Can you give some examples of high growth with low ROE/ ROCE companies in large cap and midcap category for study purposes, where value destruction might happen?

Posts tagged Value Pickr

Praj Industries (16-12-2023)

Modi naturals receives Rs 240 Crore Ethanol order (Grain based) from BPCL, IOCL, HPCL

There are 100’s of Grain based 1G- ethanol plants of different sizes are at various stages of operation and as of today, Grain based ethanol comprises of 1/5 th of total ethanol requirement.

Recently, a lot of established players are jumping in to Grain based ethanol (1G). Modi naturals is the latest one-an edible oil company well known (there is a valuepickr thread) has diversified in to Grain based ethanol production which was commissioned in Sept 2023 with a capacity of 250 KLPD. They got their first order of 3.72 Crore litres of ethanol for Rs 240crore.

Bihar is a maize surplus state. There are some 15 megs plants coming up, two of them are already in operation.

There is yet another company Fertiliser cooperative Krishak Bharati Cooperative Ltd (KRIBHCO) is investing around INR 1,100 crore to set up three ethanol manufacturing plants using maize and broken rice as feedstock. These three plants are being set up in Gujarat, Telangana and Andhra Pradesh with a capacity of 250 kilo litre per day.

All this will ease the issue of Sugar ethanol in coming days.

2G ethanol plants are also coming up in big ways. All this will ensure flexibility in getting ethanol for the ambitious petrol blending program and save forex and ensure carbon foot print and sustainability.

For Praj , there would not be any dearth of future orders inflow

Praj Industries (16-12-2023)

Modi naturals receives Rs 240 Crore Ethanol order (Grain based) from BPCL, IOCL, HPCL

There are 100’s of Grain based 1G- ethanol plants of different sizes are at various stages of operation and as of today, Grain based ethanol comprises of 1/5 th of total ethanol requirement.

Recently, a lot of established players are jumping in to Grain based ethanol (1G). Modi naturals is the latest one-an edible oil company well known (there is a valuepickr thread) has diversified in to Grain based ethanol production which was commissioned in Sept 2023 with a capacity of 250 KLPD. They got their first order of 3.72 Crore litres of ethanol for Rs 240crore.

Bihar is a maize surplus state. There are some 15 megs plants coming up, two of them are already in operation.

There is yet another company Fertiliser cooperative Krishak Bharati Cooperative Ltd (KRIBHCO) is investing around INR 1,100 crore to set up three ethanol manufacturing plants using maize and broken rice as feedstock. These three plants are being set up in Gujarat, Telangana and Andhra Pradesh with a capacity of 250 kilo litre per day.

All this will ease the issue of Sugar ethanol in coming days.

2G ethanol plants are also coming up in big ways. All this will ensure flexibility in getting ethanol for the ambitious petrol blending program and save forex and ensure carbon foot print and sustainability.

For Praj , there would not be any dearth of future orders inflow

Uniparts India Limited (16-12-2023)

Uniparts India Limited

OVERVIEW

Uniparts is the global manufacturer of precision parts and systems for off highway vehicles. The off highway vehicles include tractors, ultra terrain vehicles etc, construction and forest machinery (CFM) etc. The company primarily manufactures 3 point linkage systems, precision machine parts and adjacent product verticals like power take offs, hydraulic cylinders etc. These parts are structural and load bearing parts and hence subjected to strict specifications and load tolerances checks.

The company was incorporated in 1994 by first generation entrepreneur Mr. Gurdeep Soni in Ludhiana as a supplier to OEM’s to European players. By 2000, it established its manufacturing facility in Noida. By the mid 2000’s, the company was the major supplier to John Deere. Currently the company has 5 production facilities: 2 in Noida, 2 in Ludhiana & 1 in Vizag. Besides this, the company has 2 warehousing facilities: Augusta & Eldridge.

Business Details

The image attached below is of 3 point linkage. It gets attached to the tractor and carries different equipments like ploughs.

