Force Urbania – Mrs. Hardi Shah, Ahmedabad | Customer Testimonial

Posts tagged Value Pickr

Goldiam International : A rare shareholder friendly and debt free Jewelry company (03-12-2023)

I found this in Google searching name of Rashesh Manhar Bhansali who is currently selling the share.

Is it related to the company promoter?

The harsh portfolio! (03-12-2023)

Coal india , Power Grid , is into infra or not?

The harsh portfolio! (03-12-2023)

The event was great (Was present there physically.) One this which i wasn’t able to digest was on why they don’t have investment in the Infrastructure … When there are good companies like L&T…!

Can you please share your thoughts on this @harsh.beria93

Advani hotels and Resort (03-12-2023)

A few observations on a quick look at the company

- The average revenue per Occupied room per night is constantly increasing–only a few listed companies could charge this level to their customers.

- Occupancy is at a historic high. Practically going up from this level will be a challenge.

- EBITDA margin in FY 23 is bit high if I compare to with historic numbers. This is the case with all the players in the industry.

- When I compare it with Sinclairs Hotel relative valuation looks bit attractive

Few questions

- I did not see any expansion from the company – any management plan to expand the number of keys they have?

- What do you think the future growth will come from?

NMDC Steel ( NSL ) – A Unique Demerger Opportunity (03-12-2023)

BJP’s win in chattisgarh extremely positive for divestment prospects of the company.

Biocon – The ultimate biosimilars play! (03-12-2023)

Well, Most of the investors fell prey to the rosy narratives of being a first mover in a niche area with a visionary approach.

The problem is that not much deep dive was attempted on part of individual investors to evaluate the actual commercial/biz performance of those niche products commercially.

Even if we keep debt for acquistion apart giving mgmt a benefit of doubt or the grace period to excel in knitting a niche biz, the actual products for which all these concessions r being given needs an evaluation.

The problem with biocon is that the biosimilar products are niche in india and they r 1st mover but when it comes to the sales area i.e. US, they r not so niche and they have to compete with many established players with fat wallets.

The outcome of all this is their r 8~10 players competing for the mkt share.

The result is huge price erosion upto 50% to grab mkt share.

But the irony with Biocon is that even if they r the cheapest but still they are not in top in mkt share

So, something is really not working on the commercial realization of products the way it ought to be .

Result of all this not syncs well for long term margins and revenue front.

Mkt somehow works on actual profits at the end then the narratives.

