screener.in is one of the websites where you can build your own queries with technical parameters like ROCE, ROE, PAT etc. and get the list of companies satisfying that

Posts tagged Value Pickr

Clean Science and Technology Limited (CSTL) – A clean and green future ahead (17-10-2024)

If valuations are higher. I prefer to wait at my buying range. It is an individual decision driven by many factors for me which is opportunity cost.

Regards,

Sterling & Wilson Solar Ltd. – Will the Sun Keep Shining? (17-10-2024)

Company Profile: The company provides EPC and O&M services under turnkey EPC and BoS solutions for utility-scale, rooftop, and floating solar power projects. It also offers solar plus storage solutions. It boasts an EPC portfolio of 19.4 GWp and an O&M portfolio of 8.2 GWp. It has a presence across 28 countries.

a) Q2 FY25 results: The company’s Q2 FY25 revenues stood at Rs 1,031 crores, up 36% YoY and 13% QoQ, aided by higher execution in domestic EPC projects. Gross margins stood at 10.1% versus 8.6% YoY (11.1% QoQ). With the legacy international projects behind, gross margins are likely to trend at around 10% levels. EBITDA stood at Rs 51 crores, up 283% YoY. EBITDA margin stood at 4.9% versus 2.3% YoY. PAT stood at Rs 9 crore versus a loss of Rs 54 crores YoY. The company posted a third consecutive quarter of positive EBITDA, PBT, and PAT at a consolidated level.

B) Orderbook and order inflows: The company’s order book stood at Rs 10,549 crores as of Q2 FY25 versus Rs 9,396 crores as of Q1 FY25. Order inflows in Q2 FY25 stood at Rs 2,044 crores versus Rs 2,170 crores in Q1 FY25. 77.8% of the unexecuted order book is domestic, while 11% is from Europe and South Africa each. Also, the company has an active bid pipeline of 27.8 GW.

C) Debt status: The company’s net debt has increased to Rs 326 crores as of Q2 FY25 versus Rs 97 crores as of Q1 FY25 due to a new credit facility worth Rs 500 crores availed by IREDA (at 11.6% interest rate). The indemnity proceeds of Rs 109 crores will be used to pay off H2 FY25 debt repayments. The company’s net working capital continues to remain negative at Rs 543 crores. The company’s ratings have been upgraded to investment grade by Acuite Ratings.

D) Management outlook: The following is the outlook provided by the management:

-

The company is well on track to meet its full year order inflow guidance of Rs 8,000 crores as it has already received orders worth Rs 4,000+ crores in H1 FY25. The company’s win rate in H1 FY25 stood 46%.

-

The company has won India’s largest order BESS project worth 1 GWh from the JSW group. The addressable market for BESS and PSP is huge in India.

-

It also anticipates a strong pickup in execution in H2 FY25 and has all the building blocks in place to meet its revenue guidance of Rs 8000 crores. This will be led by projects in Khavda worth 4 GW and some projects in Rajasthan. On a very conservative basis, the company can grow at a CAGR of 15-20%.

-

Gross margins for the EPC business are expected to remain in the range of 10-11% and around 25% for the O&M business. EBITDA margins are expected to inch higher towards 7-8% as revenue increases and recurring overheads remain constant.

-

As a change in strategy, the company is now also considering turnkey projects i.e. projects with module supply for various public sector customers. However, the company is now purchasing these modules from tier 1 Indian suppliers immediately after the order is received. The procurement earlier used to happen from China. Hence there is no price risk as of now.

-

With regards to the indemnity proceeds, Rs 109 crores have been billed to the promoters as on 30th September’24, which is to be received by 30th November’24. Also, the company expects to realize Rs 800 crores of indemnity proceeds within the next 24-36 months.

-

The Reliance pilot project will be completed by Q3 FY25 and post that it will roll out new projects.

-

With respect to the Nigeria order, contract signing is awaited. The company’s partner Sun Africa has recently signed two projects in Africa funded by the US EXIM bank. The management expects to sign this order very soon. Financial closure will further take 6-9 months from the signing date.

E) Key monitorables: The following are the key monitorables for the company:

-

The management has repeatedly reiterated that order inflows in the business could be lumpy.

-

Mr. Khurshed Daruvala has committed to be a long term player in the company and there will be no further stake sale by him. SWSOLAR’s stock taked 8% in 2 days when the SP group and Khurshed Daruvala sold about 7% stake in the company.

-

The progress on the Nigeria order remains a key monitorable.

The Ideal Investment Thesis (17-10-2024)

Hey @ankurgupta, I would love to know the websites and tools to get the data you mentioned, could you please help me with it

Buy Unlisted Shares (17-10-2024)

sir what is the ur view on upcoming waaree ipo is it worth it or not ? wiil it be a multibagger in 04 to 5 yrs

The Ideal Investment Thesis (17-10-2024)

Excellent investment hypothesis.

