You are right in the supposition that this question does not belong to this thread. This is not a thread to give opinion on other websites or advisories. In the future let’s avoid these kind of queries on this thread.

Posts tagged Value Pickr

Fine Organics – Niche Player in Specialty Chemical (24-12-2023)

Fine Organics – A Business Analysis, 24th Dec 2024

Background

Fine Organics, founded in 1970, is in the chemical specialty additives business. They produce additives from oleochemicals, i.e., additives derived from vegetable oils, instead of petrochemicals. These are biodegradable. One may say they are renewable but in my opinion that depends on one’s perspective – crops need fertilizers, fertilizers in turn are produced using vast quantities of natural gas and fertilizer use can lead to Nitrogen and Phosphorous pollution. So, I have a somewhat skeptical view on these oleochemicals being called ‘renewable’ and ‘green’, although marketeers can get away with it. Certainly thought, oleochemical have advantages over petrochemicals. That is unarguable.

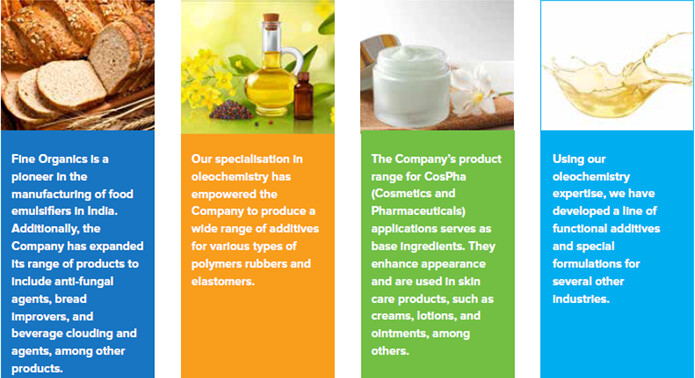

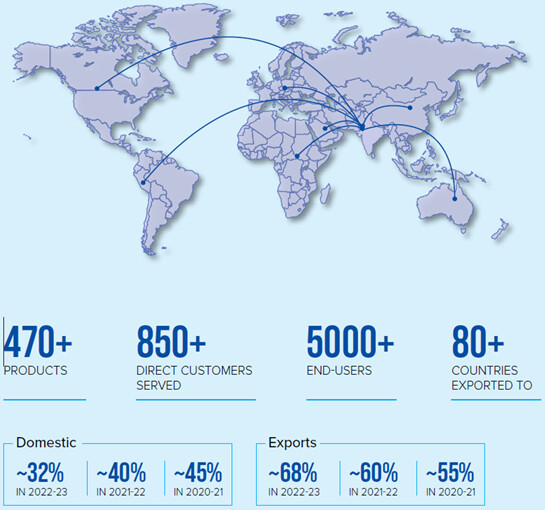

Fine Organic’s target industries include foods, plastics, packaging, coatings, polymers, cosmetics, rubbers and feed nutrition. See Figure 1. They have a diversified product portfolio of products sold to a diverse customer mix and with exports to 80+ countries. In fact, the domestic:export mix is about 40:60. See Figure 2 for details.

Figure 1: Target industries of Fine Organics.

Figure 2: Product and customer mix of Fine Organics.

Business drivers

Additives typically are only a small percentage by weight or volume of a product but they can change the characteristics of the end product tremendously. For instance, anti-fungal agents in foods, polymers that are flame retardant, hydrophobic, non-fogging etc. So, this a value-add industry, the opposite of commodities.

An established player like Fine Organics, the biggest oleochemical company in India and among the top six in the world, has a decent moat, as can be deciphered from this statement in the 2023 annual report: The regulatory approvals obtained from different industry institutions are typically only valid for a specific time. In addition, regulatory compliances are frequently revised depending on the location, industry, end-use, and other factors. It might then take another three to five years for an end client to accept the additives once the immediate customer has given their approval. See Figure 3 based on investor presentation Nov 2021.

Figure 3: Entry barriers into the oleochemical additives business.

So, for a new player, its hard to break into the market. Established players though may have enough stable products to foray into new areas or compete with other established players. The business is simple enough, purchase edible oils, convert them into oleochemicals and sell them to customers like Coca-Cola, Britannia, Asian Paints, Parle, Pidilite, Berger Paints etc. It’s the regulatory process that prevents new players from getting into this business.

