My intention was to emphasize that management considers other income as a component of operational efficiency. Consequently, operating income in FY23 is not lower than FY22, please disregard this information if it does not align with your focus.

Posts tagged Value Pickr

Avanti Feeds (18-12-2023)

This is what I was able to come up with after doing some reading here and elsewhere (AR, earnings call, research articles, etc). A huge thanks to those who really dug and put up the information here in the previous posts. I have not read extensively but had a glance at Avanti Feeds and Sharat Industries and so the analysis is in the context of the shrimp sector mainly. Those of you who have been following the stock for a while, kindly correct/comment. A nice video on differences in productivity between the shrimp producing countries: https://www.youtube.com/watch?v=UnUci4BF97k&t=1213s)

What’s against the industry:

- Competitively priced shrimp from Ecuador

- The perception of Ecuadorian shrimp being better than Indian shrimp

- If the US (AD and CVD) investigations concludes that government subsidies by both Ecuador and India are either “equal” or Ecuadorian subsidy is “less than Indian” subsidy or even after introducing the additional import tariff and dumping duty, Ecuadorian shrimp is still more competitively priced relative to the Indian shrimp.

- Apart from Ecuadorian shrimp productivity (and output) already being superior to the Indian shrimp productivity (and output), if Ecuador ventures into Value added products and is able to scale, the Indian shrimp will further lose its competitiveness

- Volatility in price of the 3 raw materials in addition to government intervention (in the form of minimum support price for Wheat and Soyabeans and a non-conducive policy for fish meal production/import)

- Raw material prices remain relatively high throughout and do not come down as anticipated (Feed business is left with mediocre margins)

- Inability to raise prices as farmers are price sensitive (shifting to fish, etc) and government intervention to protect farmers

- A disease or virus affecting shrimp production in India (and asia/globally)

- India is unable to adopt the technological advances for increased productivity (automatic feeders, mechanical harvesting, availability of electricity, lack of vertical integration and large-scale farming), hence loosing against Ecuador.

- Although management has skin in the game, but slightly exorbitant salaries may indicate something – Are good times behind us? / Is Growth coming to an end?

- Management becomes dumber: Either under pressure to meet market expectations or in order to justify the increased pay, they might expand into new areas (destroying capital or taking on debt). This might be unlikely but you never know with certainty with new blood coming in.

- Their ability (and probability) to return to their original (or normalized) margins depends entirely on the upturn of the cyclical-nature (revival) of the shrimp industry in India. (THE UNKNOWABLE)

- How bad could it get? (THE DEADLY UNKNOWABLE) i.e. The probability of the Indian shrimp sector being wiped out as a result of the fast and aggressive ascent of Ecuadorian shrimp sector, which has advantages of higher productivity, large vertically integrated players and proximity to US and Europe.

What’s in the favour of the industry:

- The company has no debt and plenty of cash (most likely can withstand a prolonged downturn)

- Capitalism at Play: If you consider the US to be the cradle of capitalism, and if the AD &CVD investigation levels the playing field for India and Ecuador, then there is a very good chance that things might get back on track with an upturn in the cycle. (The investigation against Ecuador and Indonesia is for selling in the US at less than fair value and govt. subsidies whereas the investigation against India and Vietnam is for govt. subsidies). If allegations prove to be true and the outcome/result of the investigation plays out positively, with the former two countries put at a greater disadvantage than the later, then this might result in the Indian shrimp becoming competitive and growth might continue with the upward turn in the cycle.

- (For Avanti) Management has a proven track record of not making dumb decisions, being conservative and has skin in the game (I am fine with them hoarding cash). They might be slow, but are cautious – slow for not recognizing Ecuador as a threat and cautious for keeping cash for opportunities and not giving it out either as dividend or buybacks along with a strong reluctance to using bank debt (aversion to paying interest – I personally like that).

- (For Avanti) The new areas of pet food and care are accretive to volume, growth and revenues – difficult to put a probability on how this might play out in the Indian market.

