I was not trying to analyze the stock. I have always believed that it does not deserve the sky high PE. Now as well as in the past. What I do know from first-hand experience is for a B2C company, consistent quality of all its products, especially when they are sold under the flagship brand name, is paramount to its survival and growth. The % share of a product in total sales is irrelevant.

As far as Caratlane purchase consideration goes, my comment is, shareholders and the market gives a long rope to its darlings. How many minority shareholders go through the trouble of voting on resolutions?

Posts tagged Value Pickr

Titan Company Ltd : a three decade old company (08-12-2023)

Embassy REIT: Is this “Blackstone” promoted REIT is real diamond? (08-12-2023)

Yesterday’s accounced SEZ reform is welcomed by the REIT’s. Based on comments from Reit’s leaders, this will help increase the occupancy.

Infact, in the recent concalls, Embassy and Brookfield management were stressing, the need of this reform and were making representation to the government.

My naive question, why does it matter for the prospective leasor whether its SEZ area or non SEZ. What are the clauses in SEZ area that no one seams interested in leasing these assets now?

I understand SEZ do not offer export tax incentives anymore, but how does it matter if the prospective leasor is not looking for it anyways.

@dd1474 Can you provide some insights please?

Sorry, probably its a silly question, but I am not able to get the crux of the matter.

Amit

Rural Elect Corp (08-12-2023)

Not denying that REC / PFC are veterans in financing power sectors since decades.

As I can see from their website, IREDA can also finance utility scale power projects that REC PFC are mandated to finance , but IREDA would focus mainly on100% renewals. REC PFC can do both thermal & renewable & more recently infra projects also.

Further additionally IREDA can also finance micro renewable projects such as Bio-gas , Bio-ethanol, Roof top solar for individuals , societies , small medium offices. Even EV …

Perhaps Mr. market gives a thumbs up to its 100% commitment to renewables , which is currently fancied by investors.

However , few quarters down the line only Financial performance would decide the valuation.

Discl: holding REC PFC since high Dividend yield period of 11-12%. IREDA I got a small allotment through IPO which I am holding. Would like to add further in declines

Not a buy or sell recommendation. Please do your own assessment before investing

Gensol Engineering – A play on Energy Transition (Solar Energy & EV) (08-12-2023)

Sorry was my mistake in interpreting it! Here’s what I had seen https://www.youtube.com/watch?time_continue=97&v=fHK-y51Hbag&embeds_referring_euri=https%3A%2F%2Ftwitter.com%2F&source_ve_path=MTM5MTE3LDEzOTExNywyODY2Ng&feature=emb_logo

INOX Wind (08-12-2023)

Thanks for this update.

This is indeed big and very good developement.

It emphasizes goverment’s willingness to improve wind energy capacity as well as efficiency by replacing old inefficient windmils…

Bhansali Engineering Polymers – An Import Substitution Story! (08-12-2023)

Second last paragraph:

As capacity expansion is ‘Need of the Hour’, the Management will endeavour to implement the project within the shortest possible duration of 18 months i.e. by September 2025. In any case, the project will certainly be completed latest by March 2026, with an estimated Capex of Rs.250 crore.

So the earlier target of Dec 2024 for implementation of capex is now shifted to Sep 2025 – March 2026. Is that what it means?

MOLD TEK PACKAGING—dividend plus growth (08-12-2023)

Agreed completely.

Moldtek is not present in entry level Paints segment.

Abnormal Rains is a major reason wrt ice cream sales specially

Moldtek suffered the most coz of these factors.

Pharma segment is where IBM can be good – Lets see

Festive season – they make Sweet box too – Something to check is fmcg segment

INOX Wind (08-12-2023)

Govt. has come out with a fresh policy for repowering old wind mills below 2MW capacity. The compensation under the scheme is detailed Page 8 onwards. They want to target 25GW worth of old wind mills under this policy. If even 50% of the capacity comes forward for repowering, that can be a great further demand driver for Wind OEMs.

