Monday sugar sector will be up again !!

Posts tagged Value Pickr

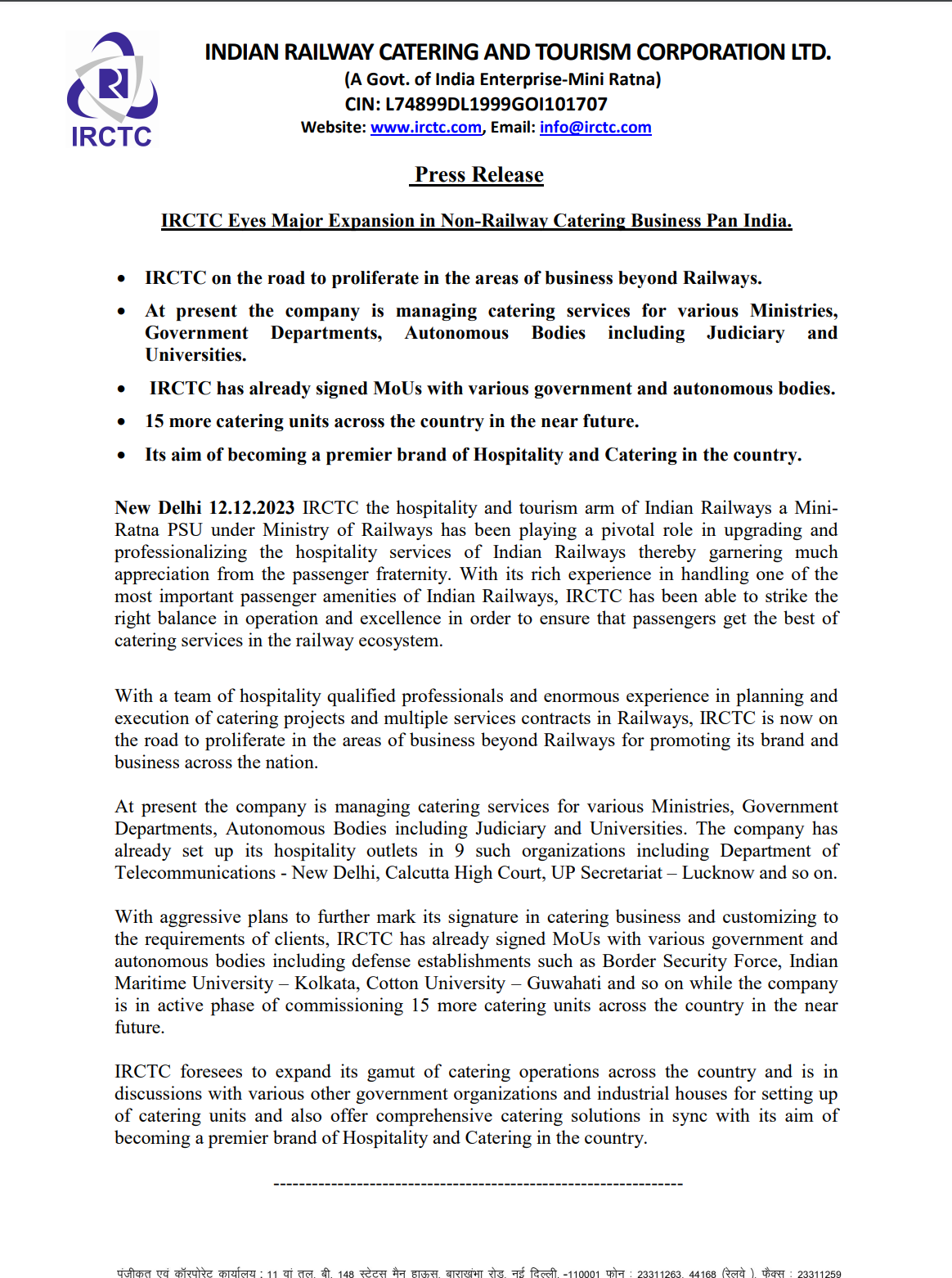

IRCTC: a necessity, a monopoly (15-12-2023)

“IRCTC Eyes Major Expansion in Non-Railway Catering Business Pan India

IRCTC, which is the hospitality and tourism branch of Indian Railways, is expanding its business beyond just managing catering services for trains. Currently, it is providing catering services to different government departments, ministries, autonomous bodies, and universities. They have even set up outlets in places like the Department of Telecommunications in New Delhi and the Calcutta High Court.

