Valuepickr rocks. Great learning with huge earnings

Posts tagged Value Pickr

Yash Pakka – (Previously Yash Paper) – Rising from ash (28-12-2023)

What is the status of pledged shares?

RACL Geartech Limited (28-12-2023)

RACL Geartech –

Q2 FY 24 highlights –

Sales @ 103 vs 90 cr

EBITDA @ 25 vs 23 cr ( up 9 pc, Margins at healthy 23 pc )

PAT @ 10 vs 10 cr

Product range –

Transmission gears and Shafts, Sub assemblies

Precision Machined parts

Chasis parts

Industrial gears

Product applications –

2, 3 Wheelers, TVs, CVs, Agri eqpt and industrial gears

Manufacturing facilities – 02

Warehouses – 03 in Europe

Comments from Concall –

Expanding Noida facility with additional leasehold area of 26k sq ft. Commercial production to start from Q1, FY 24. Samples shall be produced in Q4 this yr

Nominated for supply for gearboxes and shafts for a German electric- bicycle player. To be made at the new expanded facility. These are premium bikes costing around 5-7k Euros. These kind of bikes are gaining huge popularity in Europe. The German customer has a patent protected technology for this bike.

Nominated for supply of wheel axle for KTM Austria for their 1300 cc super bike

Another customer of the company – MAN Trucks had some of its projects delayed in the current FY. Company supplies transmission gears and axle shafts to them. By Q4, supplies to MAN trucks should begin. Supplies to MAN should be a big growth driver in FY 25

For FY 24, growth guidance has been moderated to 15-20 pc from earlier guidance of 25 pc. Should go back to 25 pc kind of growth rates wef FY 25. Reason for the same is because the company could not get its hands on gear-grinding machinery ( very high end machinery ) due various supply bottlenecks and shortages in Europe and Japan from where they r imported. Most of the issues now stand resolved

In FY 24 – company is expected to spend 80 cr on Capex. FY 25’s capex plan has not yet been finalised

The newer orders that company is getting have greater degree of value add. Hence there is an upward bias in gross margins

Company’s supplies to BMW’s R-1200

( upgraded now to R-1250 Bikes ) is a high margin, high value addition business. Its likely to continue that way till 2033 !!!

KTM has expanded into China and is doing good business there as well. RACL remains their supplier even for the bikes to be sold in China. This should help RACL grow with KTM

Still aim to hit the Rs 500 cr topline by FY 25 end while maintaining the same margins

The China + 1 sentiment and the high inflation and energy prices in Europe have been a tailwind for the company and other Indian manufacturing companies too

