Carysil up more then 50% since i worte.

https://x.com/Alazyinvestor13/status/1653131508683767808?s=20

Carysil up more then 50% since i worte.

https://x.com/Alazyinvestor13/status/1653131508683767808?s=20

Do you have any data on the industry growth rates?

Do you have any data on the industry growth rates?

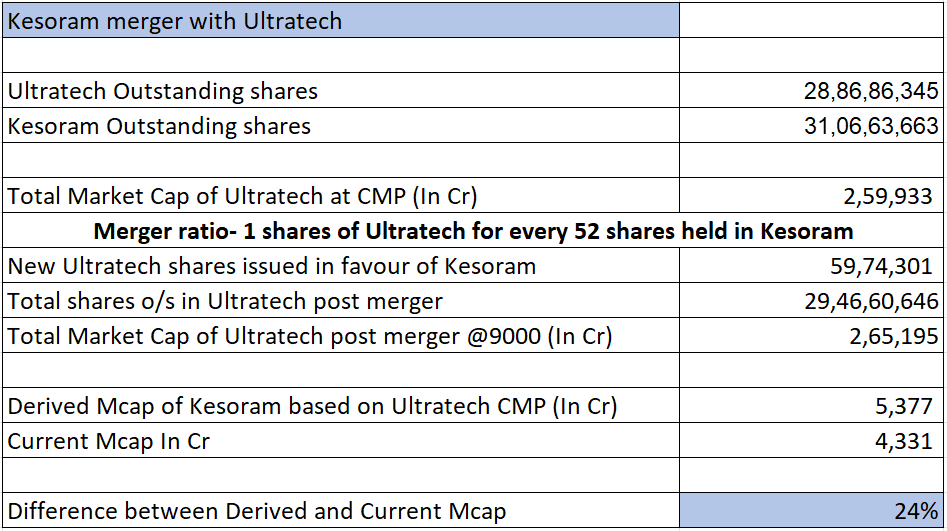

Kesoram has some non-cement business also. What value you have given to that?

Kesoram has some non-cement business also. What value you have given to that?

Thanks! Will try, test and then expand. As of now, only want to experiment for 5-10% of my overall portfolio. Once I get confidence with my experiments, I will then gradually increase. Let’s see.

Just evaluating the trades post monthly close. Some of the new trades from last 2 months are doing quite well.

Taal – Big breakout last month. Still considerably undervalued compared to other Engineering services firms. Taal Tech has respectable 40L rev/emp and exceptional margins. I feel compared to Tata Tech listed valuation (its rev/emp is 45L and a margin of 20%), this still offers great margin of safety. The hiring in recent months has been quite strong (EPFO) and is infact probably depressing the margins (should hopefully get back above 30% when it normalises). Compared to IT services businesses ER&D and Engineering services clearly is showing strong uptick in hiring and growth and should sustain due to the high wage inflation in Europe and US.

Ceinsys – The business has been winning and renewing orders in its geospatial and IoT business for Jal Jeevan and State water sanitation missions (SWSM). Ceinsys probably has a rev/emp of around 25L while AllyGrow likely tops 50L (And likely does 30% margins). Here again the engineering services division should grow strongly and the geospatial division is seeing strong revival with govt. orders in Jal Jeevan (both have strong tailwinds). Valuation remains cheap even post the strong breakout and consolidation.

Sharda Motors – Pretty strong breakout on the monthly as anticipated. Remain cheap still and hopefully should sustain the run

MOTILALOFS – Good breakout from the congestion zone around 1000-1100. Did a re-test of 1100 odd levels during the month and the shakeout should help contnuation of the trend. Still remains cheap

Holding most of the rest (PML, Goodluck, Mazda) as is and reducing Shilchar. Took a few new small bets in Wockpharma, Eimco Elecon and Electrocast to delve deeper. First two especially appear quite promising. Wockpharma has been restructuring its business (it has no choice) and is betting big on WCK5222. Numbers may not come until FY26 but if they manage to raise money for phase 3 which appears very promising, can run up in anticipation. Its perhaps a good turnaround bet. Eimco Elecon, since govt is planning to increase underground mining by 3x and at the same time also planning to cut down on imports of equipment. Eimco is also doing well in diversifying its business away from Coal mines (mining of metals) and also into construction (piling rigs). These two appear the most promising in terms of triggers and valuations but over the medium/long term.

The GDP growth (13%+) in manufacturing, infra and construction clearly shows where the fish is – most of the bets that have worked well this year have also been in these sectors. This tailwind should hopefully continue. Engineering services too clearly has a strong tailwind due to wage inflation in the west and could be a trend that could sustain for sometime

Disc: Invested in the names mentioned and not qualified to advise

It is finally happening! Ultratech acquiring Kesoram’s cement division in the form of 1:52 Ultratech : Kesoram 100% equity share swap ratio. Valuing its clinker backed cement capacity of 8.5 MT at $87/MT and total cement capacity of 10.75 MT at $70/MT. Another case to justify that M&A in cement sector happens at least closer to its replacement value, despite the existing problems.

I recommend you go with Vishwanath’s approach. His approach by far makes sense from risk vs return perspective.

Thanks Praveen. Good points. Actually I want to select only top 10 stocks (instead of top 20 in Vishwanath case) based on return and volatility criteria and for a stock to exit, it has to fall outside top 20 (so a gap of 10 stocks instead 5 in case of Vishwanath). For the universe, I agree that top smallcap top 250 makes more sense.