IRCTC is planning to grow its catering business even further. They have signed agreements with various government and autonomous bodies, including defense establishments like the Border Security Force and educational institutions like the Indian Maritime University and Cotton University. The company is also in the process of establishing 15 more catering units across the country soon.

The ultimate goal of IRCTC is to become a top brand in hospitality and catering throughout the country. They are in talks with other government organizations and businesses to set up more catering units and provide comprehensive catering solutions. The idea is to bring their expertise and quality service beyond just the railway system and make a mark in the broader hospitality industry.

HBL POWER SYSTEMS: Booting-up for the Race of the Century (15-12-2023)

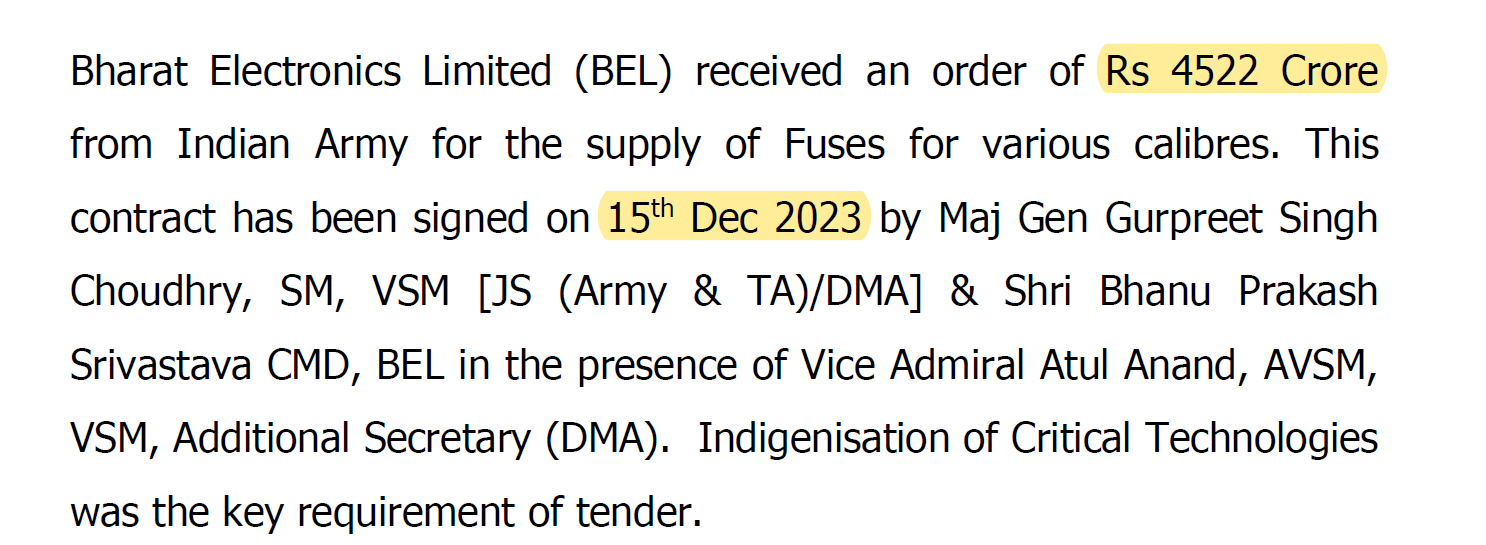

BEL won the electronic fuze order from Indian Amry. Will be interesting to see, if HBL has any role here.

Dollar Industries ltd – Fit Hai Boss (15-12-2023)

Excellent analysis. Well done.

If they do 1500cr this year, then 2800cr should come sooner than FY28, ideally. If it takes that long, then it’s a bit of slow growth ?

Would love to see you break down Skipper Ltd.

Ajay Upadhyay is a common investor in both Dollar & Skipper, and is know for picking odd gems.

