Thank you for putting in excel . I was also wondering the same.

Sold my tracking position.

Thank you for putting in excel . I was also wondering the same.

Sold my tracking position.

@xvivek what they have stated is that every EV requires an lead acid battery as auxiliary power source in addition to Lithium-ion Batteries. However as per my checks, one with a 25+ years experience in mahindra’s production division and another with 10+ years experience in maruti service center, EV do not have lead acid battery as auxiliary power source.

IMPAL WORKING (back of the envelope)

CORE VALUE @ 300cr (6.5x PE)

LISTED @ 1000cr (850 sundaram)

UNLISTED @ 450cr (365cr Royal Sundaram @ 5kcr)

CASH @ 200cr

Total @ 1950Cr

IMPAL Market Cap = 1060Cr

Approx 45% Discount to actual value Approx 55% Discount to investments and cash if you remove the value of core biz.

I own Sundaram finance since a decade and absolutely love that company, I wouldn’t mind seeing this as an alternative to holding Sundaram Finance + Additional cash flows/Dividends from core biz.

Core biz is trading work with 15% ROCE (ICRA) and hence would give it only a Single Digit PE.

I have valued Royal Sundaram @ 5Kcr – In 2018 aegis gave a 3800cr valuation for 40% stake. There is an optional value of value unlocking here.

The company has a good Dividend payout policy.

I normally completely avoid Holding companies, especially those with minority stake but am willing to consider IMPAL because they have a core biz of their own and I have very high regards and faith for the TVS-Sundaram group.

RISKS.

As mentioned by Sandeep, you can use CROIC which takes 3-year average FCF divided by invested capital. Otherwise, you can use FCF of last year (strangely, FCF of current year is not available on screener) and divide it by invested capital. Invested capital can be equity + debt + reserves – investments – cash at hand.

Hi Sandeep,

I follow the principles and calculations done in this wonderful article written by John Huber:

This answers both of your queries in my view.

While I agree that rules need to be followed while starting a thread, a few of my posts on 52 weeks high thread didn’t get accepted. That thread seems like a privately managed thread where only a select few can post.

Disclosures: No investments

Stunning, in one word!

