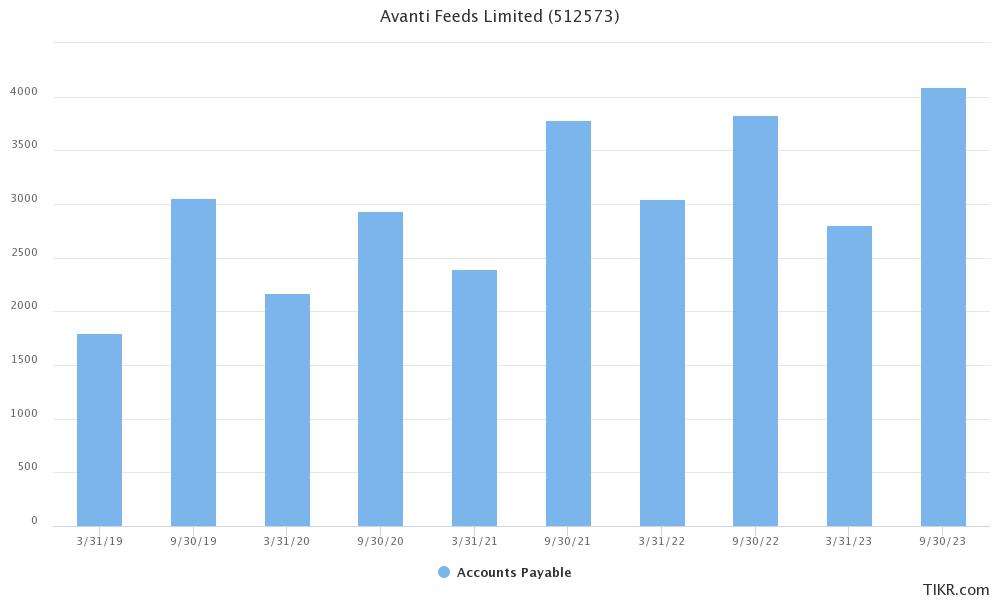

This is a normal H1 phenomena, please look at payables at end of each H1 during past few years, this year its not abnormal.

This is a normal H1 phenomena, please look at payables at end of each H1 during past few years, this year its not abnormal.

Demerger of wealth management .very unlikely. Promoter family is not going to dilute their holding or or pledge their holding and they dont need to do this ” unlock ” as you mentioned . They will just take dividend as malai … if you dont mind this ” desi ” phrase … They are not overly concerned about valuation of MOSL …

Total assets and total liabilities are same because very financial transacton needs to be balanced. Suppose you had Rs 20000 as bank balance. Ideally your bank statement should show Rs 20000 as liability to you. and you will show Rs 20000 as asset in your books … Hope this is clear now …

Malolan

This logic implies that, when Indian GDP Growth rate was almost 8% to 9% during 2003-2013, Nominal GDP rate was about 16% to 18%.

Probably that’s the reason why SENSEX CAGR was about 16% during that period.

Probably it is good idea to understand the lessons learnt at that time and use those in next 20 years.

when will you enter gain? And starting from scratch, how will you approach the process?

Good session by Siddharth Bhaiya on finding mulibaggers. Some good case studies in the last 30 mins

Goodbye Charlie Munger.

Your influence has been immense.

Two quotes, which I hold dear; especially considering my many stupidities in investing and more when I migrated to trading for a period;

—-

If you’re not failing, you’re not improving.

—-

“Of course, there’s going to be some failure in making the correct decisions. Nobody bats a thousand,” Munger said. “I think it’s important to review your past stupidities so you are less likely to repeat them, but I’m not gnashing my teeth over it or suffering or enduring it.”

“I think the tragedy in life is to be so timid that you don’t play hard enough so you have some reverses,”.

—-

Goodbye Mr Charlie.

You will be an influence to me all my life.