IRM Energy – A new kid on the (listed CGD) block (15-12-2023)

Cadila Pharma Promoter – in pharma circle the company do not have very good credential to talk about. To attract talent is a steep task to expect from that company. Cadila Pharma-Torrent Pharma-Zydus Cadila-Intas : all were at same levels (Infact Cadila pharma was ahead) in early 2000. Zydus Cadila and Cadila Healthcare promoters were partners if I am not wrong (hence Zydus Cadila & Cadila Pharma). Then the rest is history.

My only point was – as your message implied Cadila Pharma promoter means something positive, in my view and anyone in pharma industry will say its a negative, to say the least.

Pricol limited – OEM automotive (15-12-2023)

They still hold around 3.3% of Pricol Ltd. after the recent sale to Goldman Sachs.

Attached information:

2DDBC704_D1DE_49F6_BF4E_326D9F8F3735_163914 (1).pdf (2.3 MB)

Chins’ Portfolio (15-12-2023)

In the last week, I have taken a 6% position in Dollar Industries.

I had a discussion with a former employee at Rupa, and my goal was to better understand the innerwear cycle, where we are right now, and a channel check of the current demand. In this conversation, he spoke about Dollar Industries unprompted, and proceeded to explain in the next hour why Dollar has the most differentiated model within the economy innerwear segment.

Prior to this call, I was of the opinion that the chaddi companies were all the same, there was not much differentiating them, and the play is largely mean reversion in the cycle. I now am of the opinion that we’ve stumbled upon a story whose gravity is only visible through scuttlebutt.

I think Dollar therefore is a perfect candidate for a long term position in my portfolio, with the one risk of being a year or two early to the story. It fits my bill of being in an out of favour sector, and the thesis is not very transparent unless one is looking closely. Indeed without this coming from a competitor’s mouth, I may not have paid as close attention.

I have shared my thesis of Dollar Industries on the company thread below.

Menon Bearings: Gaining Traction both operationally and stock wise (15-12-2023)

Even on margins, the brakes segment is not attractive. Rane, Sundaram are making single digit operating margins. But in the Q4 FY23 concall, the management said they will make 18 – 19 % EBIDTA margins.

It is not clear on what basis they said they will generate 18-19 % EBIDTA margins, so I wrote to the management. They replied that 18 – 19 % are gross margins. Then when I pointed out that they had earlier said these are EBIDTA margins, they replied that “since the set-up and project is new, other expenses are less and hence there is little difference between Gross & EBIDTA Margins”.

Overall, looking at Rane Brake Linings or Sundaram Brake Linings, brakes does not seem to be an attractive segment to get into.

(Disc.: No positions)

Dollar Industries ltd – Fit Hai Boss (15-12-2023)

I think there is a deep structural shift in Dollar Industries currently underway. The gravity of this shift has been missed by the broader market.

Claim: Dollar Industries has the right to win distribution model in the industry, and the growth / return ratios may look very different in the medium term.

Legacy Distribution Models

There are five innerwear companies that operate in the economy segment – Rupa, Dollar, Lux, Dixcy and JGH (Amul Macho). These five have conventionally used a traditional distribution framework.

Here, a company produces products at their factory, and then gives these products to a distributor. Distributors then make a small margin and pass on the products to a customer facing retailer. These distributors usually make 6-8% margins, and are given 3-4 months of credit before they need to pay a Rupa or a Lux.

Now, these companies often have no visibility on their end customers beyond the distributors and have no control on the particular SKUs that are being sold. They keep sending products into the channel, and hope the market absorbs the supply. On the distributor’s side, one distributor may cater to 2-3 brands, and will push the product that gives them the highest margin at the time. There is also no organisation between the retailers a particular distributor sells to, so you may have more than one distributor selling to a retailer.

During periods of downturn in the industry, this messy distribution model turns ugly. Distributors start undercutting each other, and margins fall from 6-8% to 2-3% seen in the last year! Companies like Amul and Rupa have also tried to cut down their working capital, and have demanded their money back from distributors within 21-30 days! As a result, distributors are squeezed at both ends, dissatisfied, and the inventory turns have suffered.