Disc: holding, biased, not SEBI registered

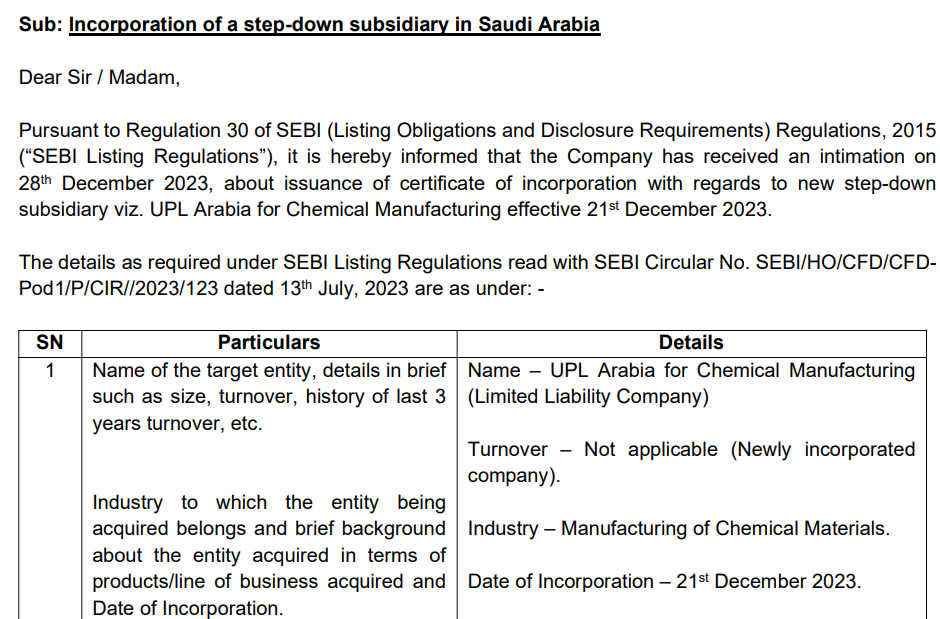

UPL Ltd – global agrochemical company (28-12-2023)

Incorporation of a subsidiary UPL Arabia. Not sure of the implications/rationale.

Ranvir’s Portfolio (28-12-2023)

RACL Geartech –

Q2 FY 24 highlights –

Sales @ 103 vs 90 cr

EBITDA @ 25 vs 23 cr ( up 9 pc, Margins at healthy 23 pc )

PAT @ 10 vs 10 cr

Product range –

Transmission gears and Shafts, Sub assemblies

Precision Machined parts

Chasis parts

Industrial gears

Product applications –

2, 3 Wheelers, TVs, CVs, Agri eqpt and industrial gears

Manufacturing facilities – 02

Warehouses – 03 in Europe

Comments from Concall –

Expanding Noida facility with additional leasehold area of 26k sq ft. Commercial production to start from Q1, FY 24. Samples shall be produced in Q4 this yr

Nominated for supply for gearboxes and shafts for a German electric- bicycle player. To be made at the new expanded facility. These are premium bikes costing around 5-7k Euros. These kind of bikes are gaining huge popularity in Europe. The German customer has a patent protected technology for this bike.

Nominated for supply of wheel axle for KTM Austria for their 1300 cc super bike

Another customer of the company – MAN Trucks had some of its projects delayed in the current FY. Company supplies transmission gears and axle shafts to them. By Q4, supplies to MAN trucks should begin. Supplies to MAN should be a big growth driver in FY 25

For FY 24, growth guidance has been moderated to 15-20 pc from earlier guidance of 25 pc. Should go back to 25 pc kind of growth rates wef FY 25. Reason for the same is because the company could not get its hands on gear-grinding machinery ( very high end machinery ) due various supply bottlenecks and shortages in Europe and Japan from where they r imported. Most of the issues now stand resolved

In FY 24 – company is expected to spend 80 cr on Capex. FY 25’s capex plan has not yet been finalised

The newer orders that company is getting have greater degree of value add. Hence there is an upward bias in gross margins

Company’s supplies to BMW’s R-1200

( upgraded now to R-1250 Bikes ) is a high margin, high value addition business. Its likely to continue that way till 2033 !!!

KTM has expanded into China and is doing good business there as well. RACL remains their supplier even for the bikes to be sold in China. This should help RACL grow with KTM

Still aim to hit the Rs 500 cr topline by FY 25 end while maintaining the same margins

The China + 1 sentiment and the high inflation and energy prices in Europe have been a tailwind for the company and other Indian manufacturing companies too

Disc: holding, biased, not SEBI registered

Lloyds Engineering Works Limited (28-12-2023)

With a resilient INR 921 crore order book, (3X FY23 sales), Lloyds

Engineering Works Ltd (LEWL) envisions substantial growth, particularly

in Marine and Civil projects, promising heightened revenue and profit

margins. Strategically investing in capacity enhancement, LEWL solidifies

its financial position as a net cash entity.

