Source: CEEW how-can-india-scale-lithium-ion-battery-manufacturing-sector-and-supply-chain

I tried doing reverse DCF for Panama Petrochem stock, just to see with the current price, what are the implied market expectations. The results are astonishing and clearly indicate that at the current level, market may not have fully optimized its potential in reflecting its true worth as far as current price is concerned. It also checks out almost all-important parameters of my checklist which I published few days ago here:

Portfolio of a novice investor – Q&A: Questions & Answers / Portfolio Q&A – ValuePickr Forum

Sales Growth Rate:

Historical sales growth rate (CAGR) for the company over last 10 years has been 15% but the market is implying only 2%. Looking at this wide difference, it seems that market hasn’t valued its potential to the full extent.

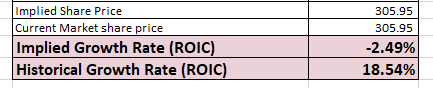

ROIC

Historical growth rate for ROIC is around 18.5% but market is implying degrowth in ROIC which is reasonable as with this kind of company without any specific competitive advantage, ROIC may not sustain for a very long time.

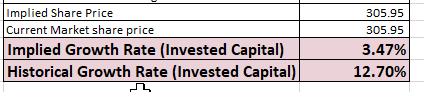

Invested Capital

Historically, Invested capital has grown by 12% but market is implying only 3% which can again be a sign of undervaluation like the sales growth.

Disc: Invested and biased.

Frontier Springs – First ever call

As of now, the segment breakup information remains undisclosed. The company recently listed on the SME, resulting in limited available data. However, apart from inventory adjustments as disclosed in results pdf, preliminary market research suggests a sales mix comprising high-margin products, notably key cabinets (gaining volumes as offices reopened since the work-from-home trend ended and it’s a corporate product) and its proprietary line of luggage, manufactured in-house. These margins are not going to be sustainable once contract manufacturing business picks up, however as the founder claimed it will help them touch 100 cr sales this year itself i.e 80 cr in H2, so even a 12-14% ebita margin instead of current 40% could lead to decent EPS.

What has led to significant jump in their margins in Sep 23 financials? Are they sustainable?

I believe, this return of money to ministry should get it of the hook. The time taken is material.

It’s other verticals are doing well. But EV subsidiary is the main driver of growth. It’s scooter sale at acceptable price(with subsidy) is essential.

If it dips more I will buy.

Every top level resignations write personal reasons, how to differentiate.

Update:

On Ethos : One point stood out in the concall. Arund 53.00 minute its claimed that the new jewellery venture – would start to become an second engine or additional engine to the comapny growth.

This point has not been commented on much before for the company. So something to consider and calculate.

Additional point is Margins are probably peaked and should stabalize around this range. So any growth henceforth will depend on top line alone.

Historically the company has struggled with its topline and the CU, so I think we should primarily be giving much importance to the topline.

Significant topline reduction in this quarter and lower guidance for the year, is definitely negative (reason why having cheap valuations)

*Disc: had some position earlier but sold off now.

All my portfolio companies declared earning results for the third quarter. After a long time I did not need to make any changes to my portfolio companies based on earning results. All except Mold-Tek reported year over year revenue and earning growth in the latest quarter. I am not selling Mold-tek as management has secured a patent on the technology and production will start for pharma companies in the coming quarter. If possible I will add more when the price consolidates.

After declaring poor results in the previous quarter, Granules India’s stock price appreciated a lot with so-so result declared in the latest quarter. In fact it became 3X to 4.5X due to a massive run up in stock price in the last 3 months. Another winner in my portfolio is Ethos which keeps on reporting double digit earnings and revenue growth and as a result stock price doubled in less than 14 months. I started buying Zomato in the 60s and kept on buying till the 90s. It nicely mimics the result and stock price movement of DoorDash listed in the US stock exchange. Other winners are Varun Beverage. APL Apollo and MAS financial. All these companies are on the verge of entering the multibagger list of my portfolio companies.

As the Indian market is hitting new highs, my portfolio has reached a new high. Not sure how long this dream run will continue. At present all my portfolio companies are in green and at least giving 25% return with 9 multibaggers. I experienced a similar boost in my US portfolio during the 20-21 bull market. But it just took less than a couple of months to reverse all the gains due to inflation and recession risk in the 22-23 bear market. I am yet to recoup all my losses in the US market even after a couple of years sticking with the same set of companies. US Small and Mid cap indices are still down more than 25% from all time high. It seems easy to make money now in the Indian market but it’s equally difficult to make money in the US market. I am not sure if the broader Indian market may also experience similar difficulty in the not so distant future. This conflicting prior experience from two different markets keeps me grounded and cautious while investing new money in the Indian direct equities at an all time high. I hope this dream run in the Indian market continues forever and makes all of us wealthy in the long run:)

Portfolio 5 yrs return 19.7%

Portfolio 3 yrs return 27.3%

Portfolio 1 yr return 15.9%

Disc. This is not a buy/sell recommendation. Biased as invested in all stocks discussed above. Not a SEBI registered advisor.