Operating income for FY 2023 = ₹3411 Cr

Operating expenses for FY 2023 = ₹2242 Cr

Cost to income ratio = 65.7%

Please verify yourself, my calculation may have mistake.

Posts tagged Value Pickr

Akash Portfolio (27-12-2023)

Investing Basics – Feel free to ask the most basic questions (27-12-2023)

IMO, it’s a gut feel one develops after scanning leadership for checks such as:

- Promoter: Owner Operator [Pay, Ownership, and RPT | Pledging; Selling…?]

- Incentives

- Prior Experience and CareerFootprints

- Strategic Plan Vs Day today Improvements

- Approach to Issuing Guidance

- Mgmt. Style: Centralized/Localized

- Senior Mgmt timeline of last 10 Yrs.

- Type of Board Members

- Capital Allocation: FCF – Reinvest | Cash | Dividend | Buyback | Acquisition

- Moment of Integrity [Behavior under stressful situations]

- Clear and Consistent communication with shareholders [MD and CEO Letter/Talk – Talks about Important Issues, Easy to Listen to, You Learn from the Mgr. | Beware: Seeded with PR, Copy of MD&A, Jargons, Double speak]: Answers or Responds to the questions.

- Independent Thinking ++ Avoids Me Too Attitude

- Self-Promoting [Frequent Media Appearances, Promotes share price]

- Accounting: Aggressive or Conservative

Even after spending time on all these, one could never be 24Carat sure.

Senco Gold: Upcoming gold story! (27-12-2023)

A little bit about the company:

-

Senco gold is largest organized retail jewellery player in the country with a market presence in more than 13 states. They have company owned company operated (coco) stores as well as franchise store model.

-

The company has a dominance in the eastern part of India with a volume growth rate of 32% in h1fy24 YoY.

-

Senco has 145 stores which includes 83 coco stores and 62 franchise stores. 57%-43%) .90% of the showrooms are leased.

-

The number grew from 136 stores in fy23. so, a 6.6% growth in 2 quarters as far as store opening is concerned.

-

Out of the 62 franchise stores 49 showrooms are in tier 2 cities.

-

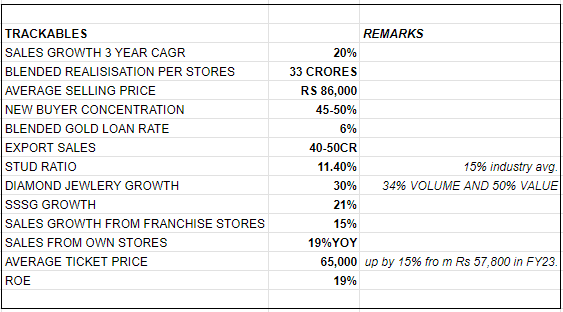

The company has allocated different showrooms for different audience.D’signia being the most premium with an average ticket price of Rs**.76,900** and house of Senco and Everlite being the most economical @ Rs. 37,000.

WORKING CAPITAL REQUIREMENTS FOR A STORE:

A store spends on two things while opening a store:

- Inventory : Inventory requires approximately 10-12 cr. capex requires 1-2cr.

- Capex: The company does no capex for any franchises. the franchises themselves have to pay for their inventory and their capex.

STORE’S ECONOMICS

-

The current stores are open in 55:45 ratio between coco and franchise stores. Franchise growth rate is 15% and the contribution stands at 35%.

-

The inventory turnover for a franchise store from 1st year is 2 and reaches 3 by the third year. blended franchise turnover is 2.

-

The company owned stores have a gross margin profile of 18% and in case of franchise stores, the gross margins are anywhere between 10-12%.

-

Senco keeps 6-7% of the margins with them while leaving 11-12% for the franchise stores.

-

that implies = 2*10cr of inventory = 20crs worth of inventory in a year with 12% gm = 2.4crs approximately, when accounting for inventory. the store pays and get the inventory. the company doesn’t show these inventory levels in their books

HEDGING:

• The company is 80% hedged and have hedged it using two instruments:

1.) Gold metal loan: accounts for 50-55% of their hedging positions:

gold metal loans are taken from the bank for their requirement of gold for their inventory. They take an unfixed loan where gold prices are directly related to the amount they pay to the bank.

•Positions on mcx: They hedge the rest of the positions with futures and options. this is a common practice in the industry.

• the crux is that they have no effect scenario as far as price escalation or de escalation is concerned.

SWOT ANALYSIS

I have done a swot analysis keeping in account the various strengths, weaknesses, opportunities and threats I find in the company. This analysis covers most of the aspects of the space that the company is right now in and might be in the coming future.

STRENGTHS:

-

Their reputation, industry expertise and knowledge: second largest retail jeweler in the country, presence in more than 13 states. have company owned stores as well as franchise stores.

-

Dominance in the eastern region: *East has 110 stores, approximately 76% of total stores. with 49 own stores and 61 franchise stores.

