Hi, I haven’t included MF as yet into my portfolio. Will do that maybe in sometime. However I track my MF portfolio separately on Zerodha Coin app. For dividends I am not sure as I started using this since last 1 or 2 months. Will update in case I get or otherwise.

Posts tagged Value Pickr

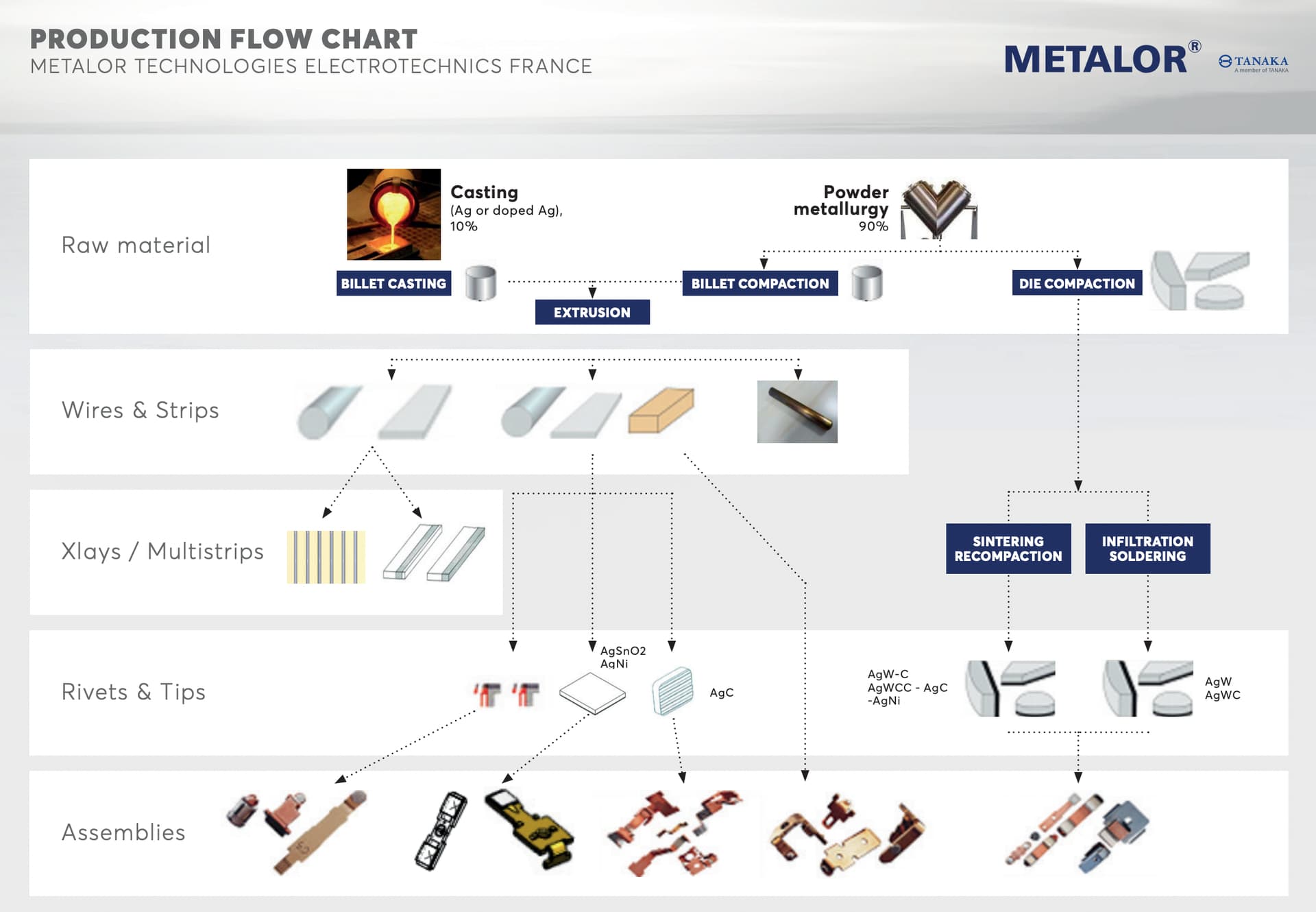

Shivalik Bimetal Controls Stock Story (24-11-2023)

Shivalik Bimetal has signed the MoU with Metalor Technologies International SA (Swiss Corporation) for setting up a Joint Venture in India to manufacture and sale of electrical contacts. Source here.