Concerning risks, India is a net importer of vegetable oils so there is currency risk, but since half the revenues are from exports, this is not an issue. Oil prices can also vary wildly so Fine Organics has contracts ranging from 3-6 months with suppliers (AR 2023). Any duration mismatch for contracts with customers can lead to wild margin changes, both on the upside and the downside. Based on an analyst report, Fine Organics from 2021, had entered into shorter term contracts with customers. But this may keep changing. My message is that keep an eye on the margins – volatility there may be due to contract duration mismatch with suppliers and customers. The annual report seems to have no info on this.

Regarding growth, as per the AR 2023, the global specialty chemicals market was valued at US$ 612.2 billion in 2022 and is expected to grow at a CAGR of 5.1% during 2023-30. The specialty chemicals industry in India has expanded exponentially in recent years and is anticipated to reach US$ 64 billion (10% of global) by 2025 at a CAGR of 12.4%. A bit more granularity below:

The global food additives market size is expected to register a CAGR of 4.6% from 2023 to 2030.

The global plastic additives market was valued at US$ 51.01 billion in 2022 and is anticipated to grow from US$ 52.45 billion in 2O23 to US$ 83.3 billion in 2030, registering a CAGR of 5.3% between 2022 to 2030.

- The global cosmetic ingredients market is estimated to register growth at a CAGR of 5.3% during 2022-28.

- The global market for coating additives is expected to reach US$ 17 billion by the end of 2032 registering a CAGR of 5.9% from 2022 to 2032.

Since exports are 50% of revenue, even if you assume that the Indian growth is larger than the global growth, the above numbers give a ballpark indication of the company’s potential growth rate.

An unfortunate aspect is that the company offers no granularity on the revenue mix from their different product lines. So, it could very well be that food additives are 80% of the revenue and CosPha only 3%. I don’t know! The revenue mix could shed light on both strengths and weaknesses of the business.

Considering that there are around 6 oleochemical companies in the world, this business can’t really be considered oligopolistic. Further, I don’t think this is a business that can be compared with that of Asian Paints or the like. Asian Paint’s success has been as much about marketing and supply chain efficacy (refreshing stock in the typical tiny Indian stores with limited storefront area multiple times daily) as about the product. Fine Organics is not an end user facing product – they are dealing with other large companies who would go for the cheapest supplier for a given quality, even if it takes a while to onboard a new supplier. Anyhow, who is to say that a business like Coca-Cola does not have two suppliers on board anyhow, as part of their own risk mitigation strategy. And then play of one against the other to not allow someone like Fine Organics to have too much pricing power.

Analysis of Financial Statements

Figure 4: Gross and operating margin of Fine Organics.

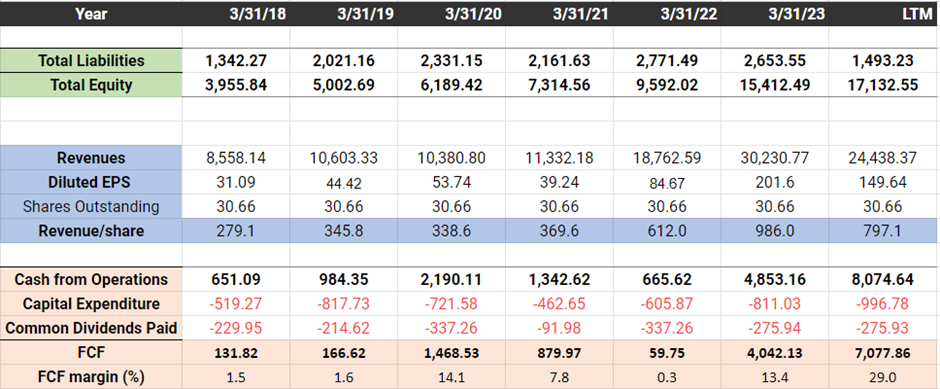

As shown in Figure 4, the operating margin of Fine Organics has been exceptionally high in 2023. This is likely due to contract mismatches between suppliers and customers during this period and is likely unsustainable. One can already see that key metrics (Revenue, EPS, Revenue/share, cash from operations) in the LTM are going down in Table 1. Overall, EV is lower than market cap, so the company has cash on the balance sheet after netting out debt. FCF margins are super volatile, but its clear that the company is growing (equity, EPS, Revenue/share). INR 500-600 million seems to the annual capex – 60% of this seems to maintenance capex (calculated from depreciation and amortization) while the rest is reinvested back in the business for growth at high ROCE. The current ROCE of 2023 is not reliable because current margins are too high (Figure 4) but under normative conditions the business still has high ROCE (>20-25%).