The Board of Directors of PCBL Limited (“Company”), has at the Meeting held on 29 November 2023, in-principleapproved the term sheet for entering into a joint venture with Kinaltek Pty limited (“Kinaltek”). The Company shallown 51% of the shareholding in the joint venture company (“JV Company”), and shall be infusing a consideration ofUSD 16,000,000 in the JV Company and a commitment to infuse funds up to USD 28,000,000 in stages in the JVCompany, for setting up a manufacturing facility (“Proposed Transaction”);

The Company has entered into a term sheet to form a JVCompany with Kinaltek (an Australian company, which has developed nano silicon technology for battery application).The Company shall own 51% shareholding in the JV Company which will have the intellectual property and know-how of

products for battery application and a pilot plant for the same.

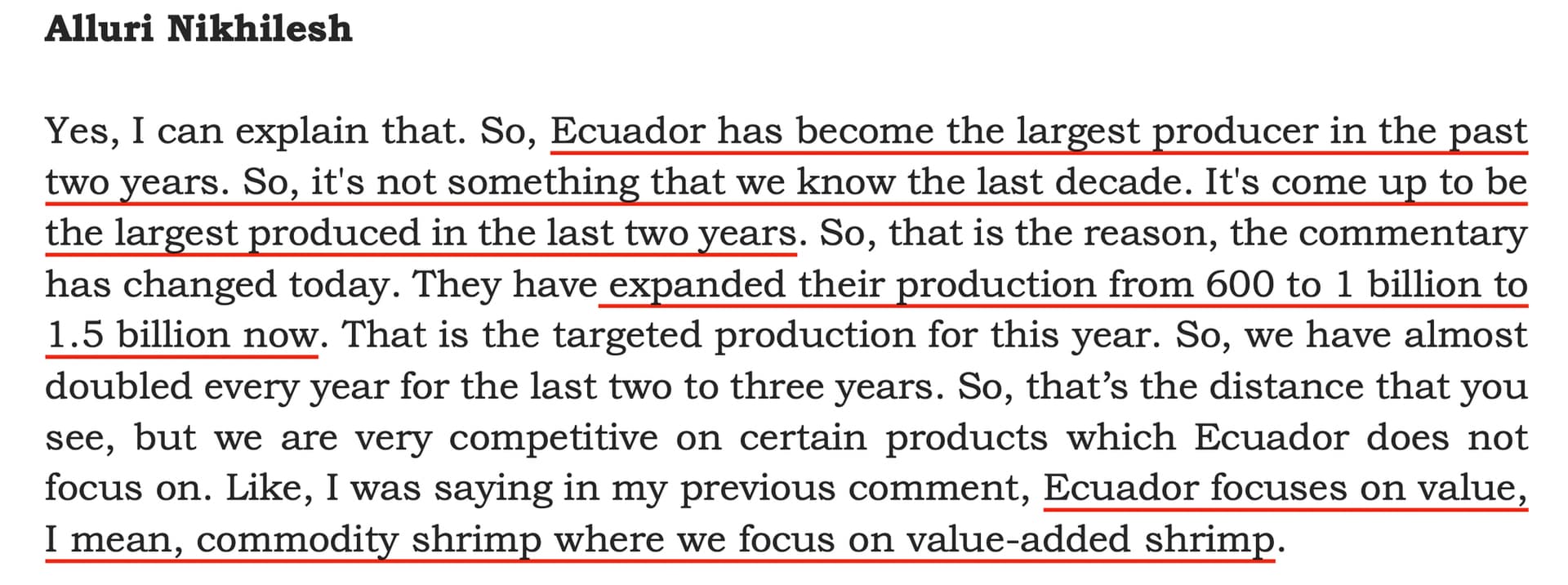

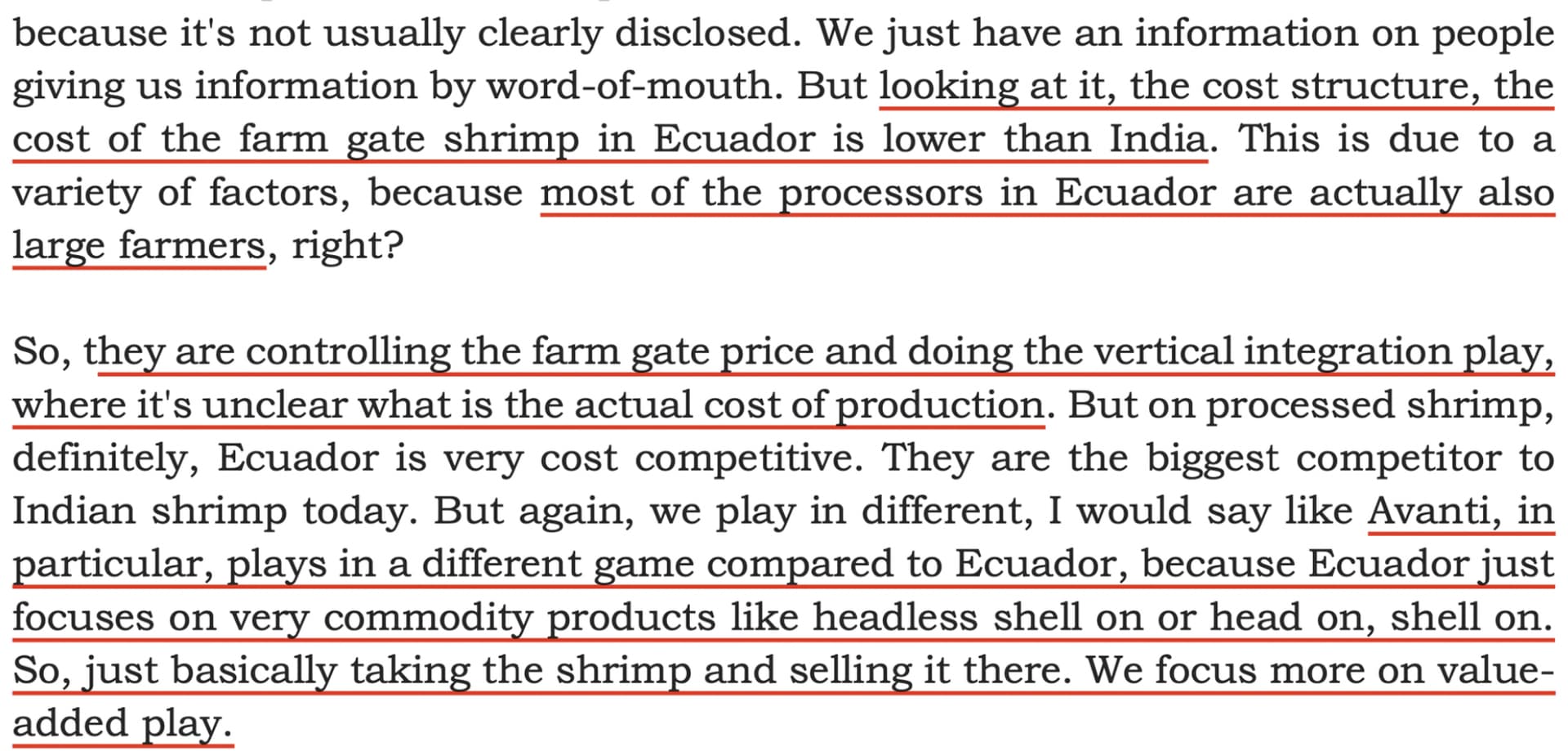

Cost Structure Comparison :