The Q2Fy24 media release has brief mention of this JV. It says –

Towards a significant strategic move, Shivalik Bimetal Controls Ltd. has embarked on the process of establishing an MoU to assess the feasibility of a joint venture with Metalor, a Tanaka group company, which is a world leader in the field of Precious Metals. Metalor, a renowned Swiss company, is celebrated for its expertise in silver contacts and state-of-the-art silver melting facilities in several locations around the world. Chairman of SBCL, Mr. S.S. Sandhu, shared, “We look forward to exploring a joint strategic partnership with Metalor in India. By conducting a feasibility study, we will assess the value addition this partnership can bring to manufacture and assemble silver contacts. This initiative affirms our commitment to pursue sustainable growth that can open doors to Metalor’s extensive global network. We hope to analyse how Shivalik’s silver contacts segment can be positioned for substantial volume growth through this venture, as we anticipate achieving greater milestones in this segment.”

(Source: https://metalor.com/wp-content/uploads/2020/07/Electrotechnics_Production_flow_Chart.pdf)

One of the most important roles of a management team and board of directors is to reinvest capital at the high rates of return. Is this JV a step in right direction (seems so)? Time will tell.

CAGR expectation and experience (24-11-2023)

I have started using Value Research services recently.

Here are the portfolio returns (CAGR % pa) for my holding since last 11 years:

- 11 Years return (21% return on per annum basis since last 11 years)

- 5 years return (24.6% return on per annum basis since last 5 years)

- 3 year return (26% return on per annum basis since last 3 years)

Screener.in: The destination for Intelligent Screening & Reporting in India (24-11-2023)

I am planning to use screener premium. Does it offer any discount/offer any time of the year?

Interesting risk/return of Spicejet (24-11-2023)

Big question whether Spicejet is turning the corner…It is rapidly turning its lessors debt into equity including a $100 million Carlyle transaction where the lessor converted at a price of 48 when the share price was in the twenties .Profit is obviously increasing now and will continue as Indian popularity for air travel continues…

However will Spicejet be able to keep costs down enough to maintain profitability ?

IIFL Finance (erstwhile IIFL Holdings) ~ Retail focused diversified NBFC (24-11-2023)

IIFL Finance ltd Q2 concall highlights –

Loan Book @ 73k vs 55.3k cr, up 32 pc

NII – 1001 vs 724 cr, up 38 pc

PPOP – 922 vs 654 cr, up 41 pc

Provisions – 252 vs 196 cr, up 30 pc

PAT – 475 vs 380 cr, up 25 pc

Gross NPAs @ 1.8 pc vs 2.4 pc

Net NPAs @ 1.0 vs 1.2 pc

Book Value / share @ 252 vs 215

RoE – 20.1 pc

RoA – 3.9 pc

Loan book break down –

Loans on company’s books – 44k vs 35.2k cr

Assigned assets – 18.4 k vs 15.4 k cr

Co-Lending – 10.5 k vs 4.7 k cr

Total – 73 k vs 55.3 k cr

Sector wise breakdown of loan book –

Home Loans – 24k vs 19.6k cr, up 22 pc

Gold Loans – 23.7k vs 17.8k cr, up 33 pc

LAP – 7.2k vs 5.9k cr, up 21 pc

Digital loans – 3.5k vs 1.99k cr, up 77 pc

MicroFin – 11.3k vs 6.7k cr, up 67 pc

5 yr CAGR of loans AUM growth @ 23 pc

5 yr PAT CAGR @ 28 pc

Avg loan rates –

Home Loans – 11 pc

Gold Loans – 18.5 pc

LAP – 18.6 pc

Digital laons – 22.4 pc ( primarily for MSME lending – unsecured loans )

MicroFin – 24.4 pc

AVG yeild- 17 pc

Avg cost of borrowing – 9 pc

Spread – 8 pc

Cost/Income @ 43 pc

Avg ticket size –

Home loans – 14 lakh

LAP – 7.7 lakh

Digital Loans – 0.7 lakh

Gold Loans – 0.75 lakh

Aim to reach AUM of 1 lakh cr by end of next FY

Company continues to remain cautious on unsecured lending / personal loans. Sounded skeptical of due diligence process followed by new gen Fintechs

Gold loan growth driven by company’s distribution strength

IIFL housing finance gets funding from National Housing Board at concessional rates – helps keep cost of funds under check

Company expects to maintain its NIMs at 7-7.5 pc or thereabouts

Management doesn’t see any credit demand slowdown if the economy remains robust – the way it is today

Avg life of Gold Loan portfolio is 90-120 days

Company believes, cost of borrowing has almost peaked in India. May move up-down by 10-15 bps, not beyond that

Company has slowed down its branch expansion spree. Should lead to lower Opex going fwd as more branches mature and their AUMs increase. Ex – IIFL’s gold loan branches have avg gold loan AUMs of 8 cr vs 22 cr for Mkt leader

Avg tenure of Digital loans varies from 6 months to 2 yrs. This is a high risk area. Hence the company is very aggressive in provisioning against Stage -3 assets wrt Digital loans. Despite that, returns are fairly attractive