Table 1: Key metrics from financial statements in millions INR over the past five years.

Table 2: A DCF valuation for normal, best case and worst-case scenarios using FCF as input.

For valuation, I prefer to use EPS and taka a more normative EPS of INR 100. 10 years from now, I imagine there is more competition and that the ROCE has reduced and therefore also the terminal value. Under high growth rate assumptions (much higher than the sector that I mentioned above) which are entirely plausible the business is fairly valued for a 10% return. But under normal case assumptions, the share price can half from here – plausible if there is margin contraction for a couple of quarters along with a reduction in PE.

Investment thesis

This is a good business with a high ROCE, secular tailwinds and a long runway. Currently thoguh its priced for perfection.

Company news

Nothing special.

Catalyst

It’s a good business, the question is how much you are willing to pay for it. For me, its richly valued so its one of those that you put on the watchlist and wait. It might be a good one for a classic Phil Town, event-based investment. Wait for a couple of bad quarters, high oil prices, margin contraction, temporary issues with the company and the like. And if you get it cheap, hold on for dear life. For me I need a 50% decrease on the current market cap. A few years from now, if the company grows, I might be willing to pay the current market cap. More likely is that I will never get a chance to get in. Also ok for me, I can live with that. I can’t live with no margin of safety.

Investing Basics – Feel free to ask the most basic questions (24-12-2023)

How to check corporate governance and allocation of a company is good or not?

Balaji Amines Opportunity (24-12-2023)

Exactly my point. If we combine the capacity of alkyl and balaji and then if we consider this dumping by chinese then there is hardly and scope for a long term story. And Kirit Patel has said that these kind of situation do come for 2-3 years for every decade. Its very difficlut to find a multibagger or a consistent compounder in such kind of sector with such nature of business…Or am I reading this all wrong? I would like to be in such companies where I can stay invested for a very long time without worrying about market size and growth of my investee companies…It may be inappropriate but with this background requirements, how would you judge Deepak Nitrite or SRF and P.I. Industries?

Balaji Amines Opportunity (24-12-2023)

Exactly my point. If we combine the capacity of alkyl and balaji and then if we consider this dumping by chinese then there is hardly and scope for a long term story. And Kirit Patel has said that these kind of situation do come for 2-3 years for every decade. Its very difficlut to find a multibagger or a consistent compounder in such kind of sector with such nature of business…Or am I reading this all wrong? I would like to be in such companies where I can stay invested for a very long time without worrying about market size and growth of my investee companies…It may be inappropriate but with this background requirements, how would you judge Deepak Nitrite or SRF and P.I. Industries?

Trent — A value unlocking story from the house of TATA (24-12-2023)

But what about the obscene PE ratio? Doesnt it make you uncomfortable?

Trent — A value unlocking story from the house of TATA (24-12-2023)

But what about the obscene PE ratio? Doesnt it make you uncomfortable?

Trent — A value unlocking story from the house of TATA (24-12-2023)

Visited the zudio store as was always intriuged by the growth and price point . Have been a frequent to westside .

I should say that Zudio will give tough competition to road side shops / vendors .

The fabric quality and experience of try and buy with a price point starting from 199 makes it connect to the indian consumer

I would put it that way that westside is for middle class and zudio stands apart for lower middle & middle consumers .

Bullish about the growth prospects

Been a very long term holding

Trent — A value unlocking story from the house of TATA (24-12-2023)

Visited the zudio store as was always intriuged by the growth and price point . Have been a frequent to westside .

I should say that Zudio will give tough competition to road side shops / vendors .

The fabric quality and experience of try and buy with a price point starting from 199 makes it connect to the indian consumer

I would put it that way that westside is for middle class and zudio stands apart for lower middle & middle consumers .

Bullish about the growth prospects

Been a very long term holding