The power take off is an additional attachment which transfers the power from the main machine to the equipment which does not have any power source

Uniparts has an approximately 17% global market share in 3PL systems and 6% global market share in precision machine parts of the CFM industry. Besides this, the company also caters to the aftermarket segment for 3 PL range. Aftermarket means that the company supplies to players like O’Reilley Auto parts so that the customers can come for their requirements post the purchase

Uniparts offer fully integrated engineering solutions from conceptualization, development and validation to implementation and manufacturing of our products. The conceptualization stage involves acquiring market intelligence, assessing customer requirements and formulating customized strategy for individual customers. The development phase includes product designing, material procurement and processing. This is followed by the validation phase, which involves prototyping, testing and feasibility analysis. Revenue from the agricultural segment contributed 70% while CFM contributed 25% of the total revenues.

The clientele is extremely long term with contacts running for 15+years. The company is having the various capabilities under its wing namely forging, machining, welding etc. This enables the OEM’s to get the products designed and developed in house. This is the major competitive advantages where Uniparts is not just the component manufacturer but engages with the client from designing to development phase to offer a high level of customization. As a result, they have over the years introduced several products to product portfolio including rear hitch, front hitch, hydraulic lift arms, PTOs and trailer hitch which allows them to offer integrated system solutions to meet customer requirements and move up the value chain. The major raw material for all the manufactured parts is steel.

UIL follows a global delivery service model with manufacturing facilities and warehouses across geographies. This helps it provide multiple delivery options to its customers, wherein they can either opt for premium priced local delivery (for products manufactured in a nearby plant or stored in a nearby warehouse) and benefit from lower lead time, or for competitively priced offshore delivery (from a relatively low cost manufacturing location, such as India) that entails a higher lead time.

However there are few concerns. There is a big revenue concentration from the top 5 clients. While this sounds a big concern, these clients have been existing with UIL for a long time.