LAP product in smaller towns etc has attractive rates. However, it also involves higher cost of origination like the cost of verifying the title, valuation of property etc

Q2 RoA @ 3.9 pc. Should be able to maintain the RoA range between 3.7-4.0

Credit cost range guidance given by the management @ 2 or thereabouts

Price war in Gold loans business witnessed in last FY is now abating. Hence the lending yields have gone back up

Co-Lending and Assigned books mainly consist of Gold, Housing loans and LAP

Current branch count at 4596 vs 3700 LY. As the new branches mature, operating leverage should kick in. On an avg, a branch breaks even in 18-24 months

Disc: Hold a tracking position, may add more, biased, not SEBI registered

Ranvir’s Portfolio (24-11-2023)

IIFL Finance ltd Q2 concall highlights –

Loan Book @ 73k vs 55.3k cr, up 32 pc

NII – 1001 vs 724 cr, up 38 pc

PPOP – 922 vs 654 cr, up 41 pc

Provisions – 252 vs 196 cr, up 30 pc

PAT – 475 vs 380 cr, up 25 pc

Gross NPAs @ 1.8 pc vs 2.4 pc

Net NPAs @ 1.0 vs 1.2 pc

Book Value / share @ 252 vs 215

RoE – 20.1 pc

RoA – 3.9 pc

Loan book break down –

Loans on company’s books – 44k vs 35.2k cr

Assigned assets – 18.4 k vs 15.4 k cr

Co-Lending – 10.5 k vs 4.7 k cr

Total – 73 k vs 55.3 k cr

Sector wise breakdown of loan book –

Home Loans – 24k vs 19.6k cr, up 22 pc

Gold Loans – 23.7k vs 17.8k cr, up 33 pc

LAP – 7.2k vs 5.9k cr, up 21 pc

Digital loans – 3.5k vs 1.99k cr, up 77 pc

MicroFin – 11.3k vs 6.7k cr, up 67 pc

5 yr CAGR of loans AUM growth @ 23 pc

5 yr PAT CAGR @ 28 pc

Avg loan rates –

Home Loans – 11 pc

Gold Loans – 18.5 pc

LAP – 18.6 pc

Digital laons – 22.4 pc ( primarily for MSME lending – unsecured loans )

MicroFin – 24.4 pc

AVG yeild- 17 pc

Avg cost of borrowing – 9 pc

Spread – 8 pc

Cost/Income @ 43 pc

Avg ticket size –

Home loans – 14 lakh

LAP – 7.7 lakh

Digital Loans – 0.7 lakh

Gold Loans – 0.75 lakh

Aim to reach AUM of 1 lakh cr by end of next FY

Company continues to remain cautious on unsecured lending / personal loans. Sounded skeptical of due diligence process followed by new gen Fintechs

Gold loan growth driven by company’s distribution strength

IIFL housing finance gets funding from National Housing Board at concessional rates – helps keep cost of funds under check

Company expects to maintain its NIMs at 7-7.5 pc or thereabouts

Management doesn’t see any credit demand slowdown if the economy remains robust – the way it is today

Avg life of Gold Loan portfolio is 90-120 days

Company believes, cost of borrowing has almost peaked in India. May move up-down by 10-15 bps, not beyond that

Company has slowed down its branch expansion spree. Should lead to lower Opex going fwd as more branches mature and their AUMs increase. Ex – IIFL’s gold loan branches have avg gold loan AUMs of 8 cr vs 22 cr for Mkt leader

Avg tenure of Digital loans varies from 6 months to 2 yrs. This is a high risk area. Hence the company is very aggressive in provisioning against Stage -3 assets wrt Digital loans. Despite that, returns are fairly attractive

LAP product in smaller towns etc has attractive rates. However, it also involves higher cost of origination like the cost of verifying the title, valuation of property etc

Q2 RoA @ 3.9 pc. Should be able to maintain the RoA range between 3.7-4.0

Credit cost range guidance given by the management @ 2 or thereabouts

Price war in Gold loans business witnessed in last FY is now abating. Hence the lending yields have gone back up

Co-Lending and Assigned books mainly consist of Gold, Housing loans and LAP

Current branch count at 4596 vs 3700 LY. As the new branches mature, operating leverage should kick in. On an avg, a branch breaks even in 18-24 months

Disc: Hold a tracking position, may add more, biased, not SEBI registered

Satin Creditcare Network (24-11-2023)

Any views on Satin Creditcare Network. Profit numbers look great to me.

CAGR expectation and experience (24-11-2023)

@sahil_vi I’ve calculated my CAGR return for my portfolio following your thread. But Zerodha Portfolio value chart gives us data for only one year. In this case how can one calculate the CAGR over years ?

Thanks

Praveen