- Adoption of shrimp as a part of staple food in India – a distant possibility, unlikely to happen in the short term

- (For Avanti) – Growth from shrimp feed being consumed by Bangladesh and Sri Lanka – again very unlikely. (Pros – low cost of labor; Cons- lower productivity)

- High returns on tangible capital (if the cycle turns normal)

- (For Avanti) All the negative and uncertain aspects discussed above are priced in the stock (This is true from a valuation perspective only if you are investing on the basis of reversion to mean and an upturn in the cyclicality of the business/industry). However, it certainly is not cheap considering the above negatives – On a TTM basis AVANTI commands a PE of 16, an EV/EBIT of about 10 and an acquirer’s multiple of 14; and the fact that I cannot predict the normalised earnings with a reasonable degree of confidence. One might say it’s fairly valued with no debt and management with a decent chunk of skin in the game. (Multiples were calculated on a standalone basis for the core business and hence excludes other income form investments).

- If the business cycle is up by the time the new processing facility comes online in March 2024, this could help them scale revenues, earnings and growth (both for Sharat and Avanti)

- There was a recent month on month increase in US imports of shrimps from India – could indicate an uptick in the cycle (however, difficult to say/judge with Ecuador being a worthy opponent)

- A new initiative of fish feed – this might need a while before it can be considered to be on the cards.

- Freight costs have come down – but doesn’t help much overall

- The raw material costs could decrease gradually once the new crop comes in, with prices of soyabean and wheat normalizing. However, this is speculation.

- I could be wrong/inaccurate here: “The import of brood stock fell by as much as 40% from December to march 2023.” Might indicate lower overall output → decreased supply resulting in higher prices → more farmers in action next season → more consumption of feed → bumper supply before the cycle turns down again. The key would be to get out before the cycle changes direction, but the pot might be sweetened if the US investigation permanently shifts the scale on our side (this is too much to ask btw).

@harsh.beria93 @lakshay_agarwal @spatel @shyamdsundar – Any insights are highly appreciated. Thanks

Finkaro Unfloding The Unheard Companies with Lot’s of Potential (18-12-2023)

Feed and Shrimp Processing Industries: India

“What Went Wrong in the Feed Processing and Shrimp Industries”

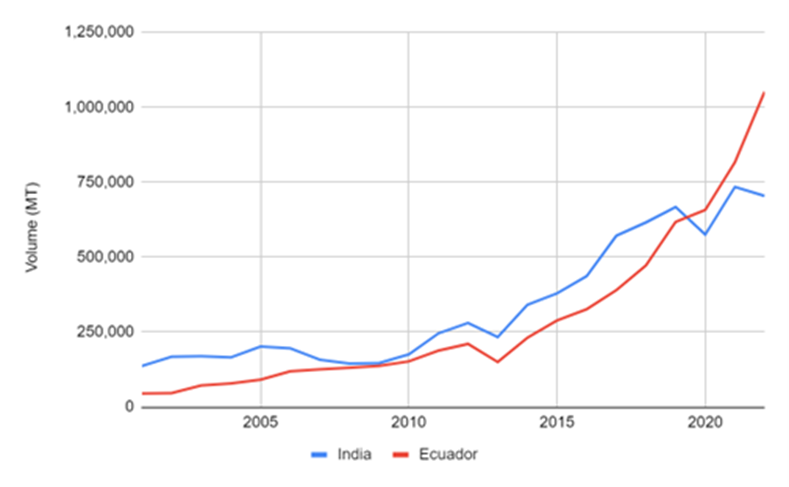

The world’s two major shrimp exporters—Ecuador and India

Increase in the capacity of Ecuador leads to oversupply and spiralling prices impacted Indian Shrimp Industry Badly Below chart shows how last 2-3 Years export of India Compared to Ecuador

How They able to Do This

Ecuador’s farmers have been increasing their output by using post-larvae that are tolerant to disease and grow increasingly fast; by using nursery ponds to shorten production cycles; by adding aeration systems and auto feeders to their grow-out ponds, which enable higher stocking densities

Ecuador supply at $7.42/kg where India Supply at $9.1/kg which leads to decrease the market share of India from 43% to 36% in 2-3 Years now again back to 36% in US

Ecuador has a lower cost of production of processed shrimp as processors there are large vertically integrated companies. Additionally, they have become the biggest producer of shrimp in past 2 years (from production of 600 mn to 1.5bn now).