I wish to add a few points;

- If we look for revenue growth or any metrics over 5 years, we miss out on the new businesses.

- Valuation over last 5 years should less than 30!! Why? How is past valuation relevant?

Pokarna Limited: (17-10-2024)

Pokarna

FY25 Guidance

Quartz Segment will see strong growth

-

REV & PAT Growth 30-35 %

-

EBITDA Margins 30-35 %

-

Looking to exit apparel business

Axiscades Mistral Technologies Limited – Hidden Defence Story (17-10-2024)

Mistral Drone trial at Him-Drone-A-Thon:

Pawan Vashishth GM Mistral Solutions speaking with ADU at Him-Drone-a-thon

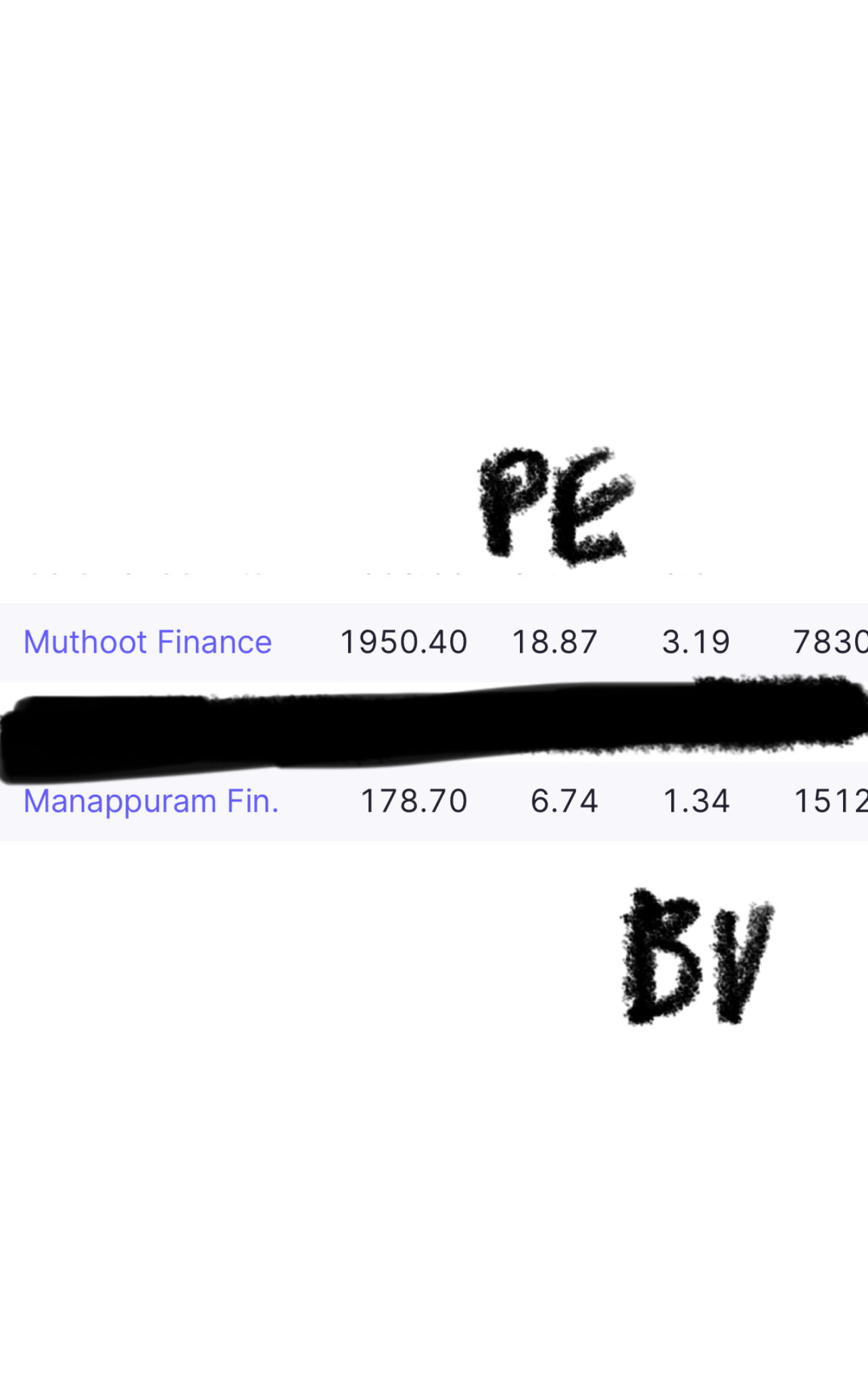

Manappuram Finance (17-10-2024)

Pessimism tends to be quite strong in this stock. However, as long as the EPS and book value continue to grow while NPAs remain manageable, it’s not a major concern. The price can quickly adjust, often within just a week or a few trading sessions. Currently, it’s trading at about 1.3 times the book value and PE 6.7 , so I believe the downside risk is fairly limited at this point. It’s hard to catch the absolute bottom, but I feel this is near it