D4mHqmI5TydoiPXborrTnwJQ07jXbjaTKixr5Fe4iIayf3cMivzU5.pdf (854.7 KB)

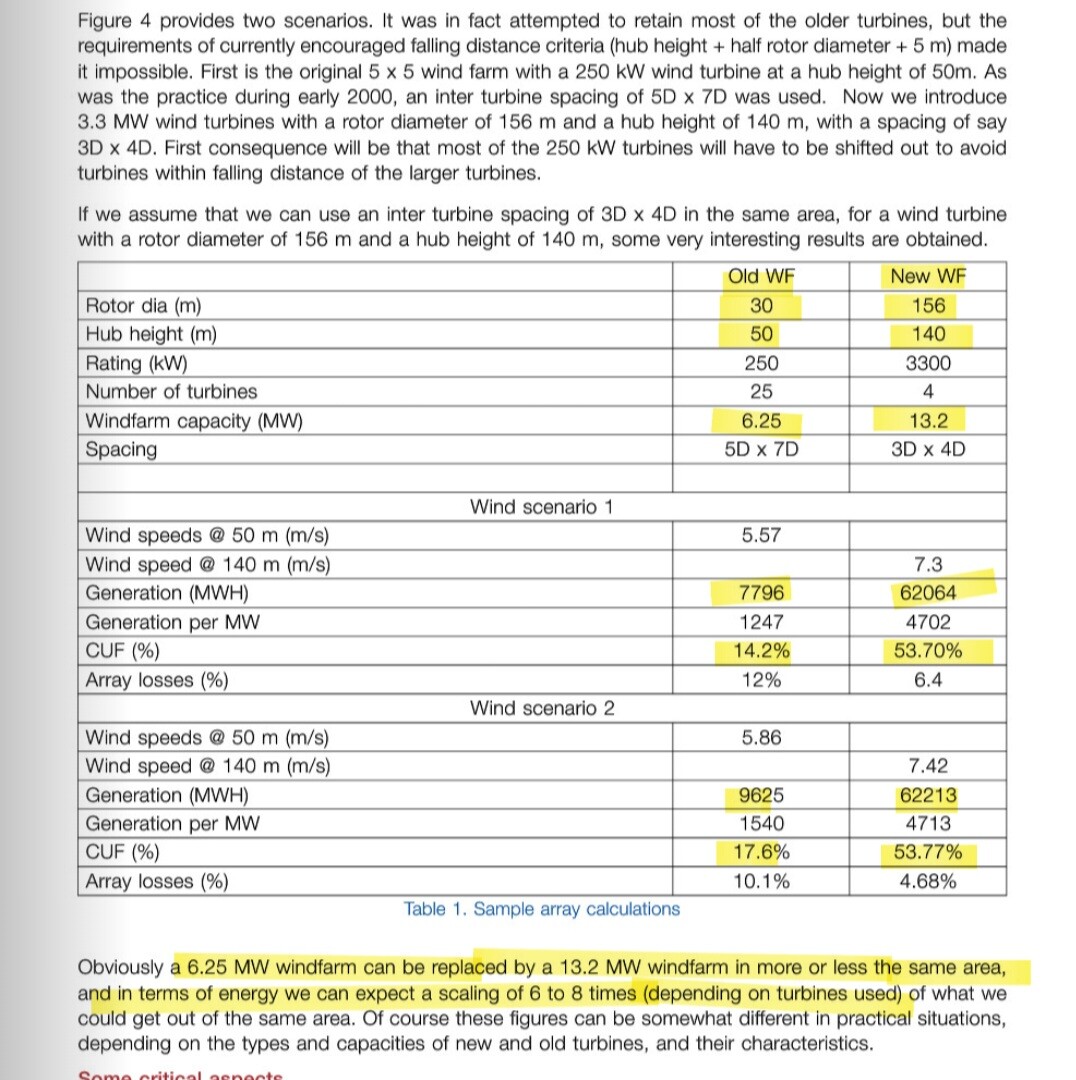

INOX Wind (08-12-2023)

Wind power

Diff between technology of old turbine of early 2000 & New 3.3 MW turbine of 2023.

Double MW capacity & upto 800% energy can be generated in the same area.

Source: Windpro

BCL Industries – Ethanol Pick (Capacity 3.5x in Next 2 Yrs) (08-12-2023)

Q3&Q4 numbers will stable with all 600 KLPD capacity on stream, I am expecting distillery revenues ~400 cr from the existing 320Cr quarterly run rate.

FY24 EPS could be ~5/- and FY25 could be ~8/-. Price still at ~10 PE of FY25 Earnings.