Dollar’s Distribution Model

In 2019, Dollar started a pilot project to implement a completely different distribution model. They mapped out all the retailers in a particular area, and mapped these retailers to a particular distributor. They gave distributors fixed margins of 6-10%, and implemented a system to track inventories, particular SKUs, and would know which part of the country needed replenishment.

They also took charge of the demand generation entirely, building a large call centre, where they regularly do a lot of ground work in reaching the retailer, telling them about promotions, etc. This means the distributors don’t have to undercut each other, don’t have to lower their margins, but instead focus purely on distribution, and are incentivised with things like loyalty points.

The benefits of this system are obvious: less stress on the channel, controlled levels of inventory, control over the SKUs that are pushed, visibility and data on the end customer, and distributors that are happy and empowered with stability, and extra incentives with the reward programme.

From scuttlebutt, I believe this model has been incredibly successful. In Rajasthan, they were able to double their market share in 2-3 years, and have since been replicating this in other states. Today, some 20% of the distributors have been brought under this model.

Proof in the Pudding

If you want to read about Dollar, the annual reports are the place to start. If you want to understand Dollar, search for @ankush12495 in each of the concalls. He’s done some brilliant work, and has been first to this idea, I believe.

In various calls, Dollar has given numbers on the difference between the old distribution network and the new one.