| Uniparts India Limited | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|

| Top Client | 36.87% | 34.15% | 32.78% | 35.21% |

| Top 5 Clients | 61.18% | 58.32% | 56.10% | 56.45% |

| Top 10 Clients | 74.62% | 73.08% | 70.42% | 71.30% |

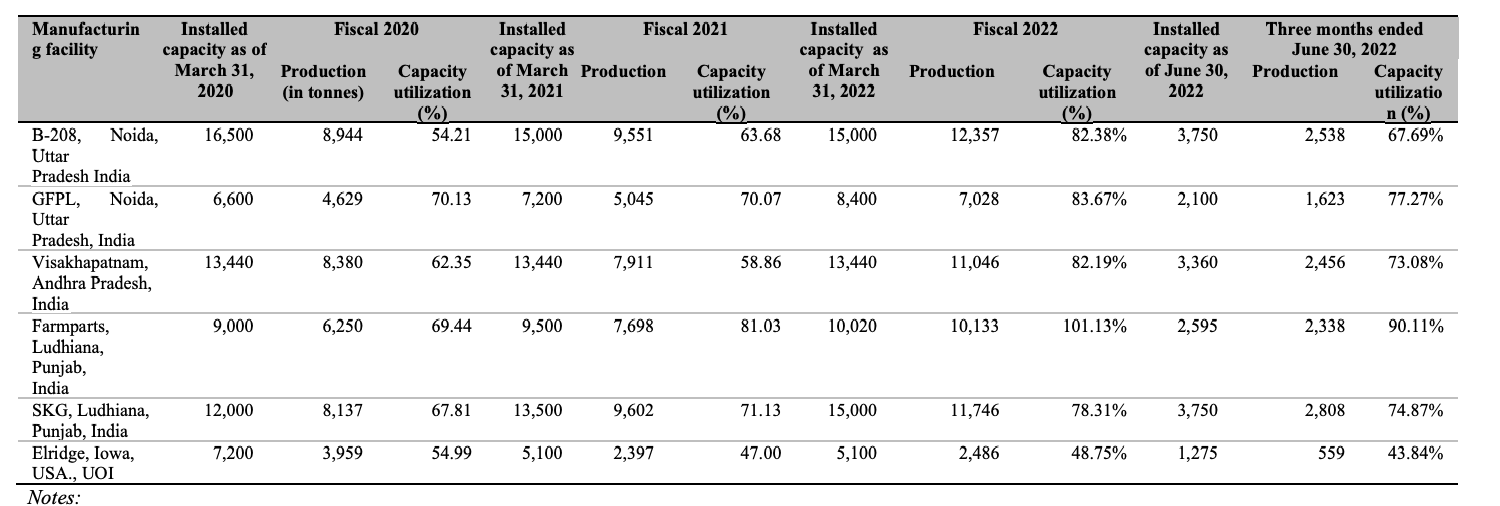

Let’s look at the capacity utilization in their manufacturing units:

Sum total capacity utilization is 76.6% which is pretty high. Now keeping these 2 contexts together, it might be possible that the company has strategically chosen smaller short tail clients so that their capacity utilization remains optimal. Had they started onboarding larger clients, they might have had to undertake the capex. But having said that, the client concentration poses a significant risk at the company level.

One interesting piece to note about this business is that the company used to enter the long term contracts with OHV OEM’s earlier. However with the increasing competition, the OEM’s have to frequently introduce new models or make modifications to existing models. Hence they provide the estimated demand to UIL which further plans its production schedule as per the data which is received. However any unforeseen disruption at OEM operations (like strikes, lockdowns etc.) can have adverse impact at UIL.

The company is cyclical where the sales of its parts depend on the agriculture sector which is further driven by a lot of factors like climate, cost of fertilizers etc. On the other hand the construction segment is driven a lot by macroeconomic policies, interest rates etc.

Financial Details

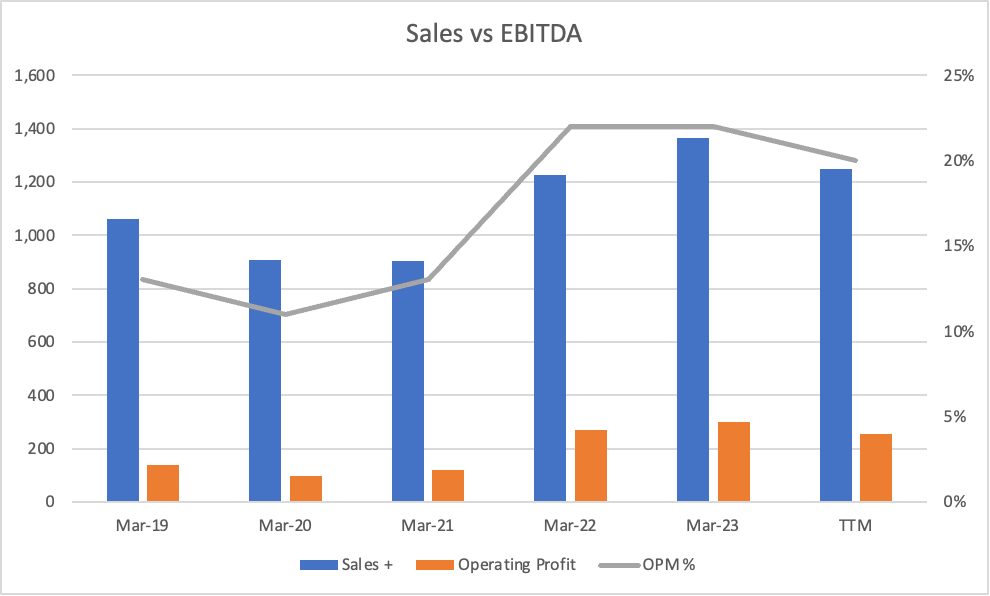

As outlined earlier, the sales are highly cyclical which is seen in the following graph:

The EBITDA margins are shown to be in the cyclical range in the above graph. However, the company is able to pass the raw material and freight rate increase to the customers due to highly specialized ancillary partnership

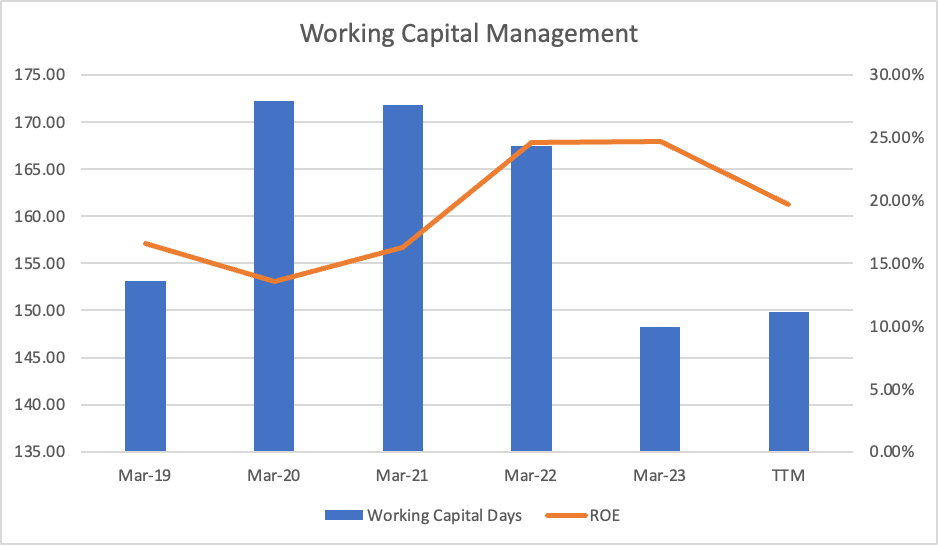

The company is having a working capital cycle of ~150 days which is quite high considering the high dependance on Europe & USA (74%) markets. However, the ROE has been consistently above 20%.

There are net profits of 598 cr from 2019 to 2023 and the net cash flows from operations of 620 cr in the same period indicating a good cashflow conversion situation for the company

Management & Related Party Transactions

The company is led by Mr Gurdeep Soni and Mr Paramjit Soni both of which were paid the salary of Rs 5cr each. The sitting fee amounted to Rs 30 lacs for all the directors in the company. Besides this, there were 3 Key Management Personnels (KMP’s) which were paid Rs 1,82,00,000 as average. The total remuneration comes out to be Rs 15.76 cr (31.82 cr+25cr+30 lacs). This is pretty under the radar considering the net profit of 176 cr.

