Strong management commentary, giving volume guidance for 5MT which would be 18% yoy growth over 4.2 MT of last FY.

As H1 volume was around 1.8 MT, H2 volumes would be around 3.2 MT

PAT margin improvement seen over last year in the results.

Strong management commentary, giving volume guidance for 5MT which would be 18% yoy growth over 4.2 MT of last FY.

As H1 volume was around 1.8 MT, H2 volumes would be around 3.2 MT

PAT margin improvement seen over last year in the results.

This is First Global , Devina’s Presentation. Out of top famous 20 PMS, only 4 PMS have beaten Nifty 50 from March 2020 till date. So 16 PMS have not even been able to beat the larger Index. And if you consider the actual buy and sell of PMS investors and Taxes paid on them, then their returns will be still lower than even these shown returns.

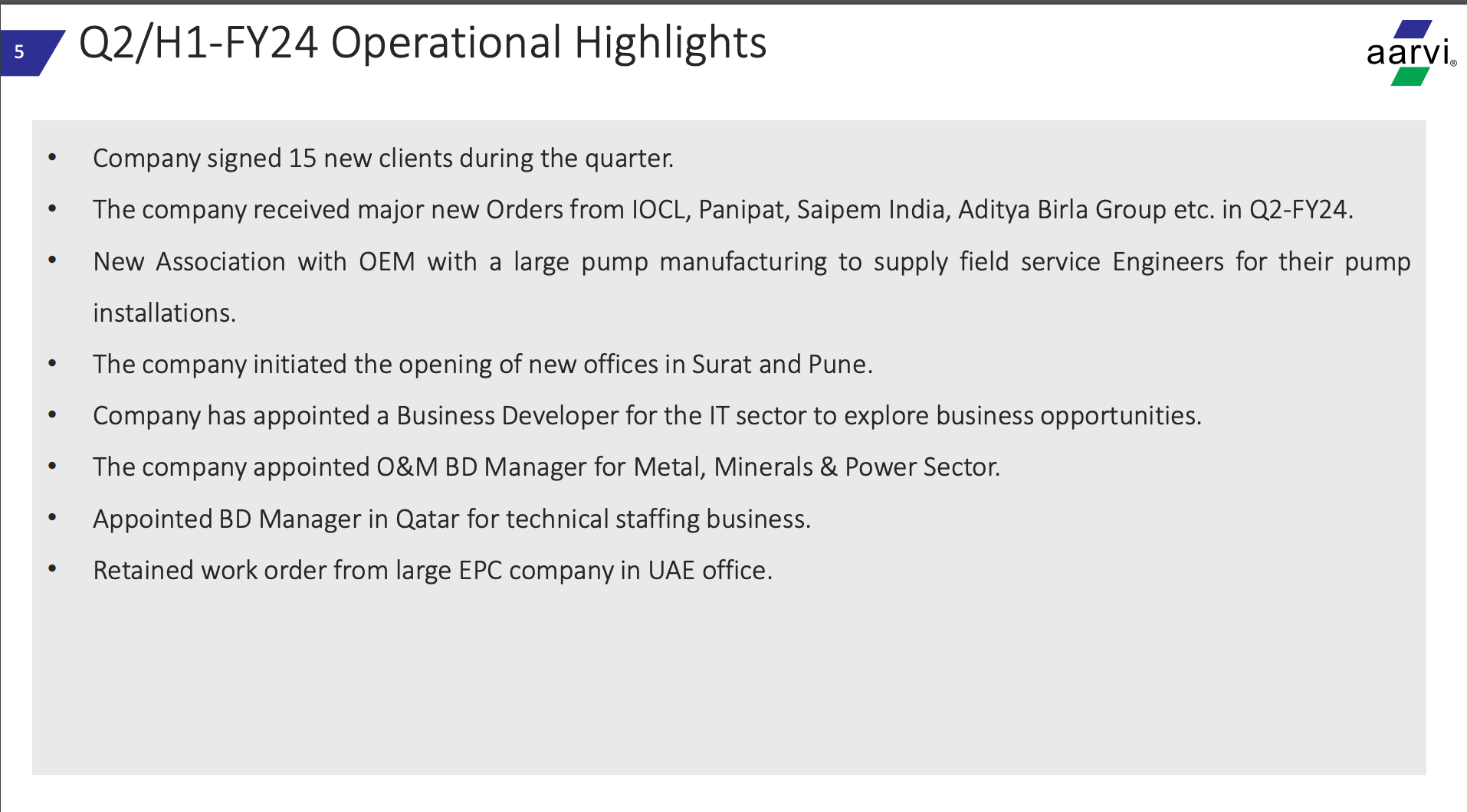

The company has done an acquisition in UAE in May 2023 https://archives.nseindia.com/corporate/AARVI_29052023204059_NSE20232405Acquisition.pdf

The latest investor presntation covers the operational highlights, hinting at better business prospects in coming months.