Ecuador focuses on commodity products like headless shell on or head on, shell on shrimp

Raw Material Cost Increased for fishmeal, soyabean, wheat impacted the overall Indian shrimp Industries

Market expansion

Nearly 75% of China was made up of Ecuador shrimp market but covid restriction led to Aggressively focus product in US Market proximity to US coast reduced the Shipment transit time, faciliting Ecuador to dump its product in US Market leads to stiff competition to India where Shipment from India to US it takes Nearly 40 Days leads Further increase in fright and landing cost

What’s Happening Now

· Most of the Indian company under CAPEX and may commissioning of new plant will yield good topline growth and better ROCE

· US shrimp import market has seen improvement in past 3 months after 13 consecutive months of YOY decrease. However, realizations are lower by 10-15%

· In Indonesia and Ecuador, there might even be Antidumping Duty by US Countervailing Duty

· Company To Watch out: Avanti Feeds, Sharat Industries, Apex Frozen, Coastal Corporation

· Avanti a Market Leader Needs to closely monitor, company at bottom price, cyclical benefit may play out ,the PE at Lowest as compared to Mean PE of 5 Years

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (18-12-2023)

any idea who is building fuel cells for it, KPIT or some others ?

Oriental Carbon and Chemicals Ltd (18-12-2023)

https://nclt.gov.in/case-details?bench=YWhtZWRhYmFk&filing_no=MjQwMTEwNTAxOTg5MjAyMg==

NCLT disposed the case in May ’23. What more needs to happen for the demerger to go through? @R_J

Disc.: invested

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (18-12-2023)

Hydrogen Fuel cell electric trains in India

To start with Indian Railways (IR) has envisaged to run 35 Hydrogen trains under “Hydrogen for Heritage” at an estimated cost of ₹ 80 crores per train and ground infrastructure of ₹ 70 crores per route on various heritage/hill routes,” The timetable calls for the first trains to run between Jind and Sonipat beginning in 2024.

The Heritage routes are narrow-guage railways including Matheran Hill Railway, Kangra Valley, Bilmora Waghai, Marwar-Devgarh Madriya, Nilgiri Mountain Railway, Kalka Shimla Railway, and Darjeeling Himalayan Railway.

Gujarat State Petronet Limited (18-12-2023)

Good Analysis, Mirae Asset Mutual Fund has been buying for last 2-3 years and have now

amassed 9% of the total outstanding shares. If the SHP is analysed less than 10% of the float is available at any point of time. Any 1-2% of serious delivery buying would take it higher.

Disc-Invested in Jan2021,first at 220 levels and later at 260, hardly any meaningfull return over last 3 years but willing to wait and add over period of time. Forms- 5% of my portfolio.

mirae asset-gspl holding.pdf (554.2 KB)

Investing Basics – Feel free to ask the most basic questions (18-12-2023)

Hi!,

I have some questions and it’s great if some help me out.

- Is DCF really matter if the investing horizon is below 3 years?, give me insights for short term investing for below 3 years?

- how to get to know sector rotation like railways had their time, then PSU Banks, Now (may be) Green energy, How to be certain which sector is having its cycle.

Steel Strip Infrastructures – Hidden Gem (18-12-2023)

There is no info about this. Steel strip group is doing good. Steel strip infra is micro cap which mcap is 28 cr now and got 45 crore profit in last 2 quarter from associate company. I tried to find more info about Malwa chemtex but unable to get detail info. It is involved in Production, processing and preservation of meat, fish, fruit vegetables, oils and fats. and holding around 2.5% stake (104 cr) in Steel strip group flagship listed company Steel strip wheels ltd.

Gravita India success story (18-12-2023)

In the financial year ’23, mangement said that out of Rs. 93 crore in other income, Rs. 88 crore came from hedging. The remaining Rs. 5 crore was from interest on fixed deposits and such. They explained that the Rs. 88 crore is counted in EBITDA because it’s part of the operational income.