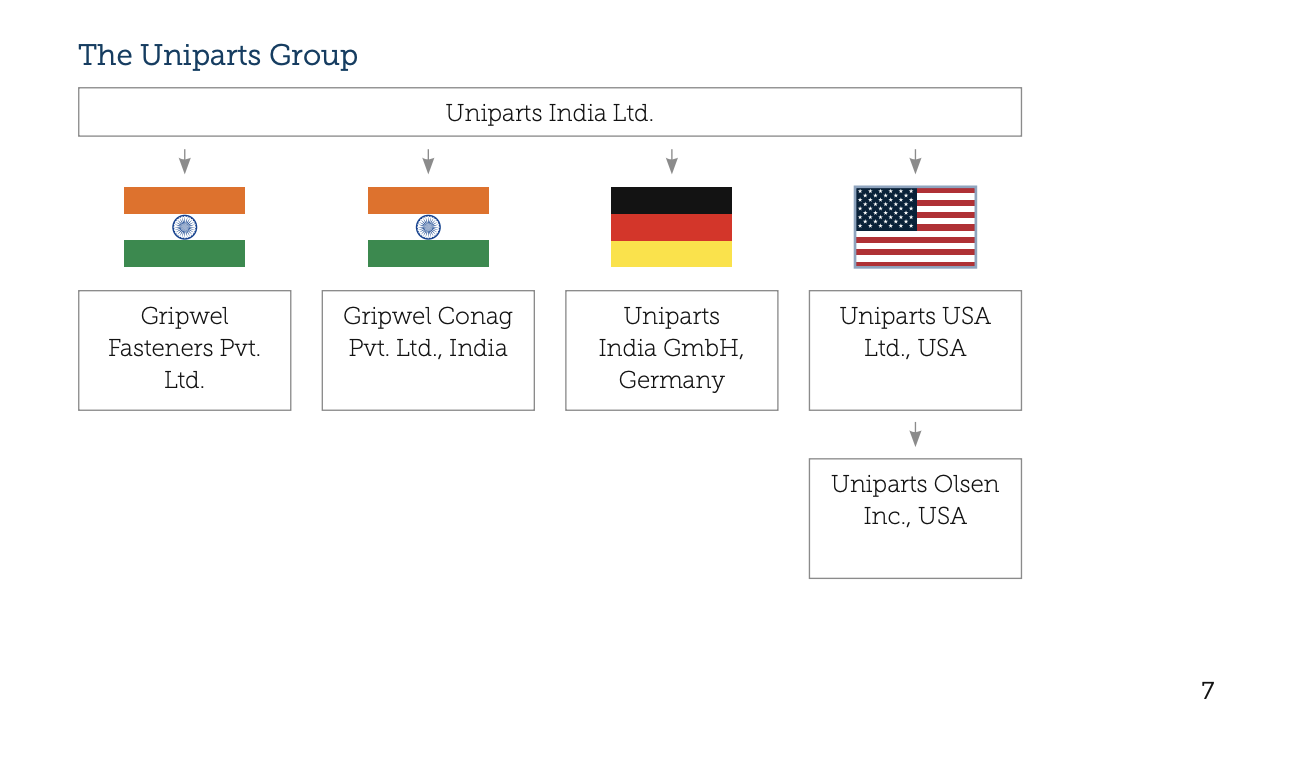

The company’s structure is as follows:

UIL is having 4 subsidiaries which are 100% owned:

- Gripwel Fastners Pvt. Ltd.

- Gripwel Conag Pvt. Ltd.

- Uniparts India GmbH

- Uniparts USA Ltd.

Uniparts USA Ltd. is having a 100% owned subsidiary Uniparts Olsen Inc. The job work of UIL is contracted to Gripwel Fastners and Gripwel Conag which is minute and amounts to 71 lacs. A loan of 5.25 cr was given to Gripwel Conag for working capital against which 3.9 lacs as interest was charged. Other related party transactions look relatively clean

Thesis

- Niche manufacturing and a full scale solutions provider rather than just an ancillary vendor

- Top 5 OHV companies in the USA are the clients of UIL indicating technical expertise (Bobcat, Caterpillar, Case New Holland etc.)

- Focus of the company on ancillary segments like UTV (utility terrain vehicles) and tractors with >70 HP

- Conservative Management, focus on free cash flows, ability to pass hike in raw materials & freight to end customer

- China+1 factor to power the sales of this company

- Revival of US farming sector from 2024 onwards (Link). This is due to the fact that the inflation had eaten into the incomes in 2023 since there was a large stocking which happened in 2022. 2023 was the year of de-stocking for farming sector

- With the China dumping of agrochemicals, the prices are at lower end which is expected to benefit farmers to modernize their equipments

Anti-Thesis

- Cyclicality in both agriculture & CFM sector

- Client Concentration risk where top 5 clients derive 55% of topline

- Short term contracts with OEM’s which can lead to overproduction/underproduction thus leading to adverse impact on bottomline

Valuation & Conclusion:

Since their margins are not impacted owing to the cyclicality of the business, assuming the modest current price to book of 2,8 and price to earnings of 14, there is a lot of room to re-rate. Globally auto ancillaries in the heavy equipment space trade at 5 times book value. With the moat of precision manufacturing, I believe the company has a bandwidth to deliver a fairly decent returns (20%+) CAGR for the next few years to get in line with the global competitors trading metrics.

