Posts tagged Value Pickr

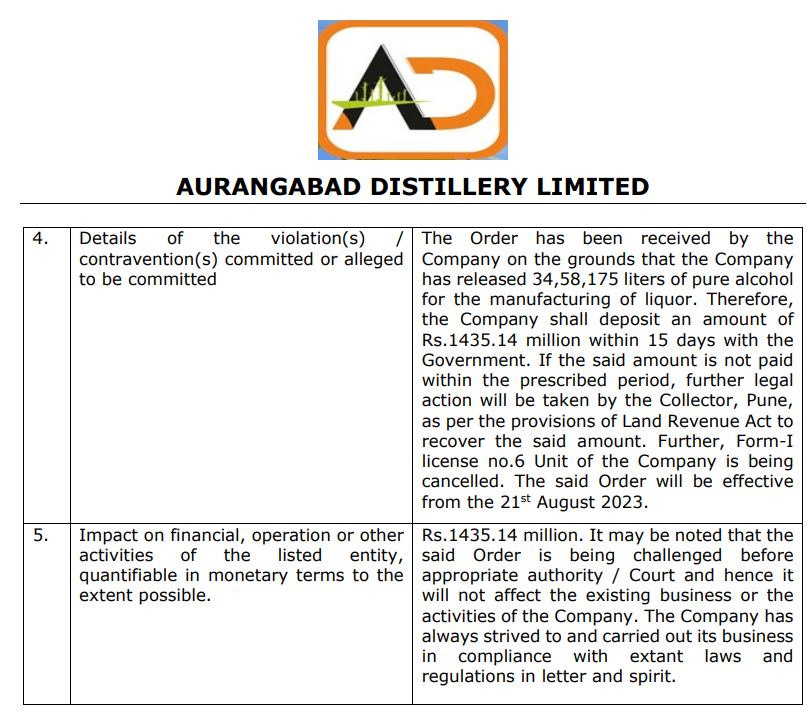

Aurangabad Distillery Ltd (07-12-2023)

AURDIS_16082023210757_ADLINTIMATION.pdf (nseindia.com)

Although the Company has obtained a stay on the order, the Liability can’t be ruled out. Also a big jump in Other Current Assets showcases the upfront amount required to pay to get stay on the order.

Do note that many parameters are in favour of the company and results have improved which is indicated in rise in the price of the share.

And also, this was mentioned somewhere. I do not remember the official source now but found it on twitter.

Disc: Invested.

KPI Green- Turning Sunshine Into Cashflows (07-12-2023)

Hi. Where do you got the information about the kpark? Can you rthe valuation report if it’s there?

The harsh portfolio! (07-12-2023)

Every investor has their own pecularity and style, they are free to do what they feel is right.

You can read more below.

Praveen’s Information Attic (Obervations, Lessons, Thoughts) (07-12-2023)

Hello Folks

I’ve posted about Averaging up in MCX on 19th Nov. I’m still going to ride the trend.

Today I’d like to make a comparison between two Cos in both technicals (mostly but some Funda as well)

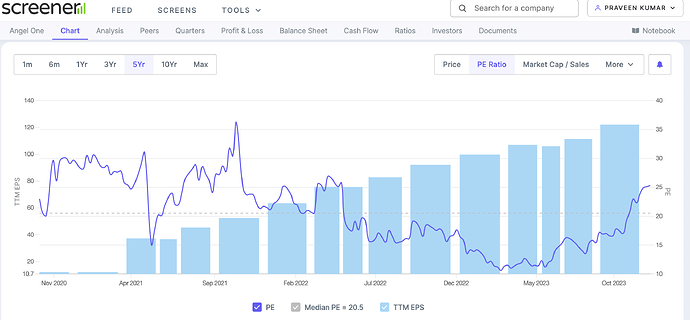

Let’s look at charts of Angel One and MCX over past few days

Angel One:

- Over Last 8 days, I see there are 2 candles (marked with arrows) where I could see 2 candles with wick on top, which indicates that the price rise did not sustain

- Even though yesterday there was big green candle (on Monthly business update release), but there’s no follow up and today the stock gave away some of the returns

- By looking at the Volumes, we can see that the Green candles have higher volumes, which is a positive sign technically

- On Funda side, the co. is trading at PE of ~25.3. The stock made a peak in Apr 2022 at 26.9 PE. Which means that the co is close to peak valuation it achieved last year

MCX:

- As per my interpretation, the stock is still not seeing much pressure in continuing the uptrend even though the momentum is not as much as it was 2 months ago

- On Funda side, the stock is trading at 40x P/E FY25 estiamted earning (assuming 424 cr PAT for FY25). Though it looks over valued, but considering that it’s a monopoly business it may not be the peak (not undervalued either). Also CAMS and CDSL trade at >45x, 62x TTM P/E and have infirior growth compared to MCX

So, from my Funda view Angel one is close to it’s peak and no opinion on MCX funda wise.

Coming to Technical view Both are making new highs. But Angel one shows signs of exhaustion but not MCX.

MCX is clearly stronger on chart compared to Angel One. My view is that MCX is stronger and should outperform over next few months.

Why and What I’m doing:

- I’m writing down my thoughts in Technofunda and would assess in future how my views played out. This would give me confidence and also help learn few things

- SInce I’m a beginner in TechnoFunda, comparing 2 stocks from my tracking universe (also in PF) is a better exercise than comparing with TechnoFunda picks of other people.

Please feel free to share views on how you’d interpret these charts and earnings. Let’s learn from each other

Disc: No reco to buy or sell. Currently holding both Angel One and MCX

Axita Cotton – is it a Hidden Gem? (07-12-2023)

What could be the next resistance of Axita Cotton? Any idea?

Cineline India – Picture abhi baaki hai (07-12-2023)

(post deleted by author)

Whirlpool of India (07-12-2023)

One of the issues Whirlpool India has is that group allows them to only make products for India ? With dilution , and depending on who is the buyer offcourse we can hope that WIL will have greater freedom to supply as contract partner to more locations outside as well as have more choices to manage costs in business decisions. Who ever is acquiring parent stake is not going to sit …they will excert pressure to relaease value and push them to deliver more results

Rural Elect Corp (07-12-2023)

I would not necessarily agree with the fact that IREDA should get a premium.

The real opportunity is in financing the utility scale projects for a longer term (otherwise, it gets refinanced through foreign borrowing) – therefore, cost of the funds is crucial in this business. As far as financing the RE sector is concerned, PFC/REC have been in the business for long and understand its nuances well. Infact, financing state thermal sector is better as they are cost plus and don’t have re-financing risk – these contracts are also long term and have implicit or explicit state guarantee (which makes them virtually an arbitrage business).

Have been in the Power Sector for a long period and can say they have good people assessing the projects…

Disclosure: Have been invested in both PFC/REC for 4-5 yrs