Is anyone has idea how long KRBL will suffer because of this litigation and how serious it is? It would be really painful to loose market share to competetor if things get delayed significantly.

Posts tagged Value Pickr

IZMO- bet on new technologies in Auto retail & defence (18-11-2023)

The ‘largest repository of auto images’ > Can it not be commoditized by AI image generators. Anyone can generate any auto image they want now using AI. What’s the advantage of a repository?

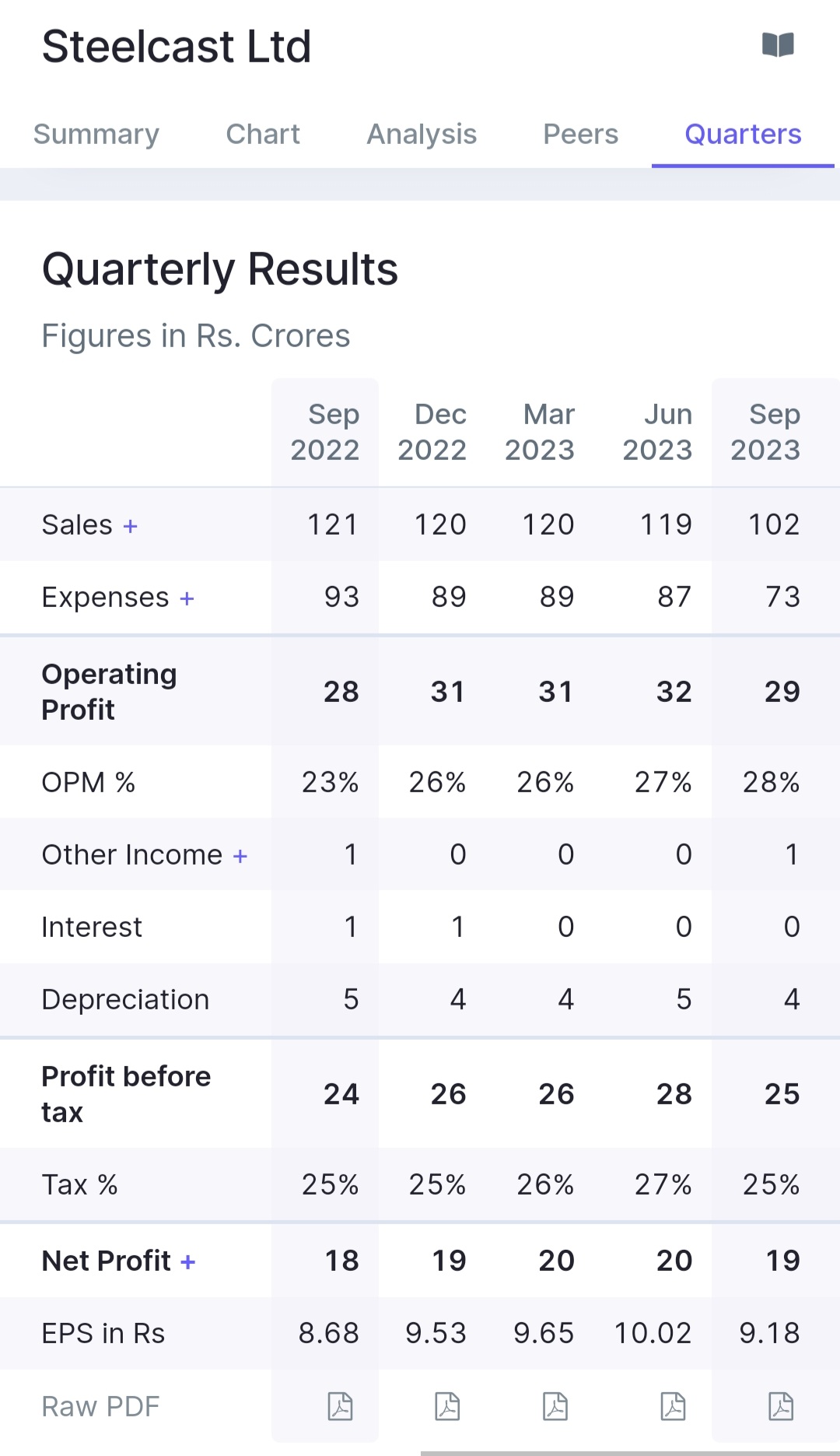

Steelcast Ltd – leading steel castings (18-11-2023)

In latest quarter, although the revenue declined but the profit grew. The OPM grew from 23% to 28%. Stock price also corrected by approx 15%.