Results on 5th November

Sakar Healthcare – Tiny Pharma Company for promising Growth ahead (17-10-2024)

Hello guys,

i had two questions –

-

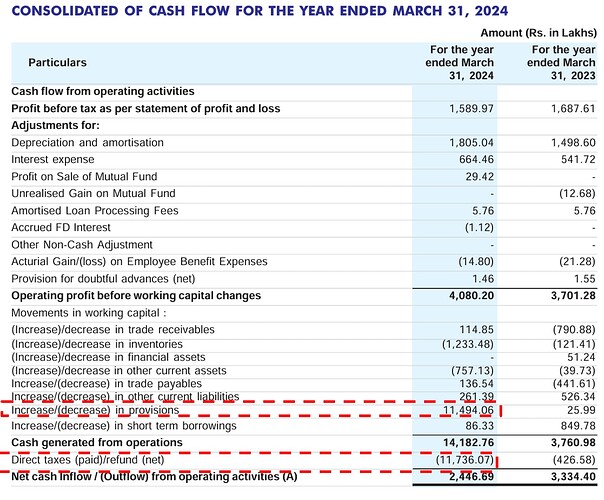

As per the AR 2024 cash flow statement they received ~Rs 115 crs via increase in provision and there was a tax cash outflow of Rs ~117 crs – can anyone clarify on this transaction as there is nothing in balance sheet provisions and notes – Attaching screenshot below for reference –

-

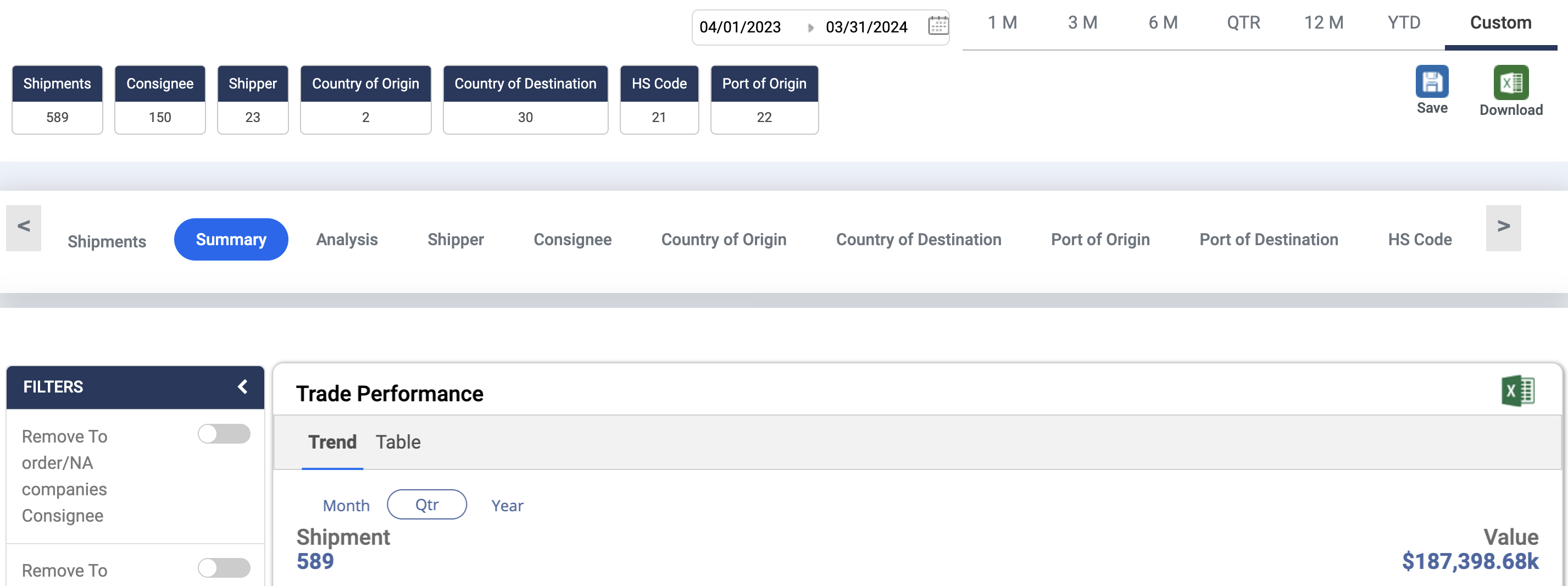

I was checking Sakar healthcare’s export data on Volza – as per company’s AR 2024 – they exported goods worth Rs 94 crs – but as per the volza portal the exports were to the tune of ~$ 187 mn which translates to ~Rs 1500 crs – there were six sakar healthcares with same address – couldnt find anyother company online which could also be named Sakar Healthcare and all these shipments source country was India – Anyone has any idea what is it that i am doing wrong here – Attaching screen shots of volza below for reference –

Thank You