Credits: @bharatbetpf for the recommendation

Uniparts India Limited (16-12-2023)

Uniparts India Limited

OVERVIEW

Uniparts is the global manufacturer of precision parts and systems for off highway vehicles. The off highway vehicles include tractors, ultra terrain vehicles etc, construction and forest machinery (CFM) etc. The company primarily manufactures 3 point linkage systems, precision machine parts and adjacent product verticals like power take offs, hydraulic cylinders etc. These parts are structural and load bearing parts and hence subjected to strict specifications and load tolerances checks.

The company was incorporated in 1994 by first generation entrepreneur Mr. Gurdeep Soni in Ludhiana as a supplier to OEM’s to European players. By 2000, it established its manufacturing facility in Noida. By the mid 2000’s, the company was the major supplier to John Deere. Currently the company has 5 production facilities: 2 in Noida, 2 in Ludhiana & 1 in Vizag. Besides this, the company has 2 warehousing facilities: Augusta & Eldridge.

Business Details

The image attached below is of 3 point linkage. It gets attached to the tractor and carries different equipments like ploughs.

The power take off is an additional attachment which transfers the power from the main machine to the equipment which does not have any power source

Uniparts has an approximately 17% global market share in 3PL systems and 6% global market share in precision machine parts of the CFM industry. Besides this, the company also caters to the aftermarket segment for 3 PL range. Aftermarket means that the company supplies to players like O’Reilley Auto parts so that the customers can come for their requirements post the purchase

Uniparts offer fully integrated engineering solutions from conceptualization, development and validation to implementation and manufacturing of our products. The conceptualization stage involves acquiring market intelligence, assessing customer requirements and formulating customized strategy for individual customers. The development phase includes product designing, material procurement and processing. This is followed by the validation phase, which involves prototyping, testing and feasibility analysis. Revenue from the agricultural segment contributed 70% while CFM contributed 25% of the total revenues.

The clientele is extremely long term with contacts running for 15+years. The company is having the various capabilities under its wing namely forging, machining, welding etc. This enables the OEM’s to get the products designed and developed in house. This is the major competitive advantages where Uniparts is not just the component manufacturer but engages with the client from designing to development phase to offer a high level of customization. As a result, they have over the years introduced several products to product portfolio including rear hitch, front hitch, hydraulic lift arms, PTOs and trailer hitch which allows them to offer integrated system solutions to meet customer requirements and move up the value chain. The major raw material for all the manufactured parts is steel.

UIL follows a global delivery service model with manufacturing facilities and warehouses across geographies. This helps it provide multiple delivery options to its customers, wherein they can either opt for premium priced local delivery (for products manufactured in a nearby plant or stored in a nearby warehouse) and benefit from lower lead time, or for competitively priced offshore delivery (from a relatively low cost manufacturing location, such as India) that entails a higher lead time.

However there are few concerns. There is a big revenue concentration from the top 5 clients. While this sounds a big concern, these clients have been existing with UIL for a long time.

| Uniparts India Limited | 2020 | 2021 | 2022 | 2023 |

|---|---|---|---|---|

| Top Client | 36.87% | 34.15% | 32.78% | 35.21% |

| Top 5 Clients | 61.18% | 58.32% | 56.10% | 56.45% |

| Top 10 Clients | 74.62% | 73.08% | 70.42% | 71.30% |

Let’s look at the capacity utilization in their manufacturing units:

Sum total capacity utilization is 76.6% which is pretty high. Now keeping these 2 contexts together, it might be possible that the company has strategically chosen smaller short tail clients so that their capacity utilization remains optimal. Had they started onboarding larger clients, they might have had to undertake the capex. But having said that, the client concentration poses a significant risk at the company level.

