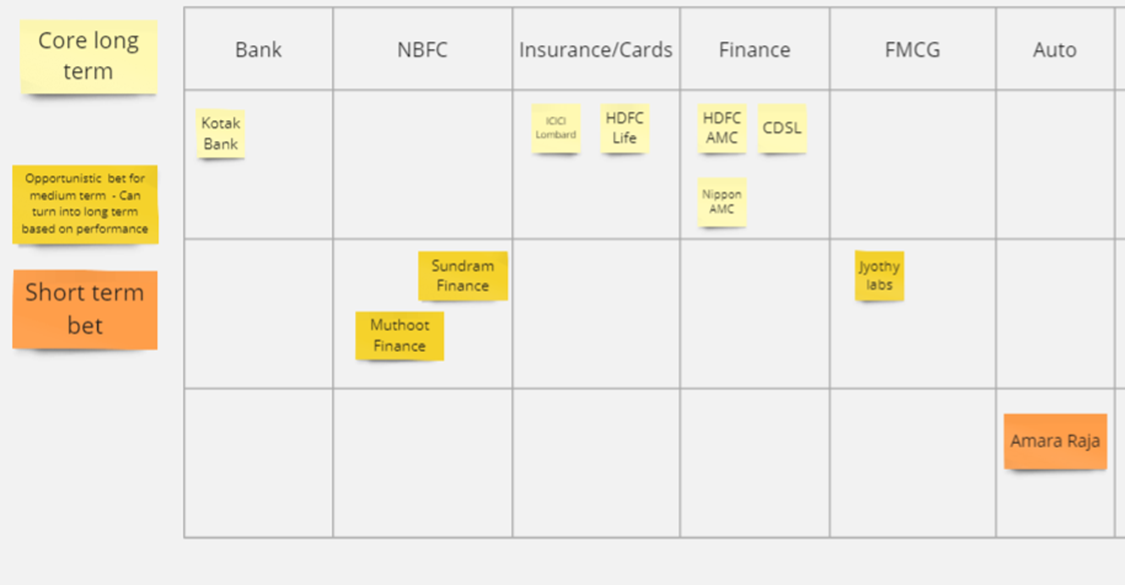

| Sr No | Ticker | Inv Price | Curr Price | Allocation |

|---|---|---|---|---|

| 1 | NSE:ITC | 206 | 464 | 20% |

| 2 | NSE:HDFCLIFE | 559 | 648 | 16% |

| 3 | NSE:ICICIGI | 1,232 | 1,438 | 16% |

| 4 | NSE:HDFCAMC | 2,018 | 3,203 | 12% |

| 5 | NSE:KOTAKBANK | 1,787 | 1,920 | 11% |

| 6 | NSE:MUTHOOTFIN | 1,017 | 1,490 | 5% |

| 7 | NSE:SUNDARMFIN | 2,336 | 3,541 | 4% |

| 8 | NSE:NAM-INDIA | 224 | 435 | 3% |

| 9 | NSE:CDSL | 1,026 | 1,835 | 4% |

| 10 | NSE:JYOTHYLAB | 206 | 483 | 4% |

| 11 | NSE:ARE&M | 610 | 820 | 5% |

I know that I am currently making a lot of changes but as I said, I am in learning phase. I am becoming more comfortable with certain type of businesses. Allocating 0-1% wasn’t yielding any rewards, even when I was right.

I like to add more mid caps stocks as these companies reached a certain scale and at the same time, they have long runaway for growth. But almost all the stocks in FMCG, IT, QSR, FMEG, new age sectors are currently trading at more than 60-70 PE, so not comfortable at the moment to add.

I will focus on large cap stocks for now and consider adding small/mid cap stocks when suitable opportunities arise.

RACL Geartech Limited (28-12-2023)

Five Rules (Pat Dorsey Page 89) probably this will help you understand. In case I am wrong others can rectify.

IDFC First Bank Limited (28-12-2023)

I checked the shareholding pattern of IDFC ICICI prudential was not a share holder there.

but it had 1.39% in IDFC first at the end of last quarter…

IDFC First Bank Limited (28-12-2023)

Hello ,

Can anyone please explain the impact of the profit and growth on back of the news that came out day RBI requesting few banks (Including Equitas, IDFCF) to reduce credit to deposit ratio to below 75 % ?