AIF circular by RBI, what is the impact on Edelweiss?

Posts tagged Value Pickr

Titan Company Ltd : a three decade old company (21-12-2023)

I made the assumption of 15% growth on the basis of this post:

Plus the base has become really big, can’t expect it to grow the way it was growing 5 years back.

The last 5 year median PE is distorted and skewed towards a higher number because of muted earnings during COVID.

While they currently contribute a modest percentage to the overall revenue, it’s worth acknowledging that some of these ventures possess the potential for significant scalability. It would be prudent to keep a vigilant eye on their trajectory and evolution.

SmallCap Hunter : Trying to find the dark horses with triggers (21-12-2023)

I tried but theres nothing, no information whatsoever on how the business is doing what is their outlook etc.

If anyone can pls share any info they have.

DCX Systems Ltd (21-12-2023)

what you are pointing to could be anybody’s guess (including mgt).

But the interesting part is management provided anecdotal markers like “Isreal counterparts are receiving calls and making timely payments”.

I think, this war could be a watershed moment for DCX where they get new opportunities to partner, but all that largely depends on India’s geopolitical position and how that evolves.

Disclosure: Invested, no action in last 3 months.

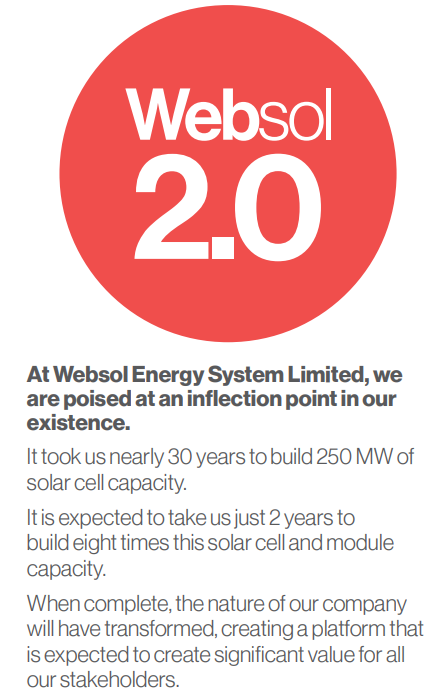

Websol energy system ltd (21-12-2023)

Yes. The history was not good so as the whole Solar industry in India. A small company like Websol arrived to market with just 1 MW capacity way ahead of its time (Globalization year 1990) and suffered due to unfavorable policies. The traction in this sector was visible late 2010 only. So, there is nothing wrong in calling a spade a spade. Much respect to Vijay malik Sir.

However, the market is always a forward looking one. So, the shareholders must be interested in the future of the business and its potential to create a meaningful value. let’s hope the Management walk the talk. Just my opinion. Hope the below image will summarize this discussion.

DCX Systems Ltd (21-12-2023)

DCX is primarily an import offset partner. They are doing value added work on imported parts which is supplied to the end customer.

Hence, fixed assets turnover etc are not reliable. EBITDA margins in EMS is usually 4-5% irrespective of customer or product categories. the same holds true for DCX as well.

The right set of peers for DCX are EMS companies like Dixon, Amber, Kaynes etc. But because, the customer set each of these companies cater to, are different, the growth potential and hence valuations are also very different.

