Hi, if a delisting fails, is there any stipulated cool-off period before the company announces the next corporate action?

In the context of TTK healthcare, as the Co still holds the Cash, any insights on what can be the next course of action, distributing the cash in the form of dividends in the coming qtr?

Posts tagged Value Pickr

Delisting Discussions (17-12-2023)

Sugar Cycles: 7-8 years of losses followed by 2-3 years of super gains! (17-12-2023)

The government has decided to allocate 1.7 million tonne (MT) of sugar for ethanol production in the current season against 3.8 MT sweetener used for biofuel production in 2022-23 season from both sugarcane juice and molasses, food secretary Sanjeev Chopra on Friday said.“The government will review the sugar production in the next one to two months to explore the possibility of allocating additional volume of sugar for ethanol manufacturing,” Chopra said at the sidelines of Indian Sugar Mills Association (ISMA) meet.

Green Hydrogen as a Fuel – Indian Companies leading the Green Revolution (17-12-2023)

Good questions raised and we have debated earlier in this thread on this topic.

Further, Someone has already commented at the end of the article

” Meaningless fears! India impounds only 20% of its rainfall. and if we do more rain water harvesting , it will take care of all our requirement”

I tend to agree to this point.

Rain water apart, while how they arrived at conclusion is not given, i suspect Perhaps the authors seem to have ignored other considerations.

(1) Hydrogen consumption is a closed loop system. Hydrogen is produced from water…But when Hydrogen is finally burnt as fuel as in automobile or domestic gas it will produce steam H2O which goes to atmosphere which comes back in rain as water.

.(2) if hydrogen is used as in a fuel cell to produce electricity for example for grid connectivity , the bye product is water which can be recycled back.

(3) Even if hydrogen is used to produce Fertiliser such as Ammonia ,DAP, SSP. which are used to raise food crops which we eat as carbohydrates and carbohydrates produce water when human body metabolise.

(4) we are lucky that our country and our geographical location is such that we have Surrounded by Sea all around East coast, West coast and south india…While rain water harvesting there is a lot of scope and we still have a long way to go , desalination of sea water always remains as an option.

(5) Coming back to Rain where India can take massive efforts in rain water harvesting , nature and Rain God has been very kind to give us 2 monsoons- SW monsoon during June- Sept and NE monsoon in Oct-Dec.

We have Himalaya in North and western ghats and eastern ghats which ensure that we have enough rain in southwest monsoon during June- Sept during which The Himalayan ranges form a barrier to the southwest monsoon winds crossing over to Tibetian low pressure area thereby causing heavy to very heavy rainfall . The western Ghats slso.act as a key barrier, intercepting the rain-laden monsoon winds that sweep in.

The Northeast monsoon ( Oct- Dec)arises due to high-pressure zones that are formed over the Siberian and Tibetan plateaus.

Winds all the way from Siberia blow towards India…However they are blocked by the northern Himalayas which do not allow them to enter the Indo-Gangetic plain. However, they escape from the North-eastern Himalayas and enter Bay of Bengal and from there the moister laden wind blows towards south east sn bring rainfall to the eastern coastal states of South India, including Tamil Nadu, Andhra Pradesh, and parts of Kerala

Therefore , we will never have dearth of water in india- we are lucky. Analysis is short-sighted

Dreamfolks services limited( DFS) (17-12-2023)

Motilal Oswal Focused Fund added Dreamfolks in the month of Nov.23…from 461912 at the end of Oct.23

to 721699 at the end of Nov. 23…

Discl. having tracking position… keenly watching.

Bull therapy 101-thread for technical analysis with the fundamentals (17-12-2023)

Eimco, Weekly – Broke out of the triangle consolidation with resistance around 1600 levels backed by strong policy action from the govt.

This is a play on 3x increase in underground mining that the govt. is planning, while also restricting gear imports

It looks optically expensive, especially post the runup but its something that can do very well over time if this plays out. The risk though is if this restriction on imports is going to apply only to Coal india or also to its mine operators and their subcontractors as well. This is where there could be many a slip. Also its unclear what margins Eimco can make. The breakout gap on the chart can get filled over next few weeks giving some buying oppoertunity around 1600 levels. The terminal value risk here will reduce over time as the piling rigs business is also doing well and could be a play on growth in skyscrapers in the Indian skyline.

Wockhardt, Monthly – Nice chart with base formation and kicking up from it. This is not a sector I understand well but here the play is quite simple. The success of this trade is going to depend on their new molecules WCK5222 and WCK4873 (Nafithromycin). Latter recently completed phase 3 approval. Former might need some capital to get it to completion sometime in the next year and could see contribution from FY26 if successful. From what I understand the opportunity size is huge, running into billions as per management but I think it could be more like $200-300m but with great margins since these will be out-licensed and royalty should be good. No point modeling anything considering this is a zero-to-one bet

Synergy Green, Monthly – First level breakout from 200 levels and another from 250 levels, both showing decent accumulation. If unwilling to play wind through Suzlon, Inox or Sanghvi as an ancillary, SGIL offers a good opportunity with 85% revenues from Wind and with good cash flows. The company currently has 30k MTPA of casting capacity which will be 45k MTPA by June ’23. The promoter interview has good details on the business. They have Vestas, Gamesa, Senvion, Adani as clients. The revenue is driven not just by domestic but to OEM sales that end up abroad and also direct exports. They do casting of windmill parts including turbines.

The machining cost is a significant part of the cost structure and there’s possibility of margin expansion here as the capex coming next year also includes machining capacity if I understand right.