Disclaimer- Invested.

Please add a stock wise rationale, otherwise this thread is meaningless. I don’t think any of the parties have announced anything specific which affects the stocks listed above.

Company is pretty aggressive in revenue recognition. CFO was 11cr but PAT was 30 cr, i.e. CFO/PAT is 39%. This looks like red flag. CFO/PAT in previous years were 19% and 39%.

Usually a rising tide lifts all boats. In the kind of bull markets we are in, most sectors will fare well.

Very few sectors are there which are still lagging in this market. That is more to do with the kind of headwinds these sectors face. And there we are not too sure how long these headwinds are going to last and when the good times going to come back.

Personally my philosophy is exactly opposite to what you mentioned in the first statement. I am always interested in what is in fancy or what is going to catch fancy in the markets. That’s where I feel most money is made. So I don’t bother myself with sectors which are not market favorites.

Stocks and sectors that are languishing at 52 weeks lows or lower during a raging bull market are there because of a reason. And many a times when markets correct they fall even more. So even though on first glance these kind of names appear to have fallen a lot from their peaks, valuations may not have become too cheap.

@Shakti_Srivastava I don’t track Mold Tek.

@rjs391 Portfolio construction strategy has been discussed in the past in this very thread. I usually hold between 6-10 stocks in my portfolio, sometimes based on opportunities stretch this to 15 stocks. While exiting a stock it’s an allround decision based on technicals, fundamentals, froth, stop loss, whatever applies. I don’t track Genus power.

@ram1984 GAIL is in a strong uptrend, though being a large cap PSU stock, upmoves are slow as of now. Resistance is at 130 and slightly above. Fundamentally I find it difficult to analyse this kind of business. PSU fever is strong in the markets. Idea should be to ride this sector till there are signs of exhaustion or reversal