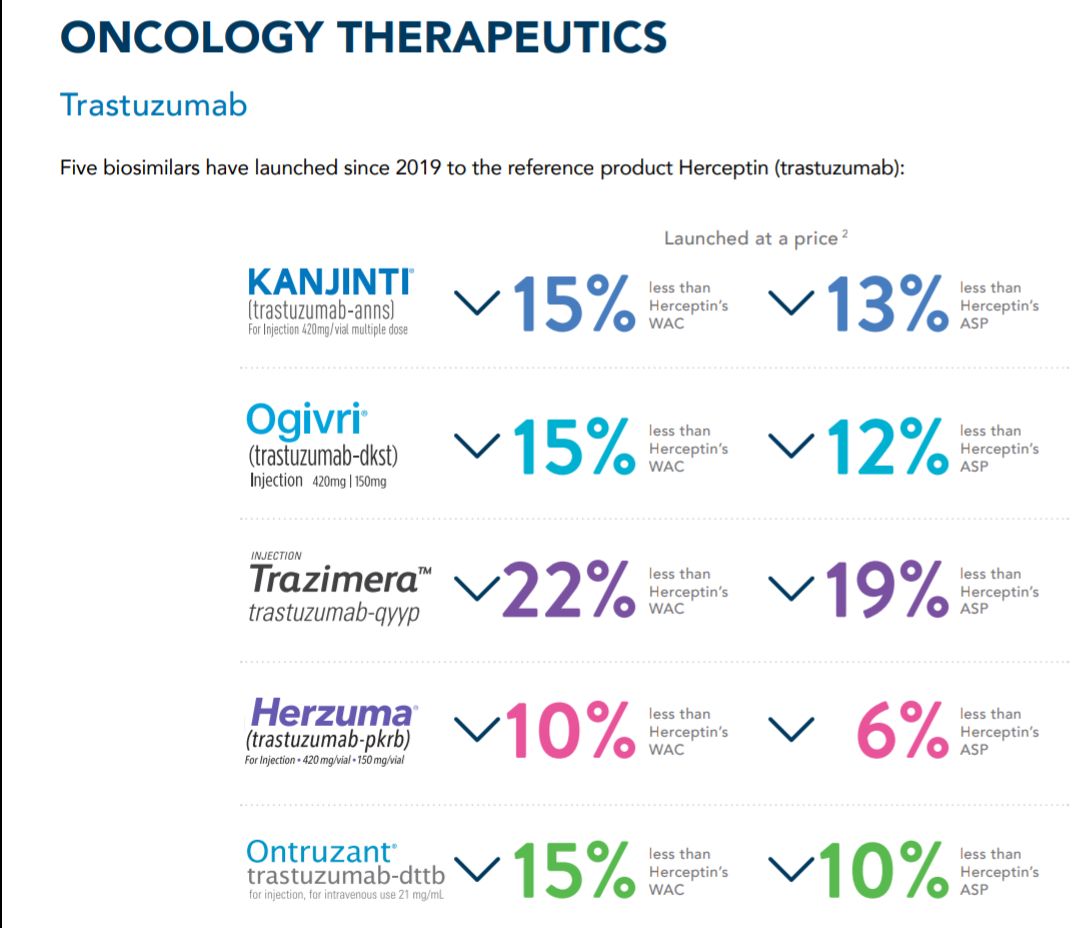

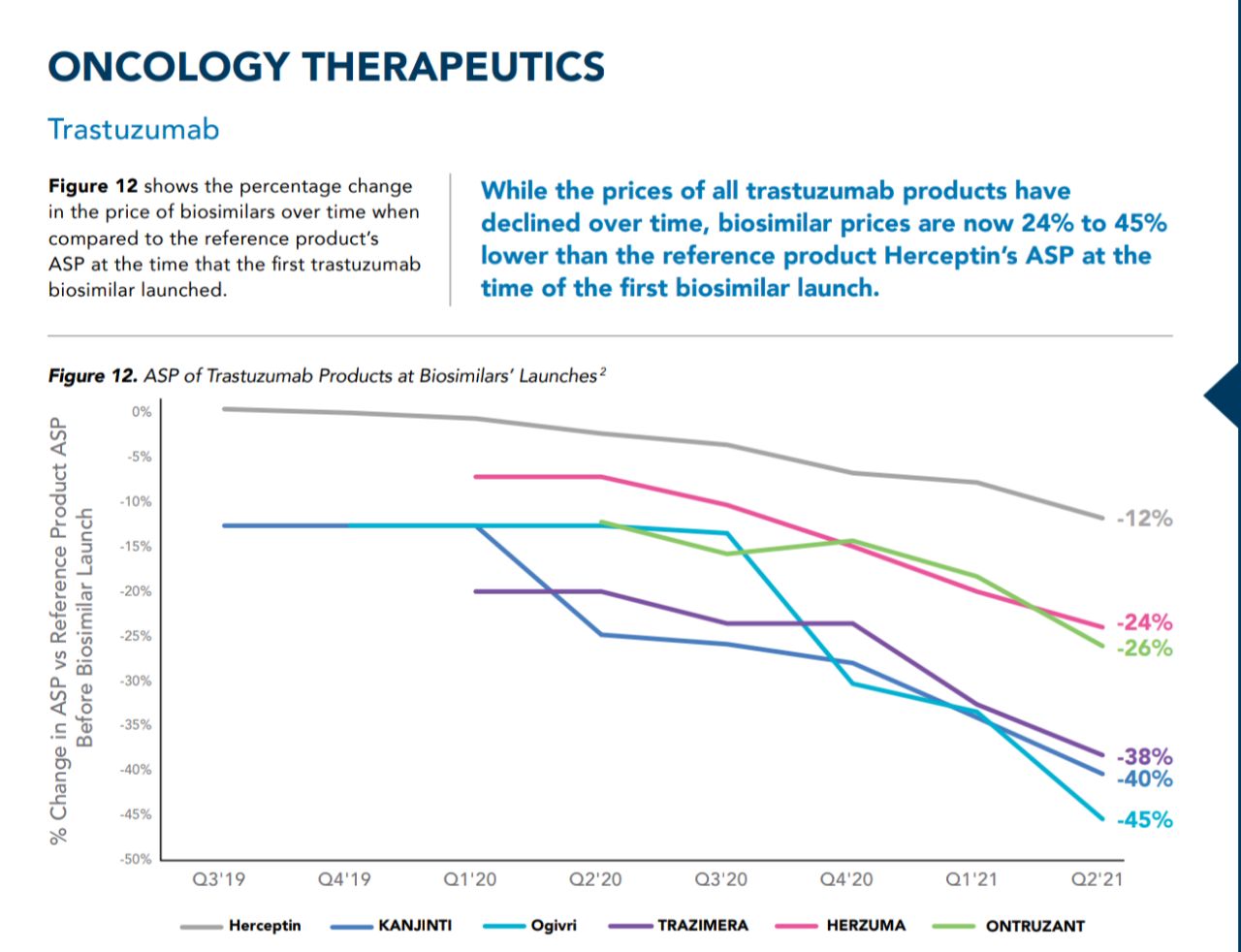

Ogivri is biocon

Ogivari eroded 45% in 2 years

It got 9% mkt share in 2 years

The nearest cheap competitor got 44% mkt share in 2 years

Eroded 40% in 2 years

Biocon was 1st to get approval

2 years down the line it eroded 45% with 9% mkt share

Ye sirf ek biosimilar ka example hai.

This is siruation when only 5 players r there

Imagine when 10~15 player will be there.

After 2~4 years

How much we will erode ?

70%

How much mkt share we expect ?

20%

-70% * 20% = opportunity size ?

Eco Recycling Limited (Ecoreco (03-12-2023)

assets trunover is .5 and ROE is single digit .

top line double digit so .My points is can this company can gave EPS GROWTH above 15-20% next 5-6 years.can this company sustain with lwo ROE ? plz anyone

Buy Unlisted Shares (03-12-2023)

Appears interesting.