One interesting piece to note about this business is that the company used to enter the long term contracts with OHV OEM’s earlier. However with the increasing competition, the OEM’s have to frequently introduce new models or make modifications to existing models. Hence they provide the estimated demand to UIL which further plans its production schedule as per the data which is received. However any unforeseen disruption at OEM operations (like strikes, lockdowns etc.) can have adverse impact at UIL.

The company is cyclical where the sales of its parts depend on the agriculture sector which is further driven by a lot of factors like climate, cost of fertilizers etc. On the other hand the construction segment is driven a lot by macroeconomic policies, interest rates etc.

Financial Details

As outlined earlier, the sales are highly cyclical which is seen in the following graph:

The EBITDA margins are shown to be in the cyclical range in the above graph. However, the company is able to pass the raw material and freight rate increase to the customers due to highly specialized ancillary partnership

The company is having a working capital cycle of ~150 days which is quite high considering the high dependance on Europe & USA (74%) markets. However, the ROE has been consistently above 20%.

There are net profits of 598 cr from 2019 to 2023 and the net cash flows from operations of 620 cr in the same period indicating a good cashflow conversion situation for the company

Management & Related Party Transactions

The company is led by Mr Gurdeep Soni and Mr Paramjit Soni both of which were paid the salary of Rs 5cr each. The sitting fee amounted to Rs 30 lacs for all the directors in the company. Besides this, there were 3 Key Management Personnels (KMP’s) which were paid Rs 1,82,00,000 as average. The total remuneration comes out to be Rs 15.76 cr (31.82 cr+25cr+30 lacs). This is pretty under the radar considering the net profit of 176 cr.

The company’s structure is as follows:

UIL is having 4 subsidiaries which are 100% owned:

- Gripwel Fastners Pvt. Ltd.

- Gripwel Conag Pvt. Ltd.

- Uniparts India GmbH

- Uniparts USA Ltd.

Uniparts USA Ltd. is having a 100% owned subsidiary Uniparts Olsen Inc. The job work of UIL is contracted to Gripwel Fastners and Gripwel Conag which is minute and amounts to 71 lacs. A loan of 5.25 cr was given to Gripwel Conag for working capital against which 3.9 lacs as interest was charged. Other related party transactions look relatively clean

Thesis

- Niche manufacturing and a full scale solutions provider rather than just an ancillary vendor

- Top 5 OHV companies in the USA are the clients of UIL indicating technical expertise (Bobcat, Caterpillar, Case New Holland etc.)

- Focus of the company on ancillary segments like UTV (utility terrain vehicles) and tractors with >70 HP

- Conservative Management, focus on free cash flows, ability to pass hike in raw materials & freight to end customer

- China+1 factor to power the sales of this company

- Revival of US farming sector from 2024 onwards (Link). This is due to the fact that the inflation had eaten into the incomes in 2023 since there was a large stocking which happened in 2022. 2023 was the year of de-stocking for farming sector

- With the China dumping of agrochemicals, the prices are at lower end which is expected to benefit farmers to modernize their equipments

Anti-Thesis

- Cyclicality in both agriculture & CFM sector

- Client Concentration risk where top 5 clients derive 55% of topline

- Short term contracts with OEM’s which can lead to overproduction/underproduction thus leading to adverse impact on bottomline

Valuation & Conclusion:

Since their margins are not impacted owing to the cyclicality of the business, assuming the modest current price to book of 2,8 and price to earnings of 14, there is a lot of room to re-rate. Globally auto ancillaries in the heavy equipment space trade at 5 times book value. With the moat of precision manufacturing, I believe the company has a bandwidth to deliver a fairly decent returns (20%+) CAGR for the next few years to get in line with the global competitors trading metrics.

Credits: @bharatbetpf for the recommendation

Hitesh portfolio (16-12-2023)

The only real answer I can give on this is – judge your Passion-level!