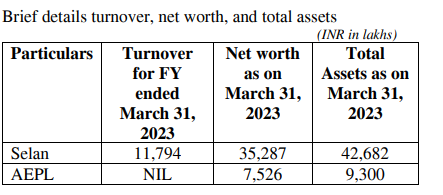

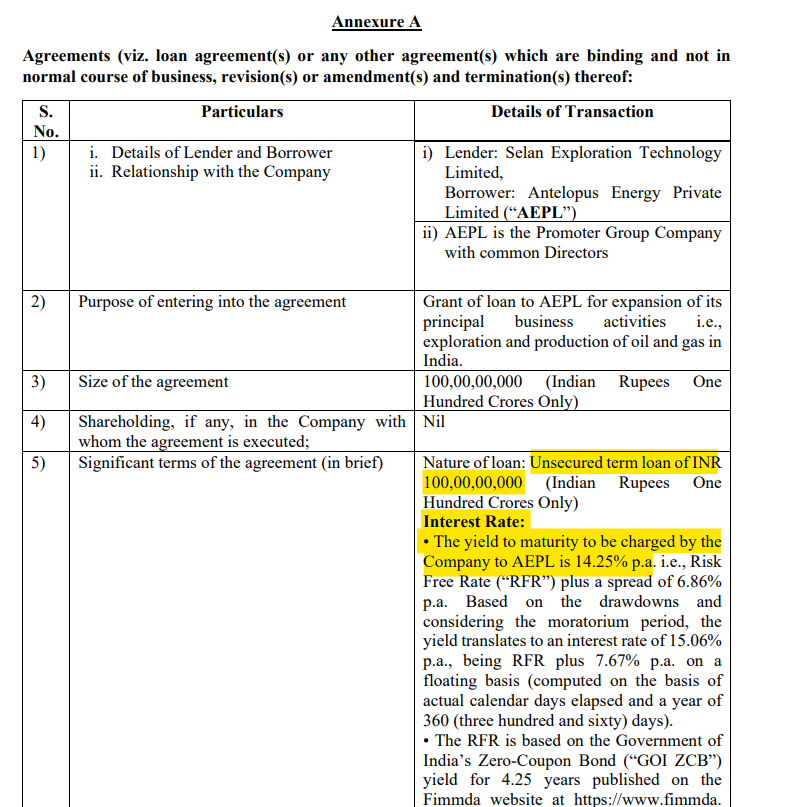

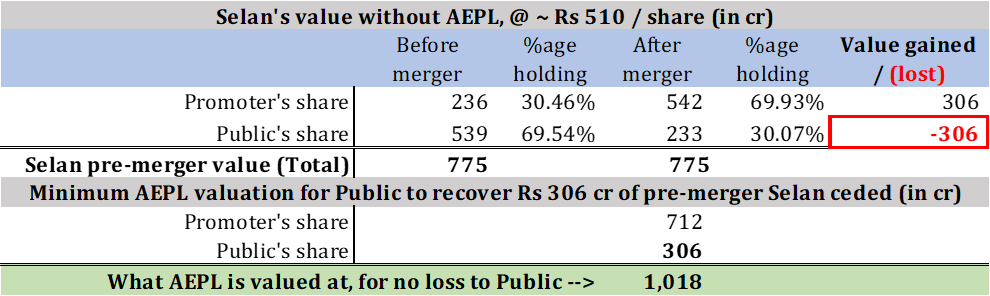

AEPL, a Promoter group company is proposing to merge with Selan Exploration, a listed company, with Promoter holding of 30.46% as on date.

Basics are as follows:

*

So the natural question is, what value does AEPL bring for getting in additional ~ 40% of the shares post merger. Selan has not yet said that in its filings. We can however find out the least it needs to bring in

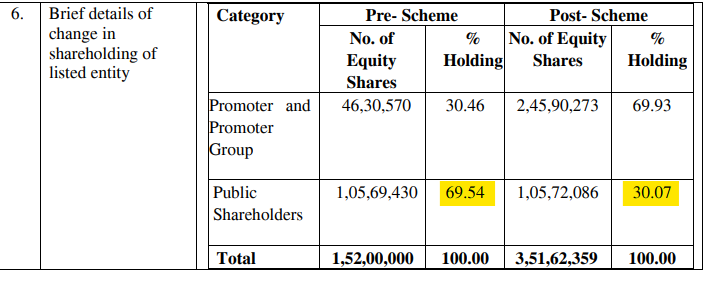

(a) Value held by Public shareholders in today’s Selan (i.e. pre-merger) = 69.54% of MarketCap of ~ ₹ 775 cr; i.e ₹ 539 cr

(b) Value of Public shareholders in today’s Selan after the merger = 30.07% of ~₹ 775 cr = ₹ 233 cr

Thus the Public suffers a substantial reduction in the value of today’s Selan held. This loss can be calculated as ₹ 539 cr (pre-merger) – ₹ 233 cr (post merger) or ₹ 306 cr of value of today’s Selan.

The Synergy and Audit Committee however have said the merger may “Enhance value for Company’s shareholders, resulting in creation of a leading energy company in India”

So the Public needs to see atleast commensurate value of what it has today; i.e ₹ 539 cr; post merger. But today’s Selan would contribute only ₹ 233 cr post merger. So the merger has to see the value held by the Public increase by atleast ₹ 306 cr.

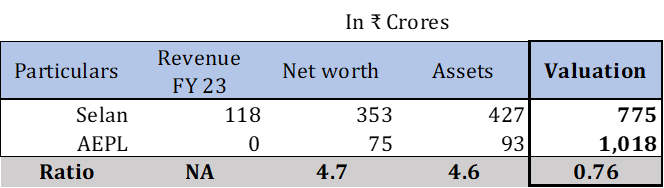

An increase of ₹ 306 cr of Public value, with reduced holding to 30.07%, means that the overall value brought in by AEPL is ₹ 1,018 cr (i.e. ₹ 306 cr / 30.07%). We can infer thus that AEPL is valued at ₹ 1,018 cr for the merger, while Selan is valued at ~ ₹ 775 crore today (as I write this). Thie fundamentals are below

Which is why I am really stunned!!!

But that’s not all. This “bigger than Selan” company entered into a loan agreement with Selan to borrow upto ₹ 100 cr of Unsecured loans at an effective rate of 14.25%!

It’s surprising that a better valued company than Selan could not get a better rate from the market and had to come back to Selan!!

Putting all of the above in an Excel sheet

Sources: All BSE filings

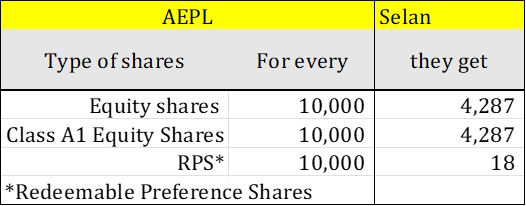

*could not understand how Pubic shares go up by 3,156 on account of the merger

Thanks for sharing this. PEL has around 20% unsecured book in the retail segment and that may get impacted. However, they may not face issues in retail mortgage loans. Not sure where the wholesale portfolio sits here.

Also being an NBFC they may have to pay higher rates in their debt financing which they have got from banks. However, considering the fact that they have one of the lowest D/E among NBFCs they are better placed in this category

Hi – you can use CROIC in Screener. it is FCF / Invested capital.