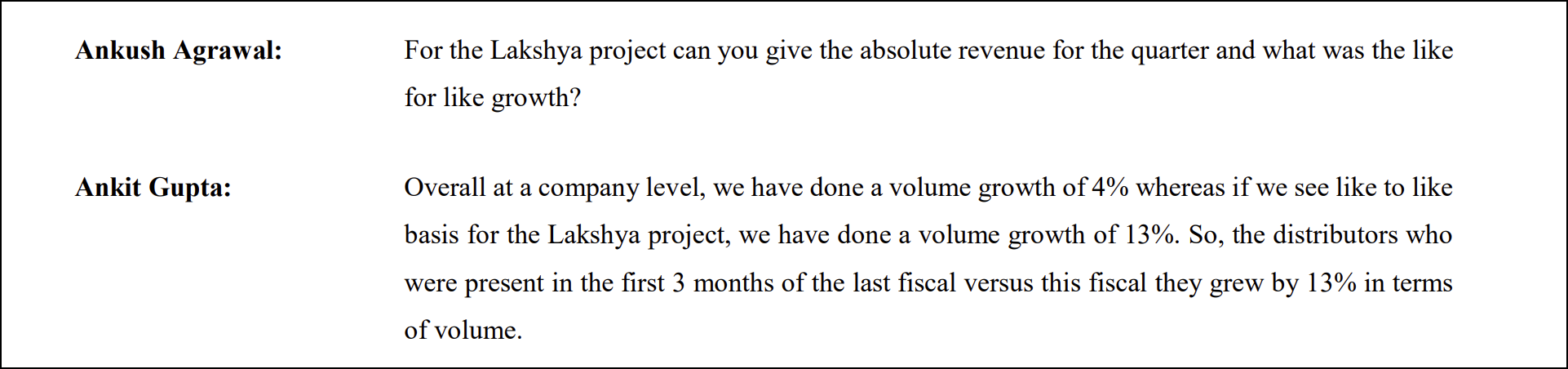

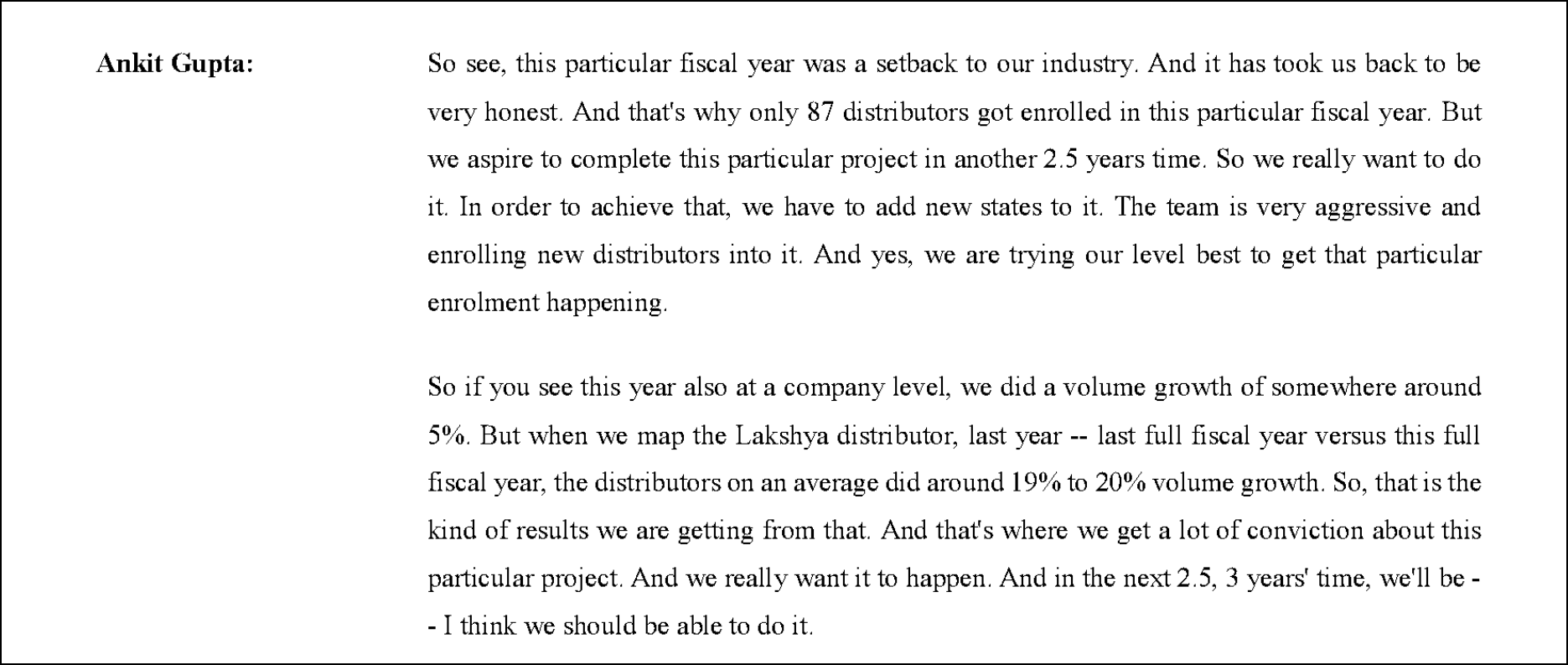

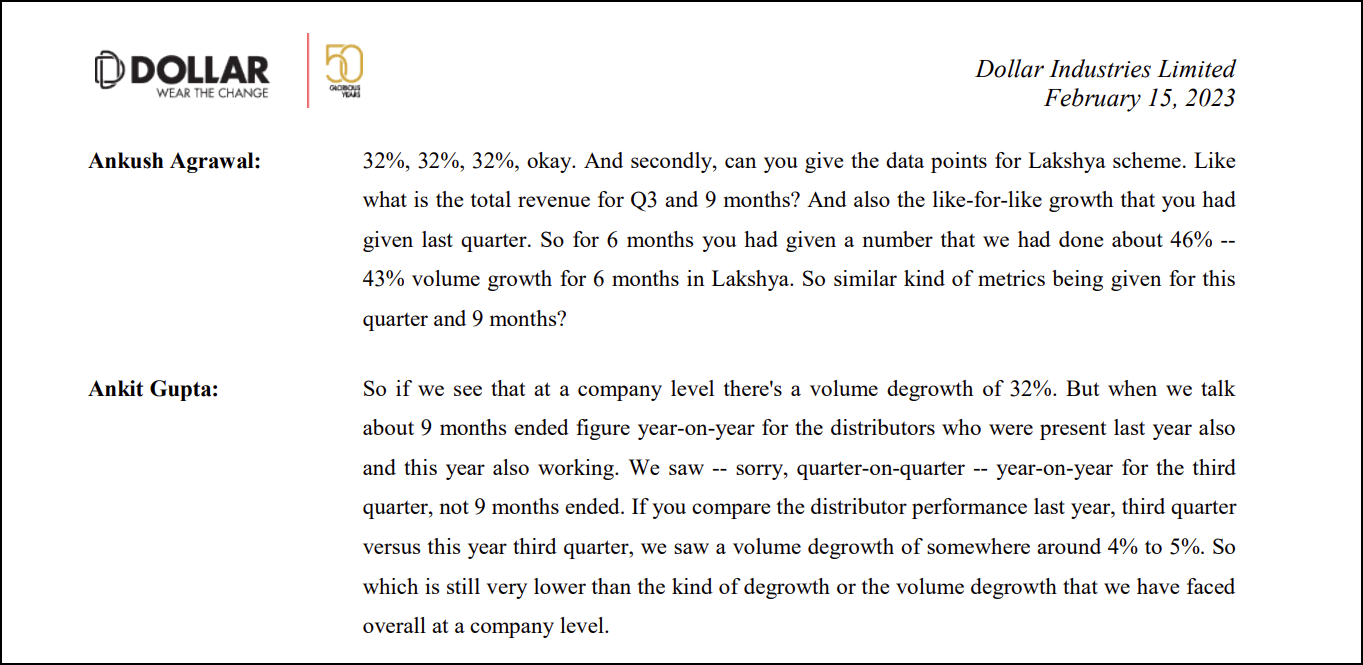

Q2FY24

Q1FY24

FY23 vs FY22

Q3FY23

The new distribution model has outperformed the legacy model by double digits in volume growth. The most dramatic data point is in the last image, where the company’s volumes fell 32% YoY, the new model only lost volumes by 4% in the same period, an alpha of 28%.

What makes a moat?

Dollar has spent 4 years in bringing nearly 300 distributors on to this new model. They’ve explained that it is a very careful procedure that needs to be done, taking 3-4 months to bring on a single distributor. They cannot interrupt ongoing sales as this would lose market share, and therefore the roll out is very slow.

Bringing more distributors under this model is vital to capturing market share, improving the return ratios, etc. By my estimates, at their current pace of adding 100 distributors a year, the contribution from the new distribution model will look something like this:

| Year | Percentage of Distributors Under Lakshya |

|---|---|

| FY24 | 30% |

| FY25 | 40% |

| FY26 | 50% |

| FY27 | 60% |

| FY28 | 70% |

Because the number of distributors under this model is still only 25%, we don’t yet see the benefits of Project Lakshya in the numbers. However, once we cross FY26 and the majority of distributors are brought in, things can look very different.

This is exactly the sort of thing that moats are built out of. If it takes 10 years to roll out a complex change to your distribution model, it is very difficult to replicate and execute. It’s a testament to Dollar’s management that they’ve been this forward looking to continue with this rollout for 4-5 years now.