At times, even though we may underperform an index in any given year, we are so passionate about doing our own researches, understanding the world better, and hence connecting the dots in making our own decisions that we could accept sub-optimal returns in a short-to-mid-term viewpoint. Hopefully our passion makes up for that over the long term, through increased happiness in pursuing this journey (which may hopefully translate to outperformance over a long term)!

If the goal is purely the outcome, and to beat or match indexes, then the decision is usually easy – avoid exposure to direct-to-equities.

Hitesh portfolio (16-12-2023)

The only real answer I can give on this is – judge your Passion-level!

At times, even though we may underperform an index in any given year, we are so passionate about doing our own researches, understanding the world better, and hence connecting the dots in making our own decisions that we could accept sub-optimal returns in a short-to-mid-term viewpoint. Hopefully our passion makes up for that over the long term, through increased happiness in pursuing this journey (which may hopefully translate to outperformance over a long term)!

If the goal is purely the outcome, and to beat or match indexes, then the decision is usually easy – avoid exposure to direct-to-equities.

Vineet Jain portfolio (15-12-2023)

Life update and musings on investment philosoply

The last couple of months have been all about adjusting to this new life in the US. My wife got a job with her employer (PepsiCo) here and we moved. I have put my papers in woth the Tatas after a 9.5 years stint with the Tata Administrative Services, in which I did exciting roles across the Tata Trusts, a long secondment to the Government of India, and the last two years at Tata Consumer Products.

As with most notice periods, work has been slow and a lot of time has been spent reflecting on on what I want to do next in my career, what opportunities I should look for in the US, and networking across the board. From an investing standpoint, one not so intuitive benefit of being here has been that I spend very less time awake when the Indian markets are open, and so I spend less time drooling over the screen and over-trading, and much more reading about businesses and refining my investment philosophy when the markets are closed ![]()

I have made a few changes to my portfolio, which i will post about separately (Hopefully it won’tget flagged like last time. I still can’t believe someone flagged my portfolio update!!). The general principle has been to conventrate into businesses in sectors experiencing tailwinds, with clean balance sheets (net cash is preferable), good management pedigree and reasonable valuations. If there is a trigger coming up, I have raised allocation aggressively. Like most people, my portfolio has done very well this year, with more than 2x of what it was on 1st April, and 85% up from 1st Jan.

Of all the investing content I have consumed in the last two months, I enjoyed the Motilal Oswal Wealth Creation Study 2023 the most.

They key take way for me was that high earnings growth at low RoE is not necessarily value additive, especially if the RoE is lower than the cost of equity. These businesses do not get sustained high valuations, even at high growth, and rightly so. And so, economic profits are more important than accounting profits. In present markets, we are seeing many companies growing fast at low RoEs. That is actually value destructive and the water will find its level.

The best returns are made when good growth comes at high RoE (or ROCE if you please, so long as debt is not too high and destabalizing with risk). If RoEs improve as well while earnings grow, you’re sitting on a hockey stick. Usually happens at the intersection of a trending sector, a business with a competitive edge (call it moat or right to win if you please), and a trigger.

In a way, RoE is a measure of the “quality” of a business, signifying it’s potential to add value. If a business can sustain high RoEs, it means that they are not easy to replace, and signals longevity, which is an anecdotal way to justify high valuations, provided there is growth.

Reminds me of a line that line thay Basant Maheshwari uses often. High RoE is like a Ferrari, high growth is like petrol. If you have both, you can speed with ease.

More details on the portfolio to come soon . . .

Capacit’e Infraprojects (15-12-2023)

4% dilution with conversion of warrants by Rohit and Sakshi last week. Some additional cash infusion in the process, and the price has remained flat, and in fact has gone up 3-4% since last week. Good signs.

IREDA: Renewable Energy Powerhouse (15-12-2023)

Keep monitoring few metrics like: GNPA, NNPA, NIM, ROA which are important to track in case of financial companies.

Many listed players are funded by IREDA (like websol i know of)