Word of caution with real estate market, IT jobs are getting cut every single day especially senior category types and freshers arent getting placed so it is important to consider RE growth is tied mostly with IT progress as the highest salary earners with disposable income is in IT

Posts tagged Value Pickr

Som Distilleries and Breweries (04-12-2023)

Got approval for Karnataka.

Waiting for clarity on IT raid, and trend should resume.

Finkaro Unfloding The Unheard Companies with Lot’s of Potential (04-12-2023)

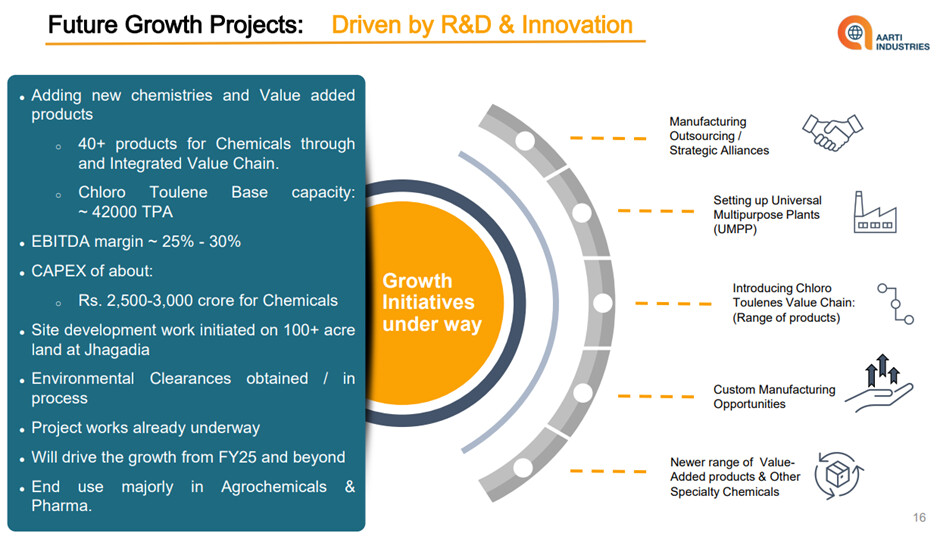

Next Business No 5 – Aarti Industries

“Sleeping Giant ,Will Come out with Flying Colours In FY26”

Company Corrected 50% Peak in last 2 years and now started forming Base

Largest producer of Nitro-Chlorobenzene, Benzene and Lowest cost producer of benzene in the world and have diverse portfolio of basic chemicals, agrochemicals, speciality chemicals and intermediates, which are extensively used in the manufacture of pharmaceuticals, agri-products, polymers, additives, pigments and dyes.

Multiple Long-Term Contract during FY17-FY19 Mfg Outsourcing, Product development and these contracts are under ramp up and can add 1000 Cr Sales and all contract are at less utilisation level

Agro chemical division business facing downturn nearly 30% Down overall

Benzene Price Volatility leads to inventory losses which is likely to cool off now.

Capex Guidelines Rs 3000 Cr for next 2 Years 50% for existing products and rest for the new product.

Chlorotoluene in Jaghadia India with Integrated Operation chain and will have 20% of the Global Capacity and whatever capacity they have built will be at 70%-90% Capacity Utilisation level by FY24 End.

Company Business into B2B and having Shallow Cyclical in nature leads to ups and down in the operating margin and overall growth in every 2-3 Years

Thesis

· Company has Given Guidance Earnings to 3X By FY27 on FY21 As Benchmark based on above expansion and product mix with higher value-added products

· Company have been maintaining CFO/EBITDA Above 75% despite B2B business Model

· Company has Big Marquie Clients recognised Globally

· Company has Strong management with Technical Know How >30 Years

· Company will be able to take benefit of operating Leverage in few years

Anti-Thesis

· From the current Outlook company seems to sleep more at least for next 1 Year

· Company debt will mount and Deprecation too may lead to poor earnings for next 1year Minimum