The promoter has pretty strong goals to get to 100k MTPA by FY27 which would mean a topline of 1000-1200 Cr and at a margin of 16-18% could mean significant upside if its pulled off –

it could happen if the govt. doesn’t mess up the wind energy plans and exports continue to remain strong. Initial signs are very promising with the Repowering policy that came up last week. Govt is incentivising developers with land that can generate better PLF to go for better modern technology and also compensating them for scrap and also for the terminal value. This seems to be a very positive move but I am not expert.

Roto Pumps, Weekly – Has a small breakout but has pulled back and given up all gains but still trading above 20 WMA which should offer support. There’s a FII that has been selling continuously which is keeping price down. As a business whatever I have found about this is very promising, be it the margin profile (not many Indian manufacturing businesses can boast of a 25% OPM), new products, new geographies the company is getting into, the consolidation happening in the space with Ingersoll Rand acquiring Roto’s main competetor Seepex and Hydro Prokav. It is heartening to see an Indian business competing worldwide across geographies with German and USA made pumps.

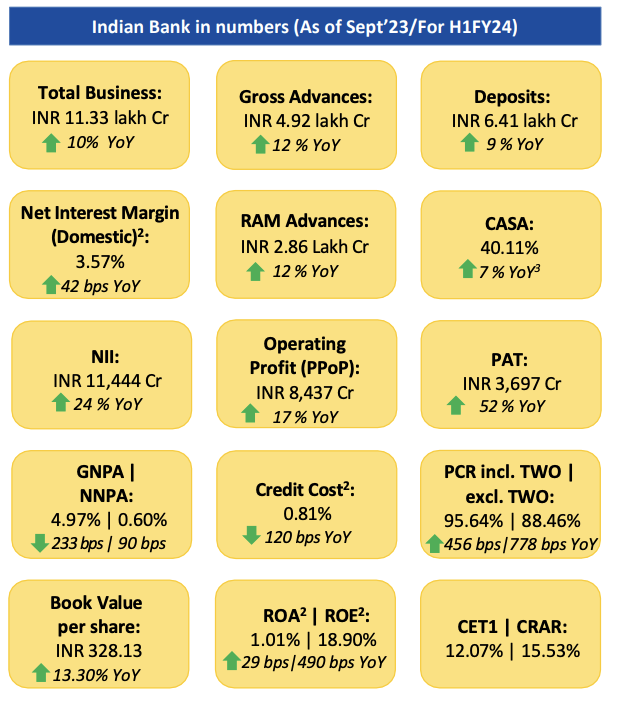

Indian Bank, Monthly – Nice breakout on the weekly after a consolidation.

This is not something I would typically touch but its very tempting. BV is 328, so trading roughly 1.4x book.

I believe BV should grow a fair bit over the next 2-3 quarters since the provisions are about to hit bottom (NNPA at 0.60%) over the next quarter or two and from then on, the growth post-prov profits should be lot higher and I wont be surprised to see 10k Cr PAT here. The same is the case with couple of other PSU banks like Union Bank and PNB as well and could be played as a basket.

Some updates in existing positions

Taal – On the approval for merger of Taal Tech with Taal Ent, the management had promised it could happen in Q3/Q4. There was a hearing on 14th sept and a follow-up on 12/12

I see in the comments as everything being received and don’t see any follow-up being posted. My guess is that this is more or less a done deal and might get to completion in this FY. Hopefully next year’s AR will reflect Taal Tech’s capabilities (the curious can go through employees’ linkedin profiles and get everything they need) and be one befitting a Engineering Services firm, aiding in discovery (as I discovered PML post AR last year)

Ceinsys – Has closed at a weekly high post 8 weeks of going sideways after the breakaway gap as mentioned by @Azlan above. There’s some supply around 370-380 levels that needs to be absorbed before it gets a move on.

Goodluck has had a good close on the weekly and looks to be readying for QIP of 200 Cr. Promoter has made hay here issuing warrants at 300 odd and paying 25% of the 40 Cr (10 Cr upfront) which is already worth 90 Cr. As a trade it still appears cheap and QIP seems to be par for the course in the bull market.

Only risk to this bull market at this point are the promoters

Disc: Positions in Eimco between 1650-1800. Wocky around 340. Synergy around 290 and Roto 380-400 and rest as disclosed earlier

Ami Organics – Pharma Intermediates & Specialty Chemicals (17-12-2023)

Ami Organics Unveils new manufacturing facility in Ankleshwar, Gujarat

www.bseindia.com/xml-data/corpfiling/AttachLive/21ff97c1-d725-4f04-84da-d97544b537d6.pdf

Rathi Bars – Microcap in steel bull cycle (17-12-2023)

Anyone tracking this stock superb rally

Understanding IT sector (17-12-2023)

Replying this too late, but “AI” being able to write a code without or with minimal human assistance is still tough when we start applying real world use cases.

Personally got a chance to work on a very similar requirement from one of the clients. The solution was not as expected.

Machines still lack the human intelligence nuances – understanding of tones, discussion with business executives, more often clients want us to chip in and help them understand how technology can help. On the other hand, AI needs the user/client to tell them exactly what we want so it can write the “code”.

Business requirements are still messy, full of nuances, constrained by budgets and has elements of common sense. AI will surely reach that level maybe in few more years but not today.

Oriental Carbon and Chemicals Ltd (17-12-2023)

Just use the balance sheet to check the total equity and subtract out any goodwill to get tangible book value.