If we consider 3 or 5 years period, the current PE ratio & EV/EBITDA is less or around the median PE & EV/EBITDA.

It looks like still a decent entry point to me.

Disclaimer – Not invested just tracking

Carysil (earlier Acrysil) – Kitchen sinks (18-11-2023)

My notes on concall

Management has guided for 1000.cr revenue in fy25 and it is on track to achieve that.

Discussion with customers for some big orders for granite sink which should materialize in 1/2 quarter.

Steel sink & tap business should be doing well.

Have lately seen them in action in terms of marketing with “cook with carysil” campaign.

Even with headwinds in europe and other countries they are delievering growth so with some tailwind they should do better.

They already have land and capex for growth . To see when they start to put that to action thats where next leg of growth above 1000 cr will kick in.

To me overall it appears to be directionally positive in terms of business momentum

Margins may remain around 20 % mark for now as guided by management

Disc – Invested no transaction recently.

Malhar’s Investing Thoughts (18-11-2023)

Temporal Alignment in Investing

In meeting well over 200 investors and fund managers over the past couple of years, I have recognised something that separates the best from the rest: alignment. Alignment of interests, and alignment of time horizons. This post is on the latter.

Suppose a find has a long-term investment philosophy, e.g., an average holding period of 8 years. While raising funds, it is tempting to accept limited partners with shorter time horizons, in a quest to grow assets under management (and thus, fees). But doing so can wreck all sorts of havoc: furious clients begin calling after a quarter of negative returns or underperformance, not recognising the managing partner’s much longer outlook.

The very best fund managers I know turn down — refuse to accept — potential clients, when they sense misalignment. They focus instead on attracting aligned capital.

Say no to misaligned capital. One rupee of aligned capital is worth hundred rupees of misaligned capital.

— Mr Utpal Sheth (source)

Doing this is difficult in the short run, since it entails willingly forgoing fees. But in the long term, it imbues the fund with what my mentor calls temporal leverage: the ability to survive in order to thrive.

Consider Nicholas Sleep and Qais Zakaria, who co-ran the Nomad Investment Partnership and returned ~20% CAGR over 20 years.

They also took delight in turning away investors who seemed unsuitable or irritating, regardless of how rich they were. Zakaria chuckles at the memory of a comically awful meeting with a team that managed billions for heirs to the food-packaging company Tetra Pak. These financial advisers demanded access to Nomad’s proprietary stock research as a condition for investing their clients’ money in the fund. Zakaria says the atmosphere grew “frostier and frostier,” with Sleep crossing his arms and legs in a sign of mounting annoyance. After fifteen minutes, Sleep and Zakaria showed their visitors the door.

— Richer, Wiser, Happier by William Green

Mr Nicholas Sleep

Beyond investment management, I can think of 2 parallels of how misaligned time horizons cause problems:

- Asset-liability mismatch (ALM) in banks and NBFCs. Nearly every banking and NBFC failure (apart from outright fraud) involves ALM: borrowing short term and lending long term. In theory, the lender can roll over their borrowings repeatedly. When the goings are good, this works perfectly well…that is, until the tide turns.

- Companies that want to build for the long term are almost always punished by public markets (in the short term). Investing for tomorrow’s profit pools entails forgoing profits today: something not appreciated by most analysts and hedge funds, who prefer higher earnings next quarter. It is crucial to have shareholder-management fit, which is why Mr Sridhar Vembu — one of my favourite thinkers — makes it clear that Zoho has no plans to list anytime soon: they are building for the long haul.