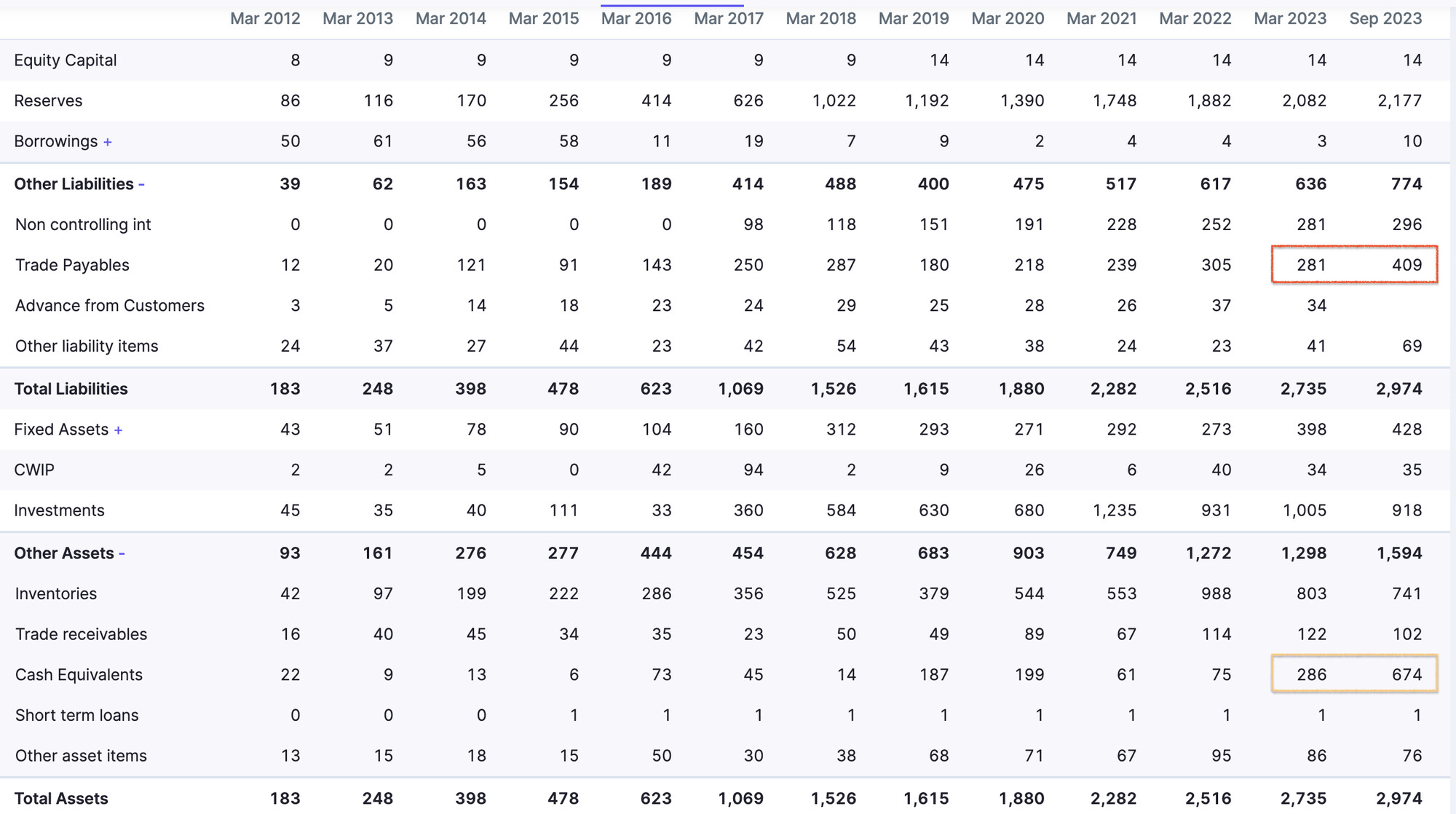

BALANCE SHEET

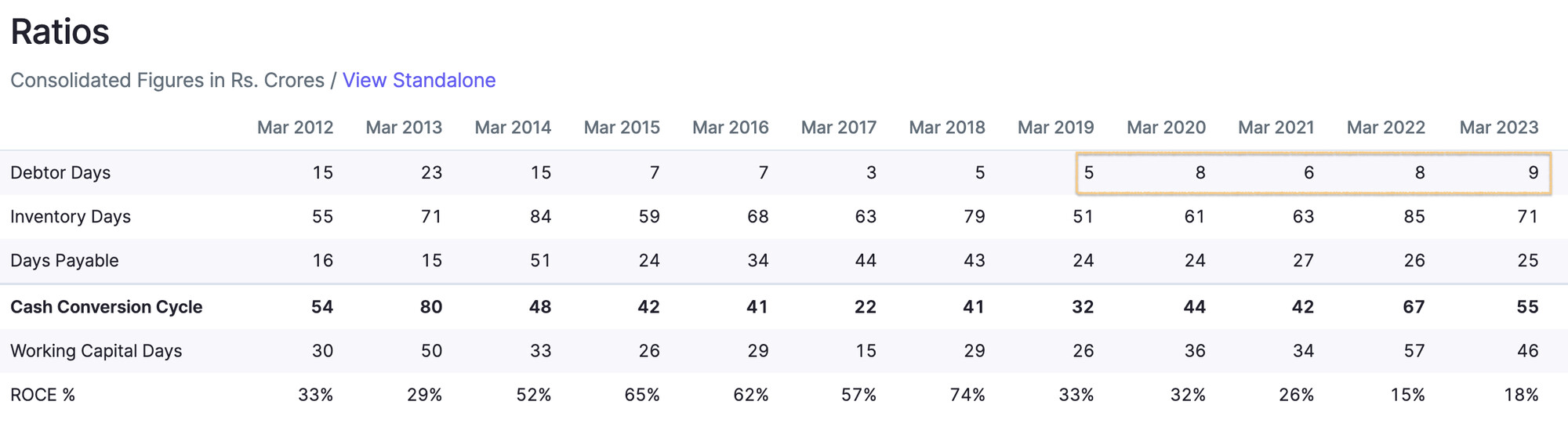

Why have the trade payables increased so much, it is a liability after all so need to be looked at because due to this the profits would have an upward bias

They are holding extra cash than what they used to

Answer : Received from con-call

