This is “hey are little more conservative when projecting the future” this is conspicuous from recent concall.

Posts tagged Value Pickr

Hikal – Pharma & Agrochem (22-11-2023)

The management eluded questions on any clear guidance in Q2 FY 24. Took a cue from past, not to focus more on guidance. Viraj Mehta’s question were good. too which the management have had hardly any clear answers.

What is your real return? (22-11-2023)

Is there any website or tool for finding XIRR or CAGR from zerodha or upstox trading statement or ledger. It is very painstaking process to count it manually. I am asking here as we need to also find what is rate of return when we are doing DIY method and compare it with index return. Thanks!

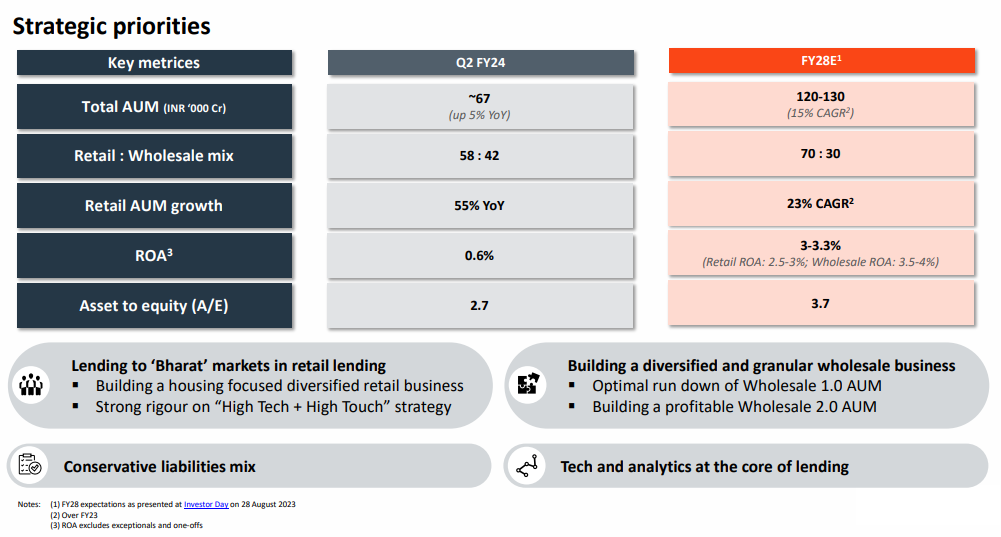

Piramal Enterprises Ltd (22-11-2023)

Largely the guidance if for ROA and Leverage for FY28…if you factor in both, we can see an implied guidance of ROE in the range of 11.1-12.2%

GMM Pfaudler: A safe way to play the Pharma/Chemical cycle (22-11-2023)

The reason for depressed price is that market has been punishing the company since the offer for sale. OFS was at price equivalent to 1750/share which at the time was at a steep discount to market price. Since then retail investors are probably worried about company taking such decisions again.

Kitex Garments Limited (22-11-2023)

Hi all,

New to the forum. Just curious. I am seeing discussion on Kitex since 2013 around on the Valupickr forum. However, is not it the case that it is facing stiff competition now from Cos like firstcry in newborn space? In my view, 2013 might have been good time for this Co but is it the same now? or Kitex still have advantage over Firstcry?

CARE Ratings Limited (22-11-2023)

Thanks for seeking my view. In my opinion, credit rating business in India is primarily depend on credit demand. In direct segment, it is bank loan rating or Debenture/bond rating which are borrowed by the companies. In indirect way, it is influenced by NBFC rating which also indirectly depend on retail credit and unsecured SME demand for credit in Indian market. If one look at FY2000 to FY2010 period, aggregate Scheduled Commercial Bank loan and advance (soured from various RBI Trends and progress annual report), the growth in 2010s was 23% CAGR which declined to 11% CAGR during 2020s.

That could have major impact on Credit rating demand as Bank account for significant portions of Credit demand. Further, in addition to credit, increased demand from SME/small corporates would also be better grwoth driver from Credit rating agencies perspective, as most of large Corporate are strong negotiator and try to cap their maximum fees. So even if bond raised during the years, increased from 1,000 Cr to 5,000 Cr. in a year, credit rating fees would constrained by cap in the agreement.

These two factors could be main factors behind moderate credit rating revenue growth in my view. However, increase capex , rising working capital demand and revival of SME could result in higher credti rating demand growth for next 3-5 years as compared with last 5 years in my opinion. My track record in forecasting can be defined best as pathetic which only 1 of 10 forecast being correct. So please read this para with bucket of salt and do your own anlaysis/due dilgience.

Disclosure: No major investment in credit rating sector, expect AGM pass holding in Crisil. My view may be biased. I am not recommeding any investment action.

Indian Microfinance Sector and the companies in the sector (22-11-2023)

Why NBFC’s which do Mircrofinance are specifically categorised as NBFC-MFI. We do not see much another classifications in other areas like vehicle finance, personal loans. One other case is Housing finance, where if you got classified as NBFC-HFC. In this case, they can access funding from NHB which is a low-cost funding. Once the size of NBFC reaches certain size, seems this low cost funding also stops. Recently IndiaBulls Housing mentioned that they are asking RBI to classify themselves as NBFC instead of NBFC-HFC, since there is no advantage is getting classified as NBFC-HFC.

On similar lines, what is the benefit companies are getting if they are getting classified as NBFC-MFI?

GMM Pfaudler: A safe way to play the Pharma/Chemical cycle (22-11-2023)

with new acquisitions on mixing business is a 3bn sector and service revenue part of the business is the runaway. Revenue visibility may improve

CG Power & Industrial Solutions – Capable management, good business & industry tailwinds (22-11-2023)

Major Investment Planned in Outsourced Semiconductor Assembly and Test (OSAT) facility

CG Power has filed an application with Ministry of Electronics and Information Technology (MeitY), Government of India seeking approval to set up an Outsourced Semiconductor Assembly and Test (OSAT) facility and the grant of subsidy for the said project under the Modified scheme for setting up of Compound Semiconductors / Silicon Photonics / Sensors Fab/ Discrete Semiconductors Fab and Semiconductor Assembly, Testing, Marking and Packaging (ATMP)/ Outsourced Semiconductor Assembly and Test (OSAT) facilities in India. It may be further noted that, subject to the project and the subsidy being approved, the Company proposes to implement the same as a Joint Venture in partnership with technology providers/anchor customers, which are under discussion.

The estimated investment on the project over a period of five years is USD 791 million and the same is expected to be funded by a combination of subsidy, JV Partners equity contribution and debt, as required.

Disc: Invested in both CG and TII. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.