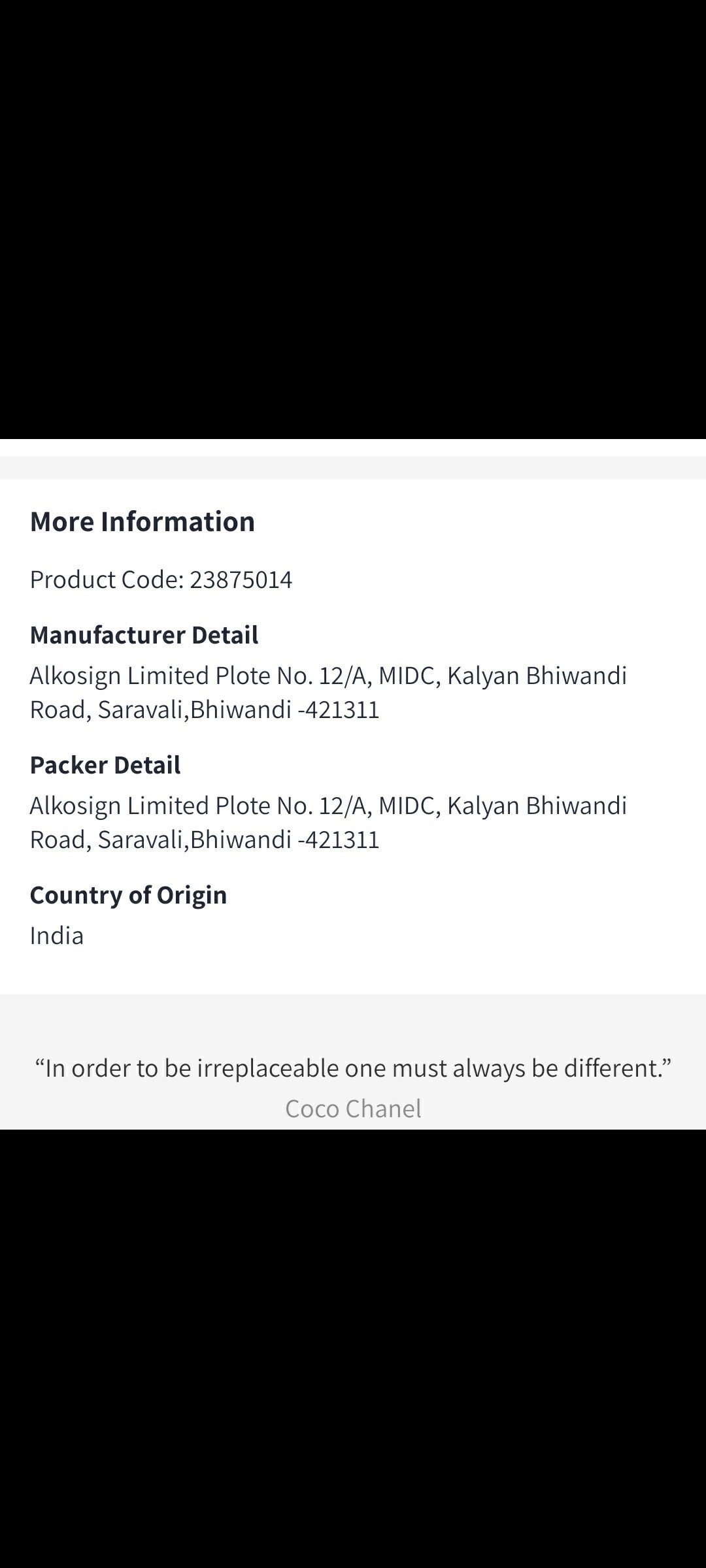

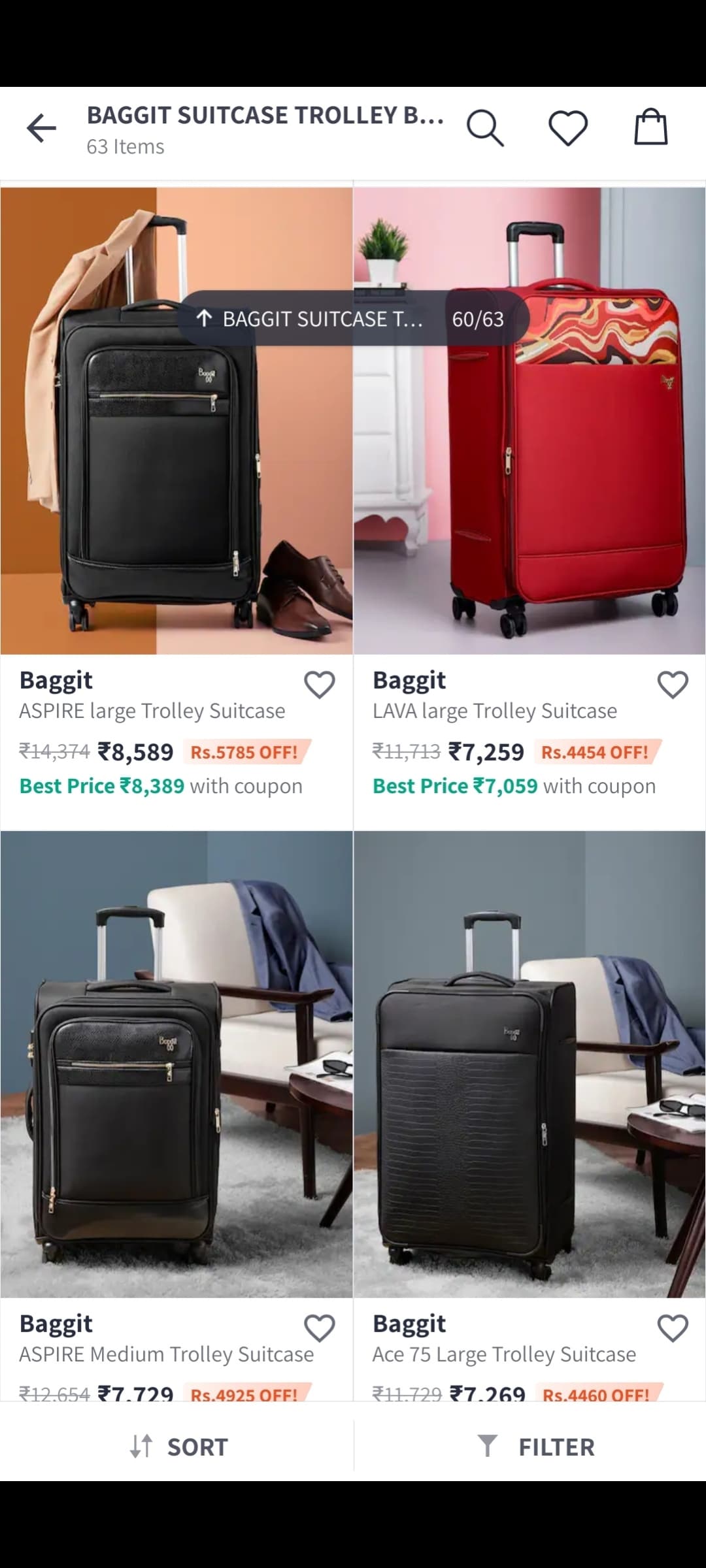

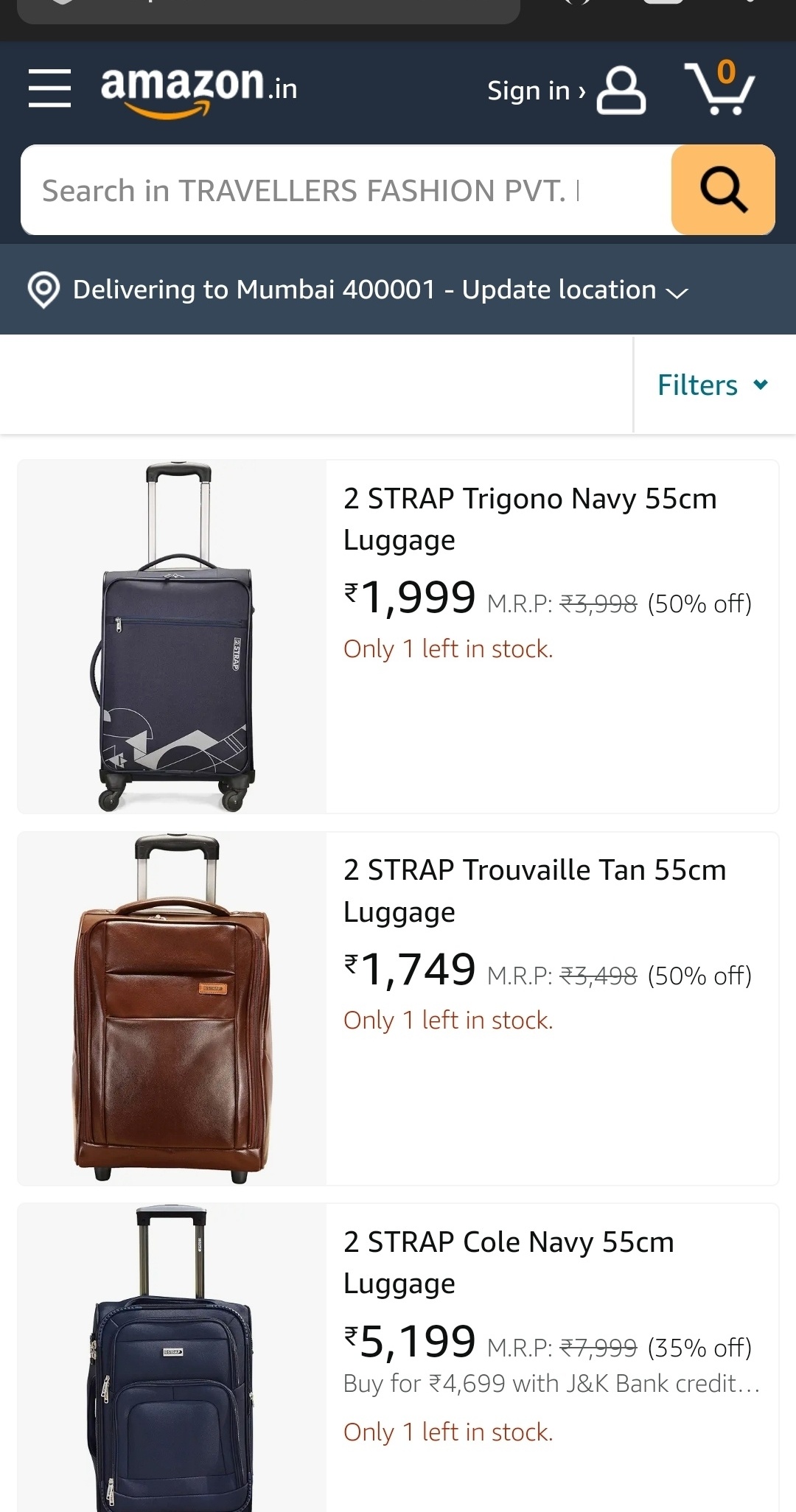

Alkosign – A market leader in white boards and school furniture entering hard luggage market (18-11-2023)

This post is about a small cap that I may be invested in, it’s a very risky bet due to the company being small and not much information about management credibility. Hence pls don’t see this as any kind of recommendation.

Alkosign, a micro-cap company with a market cap of around 100 crores and a relatively small free float of approximately 10-12 lakh shares, has shown a sudden surge in sales and operating profit, notably doubling and quadrupling, respectively, in its latest reported numbers. The key catalyst behind this uptick was unveiled in a founder’s interview where it was disclosed that Alkosign has ventured into manufacturing hard luggage for the well-known brand Baggit.

A firsthand investigation, including visits to Baggit stores in Delhi and online platforms like Myntra and Amazon, confirmed Alkosign’s involvement in producing Baggit’s entire range of hard luggage. Despite the typically low margins associated with luggage contract manufacturing, Alkosign’s own line of hard luggage under its brand name adds an interesting dimension to their revenue stream.