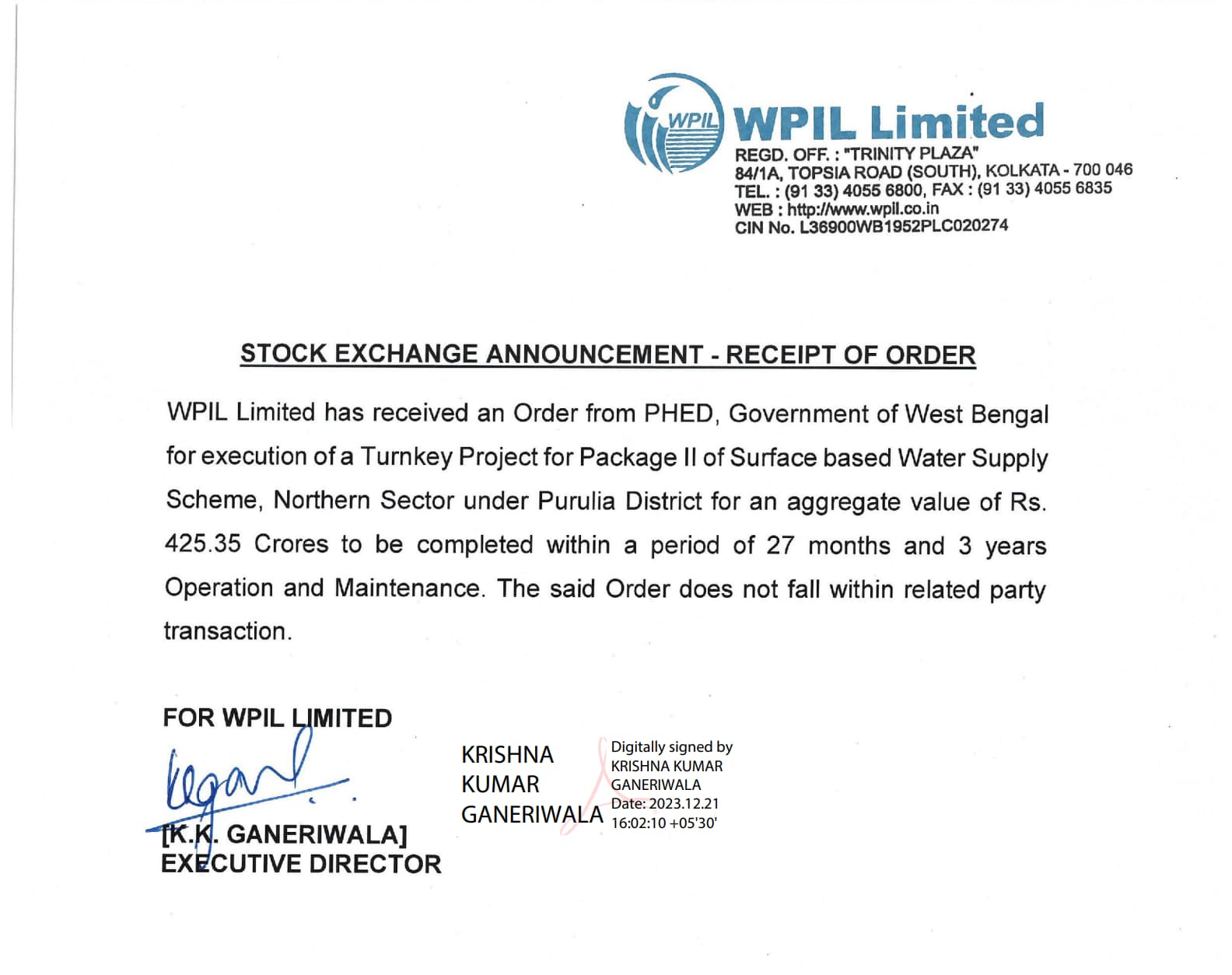

WPIL Ltd – Global Water Pumps (21-12-2023)

Another day in the upper circuit?

Skipper Ltd., (Power and Water) a moat in making? (21-12-2023)

Some takeaways that I am permitted to share.

- Order execution in full flow

- Logistics booking being initiated for deliveries

- Weight counted in over lac-MT+++++……

- Bidding ongoing for new tenders Dom & Exp

- New orders in pipeline may be disclosed soon

- H2 may be better than guided/expected

For me, it’s my highest allocation already.

Invested, bullish, not biased.

Please DYOR before investing. Do consult financial experts.

Ps: if my thesis is proven wrong, I have no qualms in accepting, learning, and exiting the company. I invest on management depth, market leadership, sector growth & demand, etc. My holding periods a long, and I’m alright with drawdowns, as long as corporate & business hygiene is intact. NOT an expert, just a dreamer

Ami Organics – Pharma Intermediates & Specialty Chemicals (21-12-2023)

Ami Organics Signs MoU with a Global Manufacturer Of Electrolytes