Poised to thrive in the infrastructure and capex sector, LEWL strategically

aligns with the anticipated surge in government spending, demonstrating

a keen foresight in capitalizing on opportunities within this burgeoning

industry. Furthermore, through strategic technological collaborations

with industry leaders like The Material Works, Ltd. (TMW), Bhabha Atomic

Research Centre (BARC), and TB Global Technologies Ltd (TBG), LEWL is

poised to innovate and diversify its product portfolio, ensuring a

competitive edge in the evolving market landscape. LEWL is set to issue

6.34 crore equity shares, raising INR 99 cr at a price of 15.5 per share. The

purpose of this issuance is to secure funds for working capital needs.

We expect revenues to grow at a CAGR of 47% to INR 996cr.This

stupendous growth in revenue is expected from:-

• Higher order inflow from marine, steel and special civil engineering

projects.

• LEWL’s Strategic Capacity Boost for Future Revenue Growth

• Strategic positioning in the infrastructure and capex sector,

aligning with a government spending surge

LEWL’s EBITDA and PAT are expected to grow at a CAGR of 59%/66% to INR

209/168 cr respectively. EBITDA and PAT margins are expected to enhance

by 430/500 bps to 21%/16.8% respectively. Subsequently ROE and ROCE

are expected to enhance by 610/750 bps to 24.9%/22.9% respectively

We initiate coverage on LEWL at the CMP of INR 44 per share (28.3X FY26

P/E) with a price target of INR 71 (47x FY26 P/E) per share, representing an

upside potential of 61.4% in the next 24 months

Financial analysis and projections

FY21-23: Remarkable Revenue Growth and Operational Turnaround

Revenues

The company experienced a 111% CAGR in revenues, increasing from INR 70 crore in FY21

to INR 313 crore in FY23

Margins and Profits

Although the company faced operating margin challenges and incurred an EBITDA loss

of INR 10 crore in FY21. The loss was mainly on account of the economic slowdown as a

consequence of the COVID-19 pandemic. It successfully reversed this trend in FY22,

achieving an EBITDA of INR 5 crore, and further improved to INR 52 crore in FY23.

FY23-26E: Diversification, technological alliances, and capacity enhancement

for Enhanced revenues and returns

Revenues

We expect revenues to grow at a CAGR of 47% to INR 996cr.This stupendous growth in

revenue is expected from

Higher order inflow from marine, steel and special civil engineering projects.

• LEWL’s exclusive technical tie-up with The Material Works co (TMW) for Eco

Pickled Surface (EPS Gen 4) Technology grants a competitive edge, allowing

LEWL to capture a larger market share in India and Bangladesh by offering

advanced, eco-friendly pickling solutions, driving revenue growth.

• The strategic agreement with TB Global Technologies, Japan, positions LEWL to

expand its product offerings, tap into a broader market, and contribute to

Atmanirbhar Bharat, fostering revenue growth through diversified solutions and

increased market share.

• LEWL’s Desalination technology deal with BARC opens up a new revenue stream

with long-term order potential

LEWL’s Strategic Capacity Boost for Future Revenue Growth

LEWL’s strategic capacity enhancement through a INR 40 crore investment in FY23

signifies a forward-thinking approach, boosting its capability to meet growing demand

and drive revenue growth

EBITDA and PAT

LEWL’s EBITDA and PAT are expected to grow at a CAGR of 59%/66% to INR 209/168 cr

respectively. EBITDA and PAT margins are expected to enhance by 430/500 bps to

21%/16.8% respectively.

Return ratios

Subsequently ROE and ROCE are expected to enhance by 610/750 bps to 24.9%/22.9%

respectively

Note: No recommendation, pl do your own study; Not Invested

KPI Green- Turning Sunshine Into Cashflows (28-12-2023)

Same here. Couldn’t agree more

IDFC First Bank Limited (28-12-2023)

Holding could be going up due to the merger and not due to secondary buying.

IDFC First Bank Limited (28-12-2023)

The attached news is very interesting. Seems like more buying to come in next few days.

Kotak Mahindra Bank – Low Cost Liability Banking Franchise (28-12-2023)

may be true… but mean reversion is also a possibility…as rates have reached peak and possible to go down in the coming quarters.