The CEO’s ambitious target of reaching a 100 crore turnover was discussed in the interview, and the prospect of achieving this goal appears feasible, given the new venture into hard luggage. Notably, Alkosign’s association with Piyush Pushkar of Suvid Retail, who shares directorship with Mr. Sameer Shah in a subsidiary responsible for marketing and venturing into hard luggage, adds promise. Piyush’s previous experience with Brand Concepts, now manufacturing for major brands like Tommy Hilfiger, lends credibility to the venture. The hard luggage arm of alkosign is travellers fashion pvt Ltd.

While contract manufacturing can drive revenue, it’s acknowledged that margins may not be as robust. The strategic move to ride the travel trend through Baggit, coupled with the expertise of Piyush from Brand Concepts, presents an interesting growth trajectory. The recent substantial investment by astute investor Mona Laroia in a bulk deal adds a positive dimension, making Alkosign a compelling wait-and-watch play in the market.

Link to YouTube interview – https://youtu.be/6nogIaxMv58?feature=shared

Link to twitter on detailed post with pics as unable to upload pics of luggage and shareholding details:

https://twitter.com/BOOMBERG_SQUINT/status/1725528393595162966?t=zAZUdU3Jb6ibSX7zd66gSA&s=19

Multi-Disciplinary Reading – Book Reviews (18-11-2023)

Quality of Earnings, Thornton O’Glove, 1987 – The author is one of the earliest accounting skeptics, having done his bit to advance forensic accounting. It is not always about spotting fraud or shorting opportunity but the techniques can be useful to understand how aggressive is an orgs accounting vs peers, or to even foretell problems. It discusses how to read a AR, what to look for between income statements, ARs, cash flow and balance sheet, how to spot discrepancies, how to weigh in on the audit report etc.

My notes –

-

IPO Mania in the 1950s – Many companies had nothing more than a romantic name, high-flying ambitions and a willing set of brokers eager to place them and reap the rewards

-

In a IPO mania, very few even read the prospectus and still made money. Genuine knowledge matters little in the short run, esp. in an emotional market

-

The pros should seek out bad news while the amateurs may only want to hear the best about the stocks they own

-

Author always assumes the worst of managements and thinks they are always upto hiding things with cosmetic adjustments

-

Most people prefer illusions to reality, as long as it conforms to their committed view

-

Author wanted a job telling people what stocks not to buy

-

Bear market of ‘69-’70 – investors no longer wanted to learn how to double money overnight but were looking for excuses to dump whatever stock they owned to preserve whatever capital remained

-

Celebrity is a person famous for being famous (Daniel Boorstin)

-

“Better a highly quotable ignoramus than an astute scholar who can’t gather his thoughts” (journalists look for quotable quotes)

-

Prices reflect only the view of optimists – though there might be pessimists around who believe it should trade cheaper – they may not do anything (natural tendency for prices to drift upwards)

-

Analysts must be on good terms with the businesses they cover, so offer supportive commentaries (hence 86% of brokerage recos are neutral or buys, 12% are sells and only 2% are strong sells)

-

If you put out negatives on a stock, the people who own it hate you, the management hates you and the ones that dont own it dont care (lose-lose situation)

-

Jim Chanos doesn’t visit managements of businesses he is bullish on so as not to be blindsided by them

-

4 types of auditor opinions – 1. clean (unqualified acceptance) 2. subject to (accepted subject to pervasive uncertainty) 3. except for (unable to audit certain parts of the company) and 4. disclaimer (most negative). Most opinions are clean and few fall in #2 and #3 while #4 is rare (until its too late)

-

CPA firms that do audit work for low fees cannot sustain quality work

-

For the big 8 firms, audit was merely a opening for consulting business – auditor opinions fence were always favorably biased to keep other business

-

Annual reports either play down bad news or hide it in the back of the statement. No one says this has been a bad year and we dont expect next year to be good either (although this happens so often)

-

Safe and sure in the knowledge that most investors dont read old reports, managements make promises they cant keep

-

A sudden shift in gears is indicative of a situation that will not run around fast (when optimism turns to pessimism)