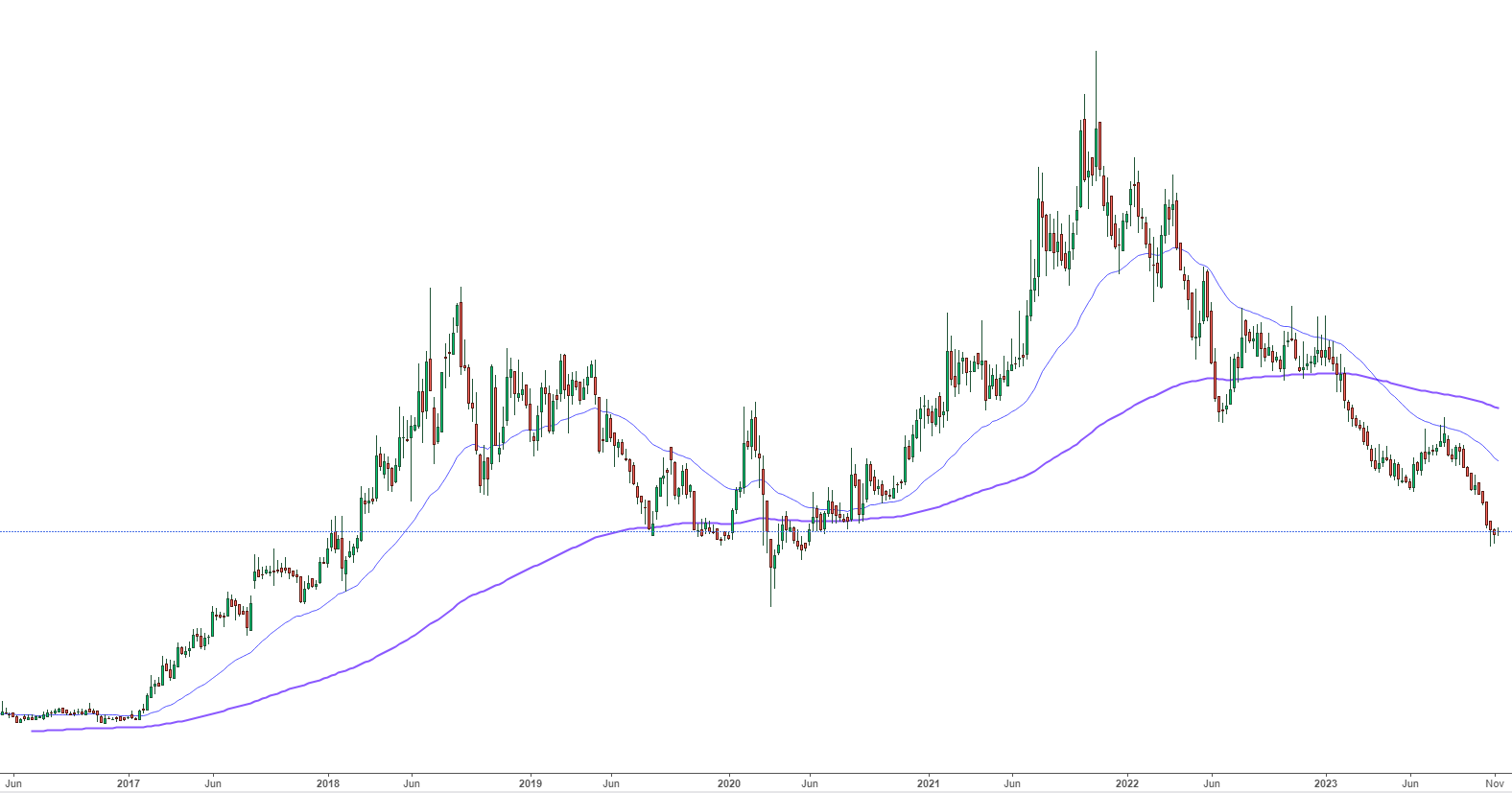

Any opinion on the setup of the below price chart?

To add to your statementsthe market size of 1000 cr ,there will be margin erosion as well as exports have better margin.

I think the worst part is how Lt foods is riding the super cycle while krbl is not able to ,these are small windows where cyclical companies can increase cash reserves and as investors for us are handsomely rewarded with increase in share price

any take on dhanuka after latest result?

Fixed asset base has almost doubled. good latest quarterly result.

Portfolio Update:

| Stock | Cost % | Latest % | Avg Holding Period |

|---|---|---|---|

| Omfurn India | 31.60% | 27.20% | 42 |

| Holmarc | 10.35% | 12.51% | 54 |

| PNGS Gargi FJ | 6.26% | 10.38% | 137 |

| Bondada Eng | 5.66% | 10.32% | 52 |

| Chaman Metalics | 4.73% | 4.49% | 213 |

| Labelkraft Tech | 6.45% | 4.27% | 185 |

| Aurangabad Distill | 4.29% | 3.94% | 51 |

| Knowledge Marine | 0.76% | 3.16% | 467 |

| SKP Bearings | 4.56% | 3.05% | 7 |

| Saakshi Medtech | 3.86% | 3.05% | 41 |

| Kotyark Industries | 2.31% | 3.02% | 299 |

| Evans Electric | 2.46% | 2.92% | 135 |

| Technopack Polymers | 4.28% | 2.70% | 89 |

| Felix Industries | 2.82% | 2.10% | 31 |

| Cosmic CRF | 1.76% | 1.38% | 30 |

| Cadsys | 1.91% | 1.27% | 60 |

| Oriana Power | 1.85% | 1.24% | 51 |

| Silicon Rental | 1.66% | 1.23% | 89 |

| Perfect Infra | 1.28% | 0.95% | 80 |

| Markolines | 1.13% | 0.84% | 95 |

New Entries:

SKP Bearings:

Good Business, Decent Capex coming into play, good results and less decent valuation.

Re-entries:

Cosmic CRF:

Re-entered on expectation of good results and incoming orders. The litigation issue persists though.

Exits:

Magson Retail:

Despite flat results, the share price rose due to HNIs and hence exited.

Uma Converter:

The valuations still are way ahead of the bottom-line results. Classic Pre-IPO window dressing levels are far away and other factors continue the company being sub par.

EP Bio:

Bad Results. The employee expenses have gone over the roof and due to this the bottom-line is flat. Emp exp may be RPTs so exited.

H1 Season:

The results were mixed as a whole, but majority have negative Operating Cash Flows (even prior positive cash flow companies turned red).

Positive results from companies:

Omfurn: Good Growth numbers and around 12-13 months order book still on hand.

Bondada Eng:

H1 Fy 24 vs H1 Fy 23 are great. H2FY23 comparison is decent.

PNGS Gargi:

Consistent Results.

Evans:

Highest ever op margins along with net profits (but with negative cash flows)

Cosmic CRF:

COSMIC CRF LIMITED – sme – #21 by Dhvanit_Merchant17.

Overall SME exposure is now at 95% and no new investment is done in SMEs (except SKP Bearings arising from sale proceeds of others on poor results)

Average Holding Period reduced substantially due to tax harvesting done in September and despite this the holding has increased to 115 days.