Infighting

There are five innerwear companies that operate in the economy segment – Rupa, Dollar, Lux, Dixcy and JGH (Amul Macho). These five have conventionally used a traditional distribution framework.

Another rather lucky fact rumour in Dollar’s favour right now is that all of the remaining four companies have divides in the second and third generations in the family. Lux’s divide is probably the most public, but I have heard that this is present across Rupa, Dixcy and JGH as well. If the rumours are true, it’s another barrier that adds to a competitor having the wherewithal to implement a complete redesign of a distribution model.

Valuations and Outlook

Today, at ~1.7x sales, the valuations are undemanding if this structural change in Dollar plays out. Once Project Lakshya accounts for more than 50% of the distributors, I would expect Dollar’s growth rates to rise higher than the industry. It is also a fallacy to compare valuations to what Dollar has historically traded at, given the difference in the company before and after 2019/20.

As a rough sketch, I think it is possible for Dollar to get to 2800 Cr. revenues by FY28. Hopefully by then, RoCEs should improve to north of 30% if this is successful, and if the industry comes back into favour, I can imagine a multiple of 3-4 times sales if the market agrees with the differentiation. Therefore, I’d expect around 11-12k Cr. market cap by FY28.

All of these insights came from a scuttlebutt discussion with the former employee of Rupa, currently at JGH. Thanks to @nirvana_laha, @Lynch and @yrm91 for their efforts in working on the company with me.

Disclosure: Invested, transactions in the last 30 days.