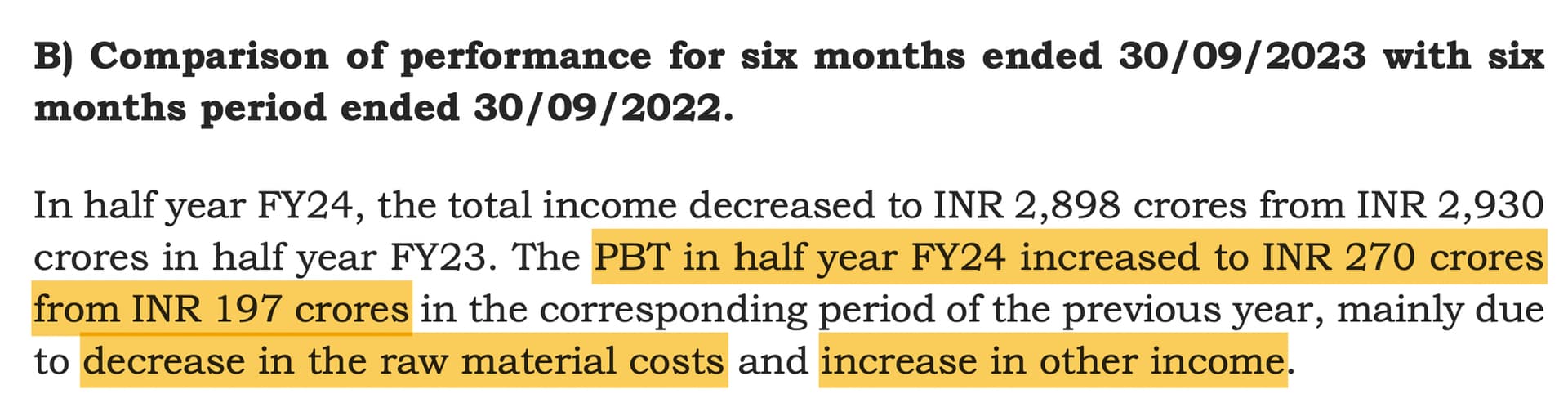

Ratio Analysis

************************************Additional Benefits :************************************

With an intermediate support of 375( No reco, do your own due diligence)

I have summarised the point in this thread too – https://twitter.com/Lakshayy_99/status/1728689844136943949.