-

Abnormally large inventory is one of the most certain signs of trouble ahead

-

Stocks of managements that involve in hype also fly at least in the near term (Keynes beauty contest)

-

A frank discussion of the problem (in an AR), along with thoughts of proper solutions, is a mark of a management that can be trusted. ARs should be looked upon as sources of info and not literary masterpieces or wellsprings for inspirational prose

-

Differential disclosures – when what a company says doesn’t match between documents

-

When managements use the word “challenge”, they mean “trouble”

-

When a company has two streams of revenues – say from insurance and from real-estate, the former is more durable stream (higher quality of earnings) while the latter is hard sell, volatile business (MOSL for eg. has HFC, WAM, Brokerage and Capital markets – first two are durable and last two very cyclical)

-

Pay close attention to reported earnings – are there things which should be in “Other income” included in operating earnings? There’s a large latitude based on “intent” here for businesses to play with – where they sometimes include sales of a real-estate asset or investment portfolio in operating income

-

Accounting bath – when large write-off happen after a new management takes over (Spandana for eg.) and with the slate clean, profits tend to rise over following years – it makes the management look good that they turned a loss-making entity into profit-making one

-

When the treasury officer or CFO is contributing to profits than the engineers, be wary

-

Income statement can be made to look good by adjusting SG&A (with some one-offs), tax rates or adopting a more liberal method of depreciation (as E2E did recently)

-

For QSR, with lower labor costs and overheads, small RM price moves can affect margins by a lot

-

For cost changes – understand what part of it are one-offs and what is sustainable (product mix, efficiency, RM costs can all be sometimes one-offs)

-

Most orgs maintain two sets of books, one for the shareholders and another for the IRS (Tax). The tax book could be more conservative and is more indicative of cash flow (even depreciation methods could vary between the two)

-

Oil and Gas companies (exploration) could use full-cost or successful effort accounting – in the former expenses are capitalised leading to better income statement than latter

-

Revenue recognition could be done using percentage completion method for income statement while for tax statement it could on delivery to customer

-

An org may start with less aggressive policies but may switch to aggressive ones to maintain the facade of growth

-

It is time to play devils advocate when receivables go up more than avg. or when inventory gets bloated – alarm bells should go off. Latter esp. is a good indicator of future slowdown

-

Companies can stockpile inventory but not services (key diff between the two types of businesses)

-

Increase in RM inventory usually mean business is speeding up (unless its a Covid-type risk being averted). Shilchar was a good eg. of this from FY23 AR (idea for re-entry came from this book)

-

Finished goods rising in a business with rapid change in products and taste (fashion retailer) could be bad news

-

Negative inventory divergence – finished goods rising while RM inventory is falling – clear sign of future distress (unless its a seasonal business, stocking up for the season)

-

In the 80s inventors became aware that debt was a crucial part of the balance sheet and was no longer deemed dangerous (dropping interest rates)

-

Rising stock market diminishes the urge to go private as takeover bids become more expensive

-

Few purchasers of long-term bonds intend to hold them to maturity – they buy them in the expectation that interest rates will decline and bonds appreciate in price

-

Revenues of a healthy company are used to pay for past (interest), present (wages, rents, RM) and future expenses (R&D and expansion). Ailing corps in stagnant industries increase payouts

-

In a majority of cases, prices of a common stock is influenced by dividend rate than by reported earnings – expanding, while paying consistent and increasing dividends – deserves to trade lot higher (These ideas also change based on market conditions and discount rates)

-

A firm that continues to pay dividend even in distress is stupid – Avon paid dividend while divesting its cash cow – its the equivalent of burning everything, incl. the ship to keep it going (Check Vedanta or Banco Products for eg.)