-

gold price escalation and de-escalation does not have any effects: because of proper hedging mechanisms in place.

-

Inventory stock turnover: Churning of stock where required gives them an edge in stock turnover ratio : **higher stock turnover gives them better roe

-

Tech savvy: launched a metaverse which allows customers to view and try on all the designs virtually. giving them a sense of the design and look. have a website names ever lite, targeting gen z by offering modern diamond designs.**

WEAKNESSES

- too much dependence on just gold. 90% of the sales are in gold products.*

- stud ratio lower than of industry average. 11.8%vs 15%.*

- slight seasonality in sales. h1 is lighter in sales as compared to h2*. The margins also get affected due to this.

- Sectors like exports have negligible margins for them. But with decent growth potential.*

OPPORTUNITIES

-

Male jewelry growing at a 15% rate (gold chains and rings)

-

Replacement market growing because of government policies eg. HUID code : purchase from old jewelry increased to 24% of sales from 19%

-

Sectoral shift from unorganized sector to organized sector: currently stands at 33-38% for organized and 62%-67% for unorganized. expected to reach 42%-47% for organized and 53-58% unorganized by fy26.

-

their average ticket price is rs.65,000, with a revenue of 4,000 cr. number of transactions has been around 5l, this suggests: the light stud jewellery which is sold on their online portals and stores increases the diamond sales. as they grow more in this segment. margins are bound to get better.

-

daily wear jewellery trend. 35-40% people are buying jewellery for them for daily wear purposes.

as their share in diamond jewellery increases which is very insignificant right now profitability increases on an ebitda level and looking at their target audience, their market share is expected to go up. As far as diamond sales are concerned they have doubled their sales in diamond in the last 4 years.*

THREATS

-

Heists: Two stores in the same region were looted, insured but insure repayment takes time.

-

Regulatory developments: Any potential regulatory developments can hinder with the short term , medium term growth eg, Deomotization.

-

Lab made jewelry: has a major effect on diamonds, especially the large studded ones. effect has not yet been seen on the smaller sizes yet.

-

Potential strikes from karigars: Company is heavily dependent on karigars from east.

GUIDANCE AND OBJECTIVES:

-

Better reach in north. to improve on stud ratio: some stores in the north particularly delhi ncr has a stud ratio of 20%*

-

Guidance is to add 20-25 stores every year till FY26: blended realization per store is around 33crs.

-

open coco stores in metro cities for higher diamond sales and better realization.

-

plan of action is to use hub and spoke model and penetrated deeper into tier 2 and tier 3 cities.*Targeting north and east as primarily.

-

maximise inventory turns because better inventory turns, higher roe’s.

-

for fy24 the guidance for the topline growth is at 20%.

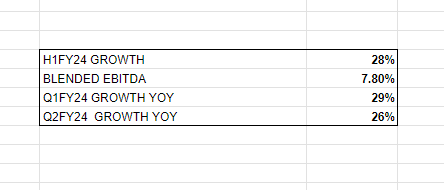

Some of the trackables which are important for the industry are as follows:

*This is not a buy or a sell recommendation!

I have created this thread on Senco gold to have better understanding of the company through the wise inventors and learners we have on this forum. Its imperative to keep having discussions on this company through this thread to have a better understanding of how the company performs.

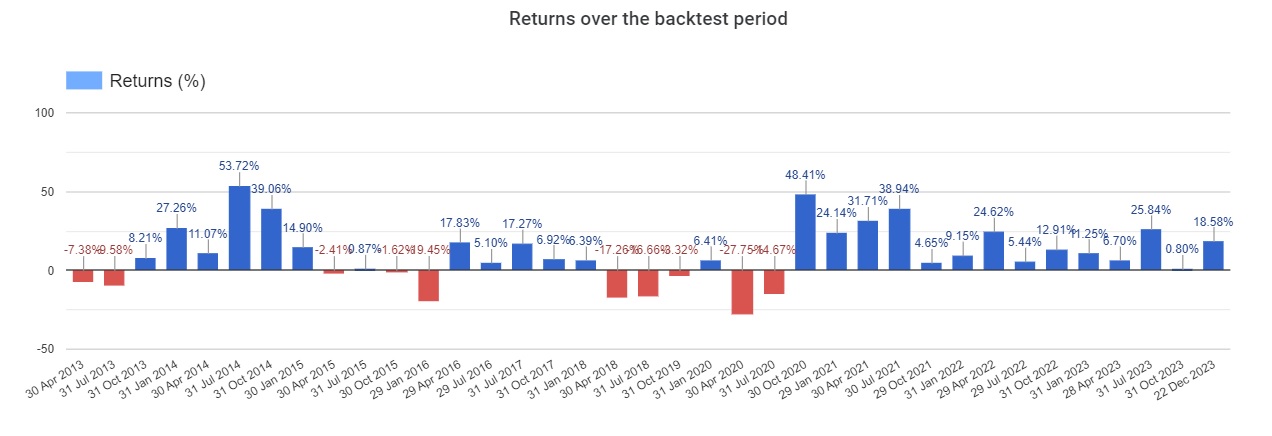

Simple strategy with back-test results (27-12-2023)

Hi Abhi,

Have further tweaked the revenue growth and annual roce as both of these parameters become important for my comfort.