Do let me know your thoughts, and correct me if there’s any thing incorrect. Hope you gained some insight from this ![]()

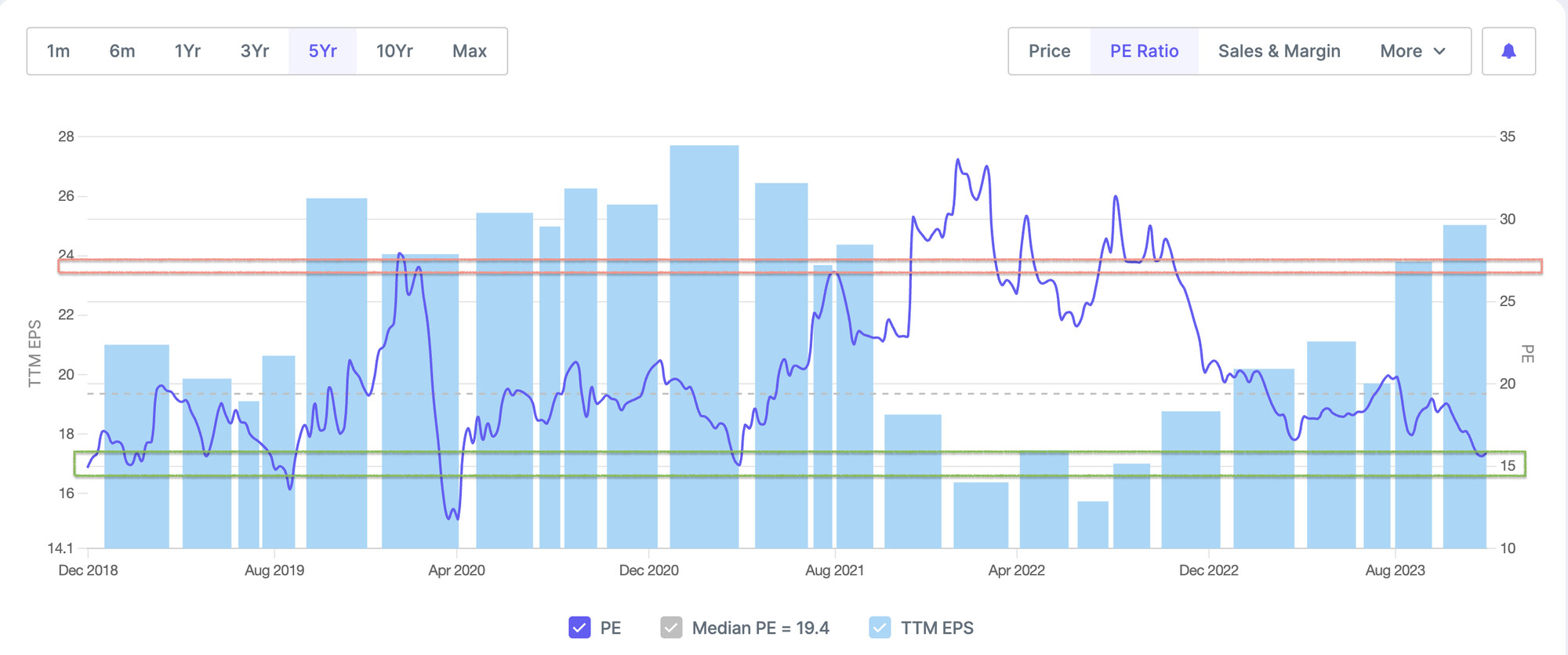

Bill Ackman asks Warren Buffett a question about stock buybacks when valuations are high

An interesting question asked to Warren Buffett about Coca Cola share buyback at 40 PE.

Though I am not sure that TCS doing a buy back at that price is right or wrong.

But this is their 5th buy back since 2017, it is a really cash rich company, pays handsome dividends, 13% Stock Price CAGR for 10 years along with 3% dividend yield.

The entire IT sector is going through challenging times but then that’s nothing new, every sector goes through turmoil and I feel it is such an amazing company to hold on to.