· How company able to pay such debt to be Noticed

· How Orderbook of the Company at Current stage and going forward

· Over Capacity and if China starts dumping company may suffer

Dis: No Buy/Sell Rico*

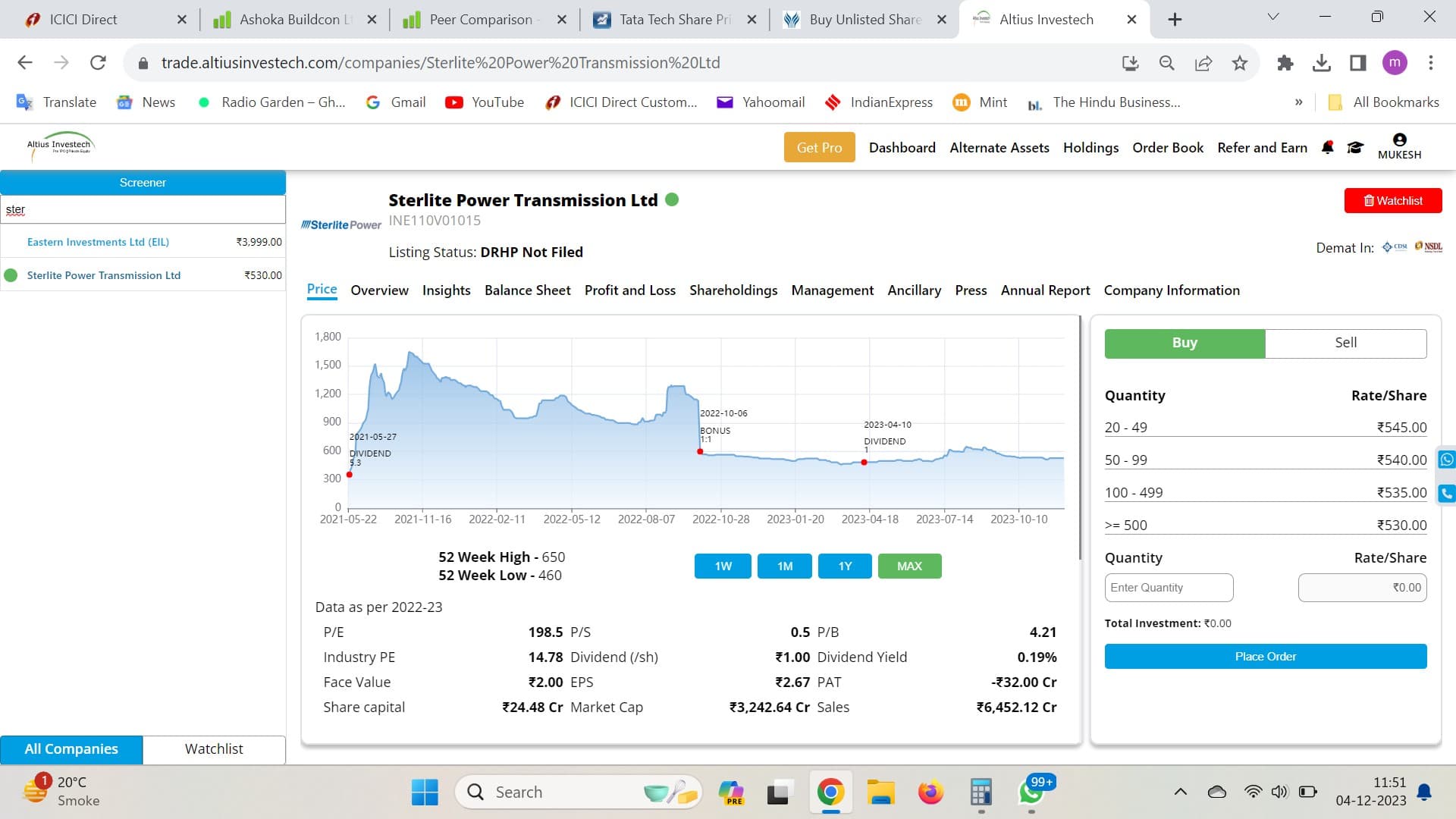

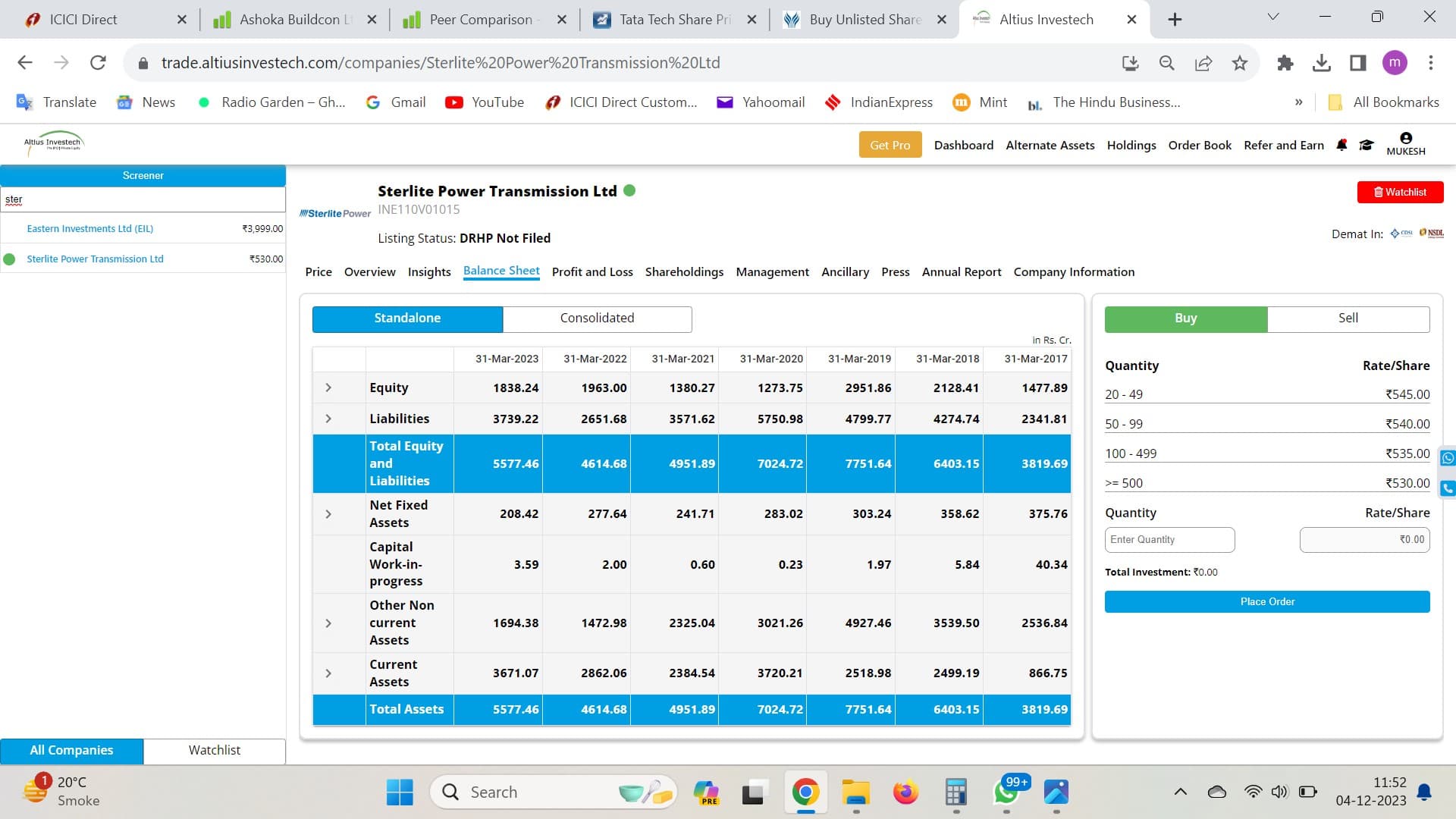

Buy Unlisted Shares (04-12-2023)

Thanks, I went through the balance sheet given here and PAT seems aligned with the news articles.

However, market cap in all other places is 6k crore plus.

Seems overvalued definitely on grey market.

Ujjivan Financial – Small Finance Bank (04-12-2023)

I feel it is more procedural and matter of few more weeks now ( Mgmt wanted to complete it before end of Q3 ) . Even if we account for another three months and make it end of Q4 , a 20% discount at current valuations looks attractive .

I feel that Ujjivan Bank itself would be a strong buy with yesterday’s election results . Considering it has one of the largest MFI books in Small Finance banks , unless we see signs of stress in portfolio . Considering their Provisioning levels , they seems to have create sufficient buffers for any stresses .

CreditAccess Grameen: Traditional MFI model, efficiently operating at scale (04-12-2023)

Recent rating upgrade by CRISIL to AA-/Stable.

This could reduce their cost of capital by few basis points.

NMDC Steel ( NSL ) – A Unique Demerger Opportunity (04-12-2023)

Wasn’t it Amit Shah who promised people of Chattisgarh that NMDC Steel Nagarnar plant will not be privatised?

I really hope this is one of those promises that are only meant for election time.