6 losers out of total 23 stocks and 17 winners.

My query :

“Market Capitalization in Cr > 500 and

Long Term Debt To Equity Annual < 0.3 and

Promoter holding latest % > 40 and

ROCE Annual 5Yr Avg % > 25 and

( EnterpriseValue Annual Cr / Operating Profit Annual in Cr ) < 5 and

( EnterpriseValue Annual Cr / Operating Profit Annual in Cr ) > 0 and

ROCE Annual % > 10 and

Revenue Growth Annual YoY % > 0”

Current list :

SJS Enterprises Ltd (27-12-2023)

Just to add to your points, while they did replace the CFO, a new professional CEO has never come (Sanjay Thapar wanted to remain as a Director and take up a more strategic role, with KA Joseph focusing only on new product development). Wonder what made them reconsider their decision of a new CEO. This also says about the drive of the current CEO who doesn’t want to run day to day operations and me more hands on. Agree with you that the mgmt. (Mr Sanjay in particular) sound overly optimistic despite generally missing expectations for multiple quarters since listing.

Roto Pumps – Fluid Engineering Company (27-12-2023)

@shanki_Bansal: Thanks for sharing your note. Few questions since you follow it for quite some time:

- Any idea why they are unable to scale up [Sales and Op. Profits] their subsidiaries meaningfully even though some were started 9+ Yrs. back?

- What’s the revenue potential from downhole pumps, mud motors, and Solar Pumps?

- What’s their USP in the exports market since the majority of revenue comes from exports? In FY15 AR, it was noted “Two global major players have set up their base in India. Their presence is felt significantly as some definite amount of business has been lost in the year under review”. I infer that the company had difficulty competing with global major players in home base. How did they overcome the trend in exports?

- How are their products or competencies different from peers such as KSB, WPIL etc?

Disc: Under due diligence.

Krsnaa Diagnostics – what is the diagnosis? (27-12-2023)

and Cash tax Paid/Reported PBT –

Variations a plenty ranging from 34% to 6% between 2019 and 2023 – wonder what lends to such volatility

Disc – noticing plenty of amber flags, hope fellow community members can help wrap our heads around this

Krsnaa Diagnostics – what is the diagnosis? (27-12-2023)

and Cash tax Paid/Reported PBT –

Variations a plenty ranging from 34% to 6% between 2019 and 2023 – wonder what lends to such volatility

Disc – noticing plenty of amber flags, hope fellow community members can help wrap our heads around this

Krsnaa Diagnostics – what is the diagnosis? (27-12-2023)

I have recently started studying this co and there a re a few things I could not wrap my head around –

- How much did the Promoter dilute to PE in 2015 that his stake came down to 31% Pre IPO?? Seems a little off to me given that Vijaya for instance, diluted to Kedaara and yet promoters held 54% post listing

- Co began in 2011, raised PE money in 2015 – which means within 4 years of beginning operations, they were technically qualified to bid for large B2G Contracts (these often come with a minimal technical qualification rule)

- co was doing 40-50 crore of rev till 2017, what exactly happened between 2017 and 2019 that revenues tripled, co filed IPO Papers all in the same period ? (this should be the quickest that a startup has began operations and filed for IPO – 8 years)

- ZERO management bandwidth when it comes to this space. Apart from the COO who is ex Metropolis, I dont see any top management guy who has any experience in the healthcare space. Infact, Yash Mutha has spent 15+ years working at CS backend + top 4 accounting firms. Wonder what experience does that lend to in managing such a complex, government oriented biz

Krsnaa Diagnostics – what is the diagnosis? (27-12-2023)

I have recently started studying this co and there a re a few things I could not wrap my head around –

- How much did the Promoter dilute to PE in 2015 that his stake came down to 31% Pre IPO?? Seems a little off to me given that Vijaya for instance, diluted to Kedaara and yet promoters held 54% post listing

- Co began in 2011, raised PE money in 2015 – which means within 4 years of beginning operations, they were technically qualified to bid for large B2G Contracts (these often come with a minimal technical qualification rule)

- co was doing 40-50 crore of rev till 2017, what exactly happened between 2017 and 2019 that revenues tripled, co filed IPO Papers all in the same period ? (this should be the quickest that a startup has began operations and filed for IPO – 8 years)

- ZERO management bandwidth when it comes to this space. Apart from the COO who is ex Metropolis, I dont see any top management guy who has any experience in the healthcare space. Infact, Yash Mutha has spent 15+ years working at CS backend + top 4 accounting firms. Wonder what experience does that lend to in managing such a complex, government oriented biz