Rural Elect Corp (04-12-2023)

Is REC heading to rerating of PE?

Historically REC has majorly traded between an PE of 3 to 5

It has historically touched PE of 9.5 only once in 2014.

However after IREDA IPO it seems Power Finance companies will see an incremented PE. On higher end of IPO price (Rs. 32) IREDA seemed expensive at PE of 8.45 (REC was trading at PE of 7.1 at same time) and IREDA looked expensive.

With IREDA looking to settle between price of 60 to 65, it will be trading at PE of 15 to 17.

REC is into similar business as IREDA (Margins in renewable financing would not be too different from a mix of Non Renewable, Renewable & Infra project funding). Currently REC is trading at PE of 8.1 as of date, there cannot be a 100% difference in PE for 2 PSU’s in similar business. In short to Mid term, there can only be 2 scenarios playing up:

- REC will chase PE of IREDA and may end up trading anywhere between PE of 10 to 14 and IREDA settling to a PE of 14-16

- IREDA to correct to levels of 45 to have a PE of 10 and REC staying at a PE of 7.5 to 8.

What do others tracking Power financing sector think of?

Disclosure: Holding REC from levels of ~80.

Screener.in: The destination for Intelligent Screening & Reporting in India (04-12-2023)

Can we please add a screener to filter companies if it does concalls or not? helps to avoid micro caps that have very little public information available.

Buy Unlisted Shares (04-12-2023)

Happy to be of help. Of course, difficult to say which data is correct.