-

GAAP is more CRAP (Common Reported Accounting Principles)

-

LIFO vs FIFO (former could depress no.s in a rising RM scenario while latter would look more green), depreciation (straight-line vs accelerated), r&d expensed vs capitalised or the way pensions are accounted could all changed perceived value of a company many fold – the temptation to switch to aggressive accounting is hence irresistible (esp. if CEO compensation depended on stock price)

-

Only 16% of NYSE listed corps. had utilized accelerated depreciation

-

Accountant with a sharp pencil and a sharper mind can re-rate a stock

-

When management sets the stage for a big bath – it writes off every dubious asset in sight – plant & equipment, inventory are written down to a low level to present the bleakest picture possible so the sunny picture might be presented by the new management

-

Stock prices of companies doing a big bath fell in the month post write-offs but rose subsequently (very common pattern – see AurionPro in FY21)

This books reads like a laundry list of all the things orgs typically do, to make their numbers look better. It was a breezy read and while there isn’t a lot that is new for someone who has read a handful of investing books, its still useful to remove the rose-tints off the skeptical lenses in a bull market. 9/10

Sound sleep providers ..CYCLE is on HOTELS (18-11-2023)

EIH Q2 concall highlights –

Sales – 552 vs 417 cr, 32 pc

EBITDA – 165 vs 101 cr, up 66 pc

PAT – 94 vs 22 cr, up 256 pc

Net cash on balance sheet @ 509 cr

Out of the total revenues, revenues from flight catering and airport lounge business @ 100 vs 56 cr, EBITDA @ 37 vs (-) 3 cr

City wise Rev Par growth (YoY) for EIH properties in Q2 –

Agra – 60pc

Delhi NCR – 38 pc

International – 28 pc

Jaipur – 28 pc

Bhubneshwar – 26 pc

Chennai – 23 pc

Mumbai – 19 pc

Kolkata – 12 pc

Hyderabad – 12 pc

Bengaluru – 9 pc

Udaipur – 7 pc

Cochin – (-) 11 pc

Chandigarh / Shimla – (-) 35 pc – due floods

EIH Domestic hotels ( including managed ) vital stats – Q2 (YoY) –

ADRR – Rs 16500, up 23 pc

Occupancy – Flat

RevPAR – Rs 11865, up 20 pc

National presence –

12 Oberoi branded hotels

10 Trident branded hotels

Total rooms @ 3772

International presence –

07 Oberoi branded hotels

Total rooms – 497

Growth in ADRRs (YoY) in luxury / 5 Star part of the Industry is in 20s vs low teens for 2-3 star properties

Current number of 5 star and above rooms avlb in India @ 1.65 lakh. New supply coming on stream till FY 28 @ 0.55 lakh. Basically the demand – supply dynamics look good for next 5 yrs !!!

CWC should help the company in Q3 wrt rates, occupancy

Q3 – recovery in Shimla has been promising specially at The Cecil. The Windflower hall is taking slightly longer for full recovery as Cecil receives greater chunk of foreign tourists ( specially from UK due to its Historical value )

Middle East properties are seeing some pressure due to the ongoing Israel – Hamas conflict

EIH – vision for 2030 – minimum 50 more hotels with additional 4500 keys ( including managed Hotels ) – Confident of achieving the same. 03 hotels already in pipeline – Tirupati, Rajgarh, Vizag

Business in H2 should be good

According to Mr Oberoi- despite sharp increases in ARRs across 5 star properties, there is still a lot of head room for further growth

RIL has announced that 03 of its properties ( 02 in Mumbai and 01 in UK ) shall be managed by EIH in near future. The UK property is a 47 room hotel, purchased by RIL in 2021. The two groups shall also develop a new property in Gujarat the details of which are not yet known

RIL owns 19 pc in EIH. Another 14 pc is owned by ITC

Disc: holding, biased, tempted to add more, not SEBI registered

Ranvir’s Portfolio (18-11-2023)

EIH Q2 concall highlights –

Sales – 552 vs 417 cr, 32 pc

EBITDA – 165 vs 101 cr, up 66 pc

PAT – 94 vs 22 cr, up 256 pc

Net cash on balance sheet @ 509 cr

Out of the total revenues, revenues from flight catering and airport lounge business @ 100 vs 56 cr, EBITDA @ 37 vs (-) 3 cr

City wise Rev Par growth (YoY) for EIH properties in Q2 –

Agra – 60pc

Delhi NCR – 38 pc

International – 28 pc

Jaipur – 28 pc

Bhubneshwar – 26 pc

Chennai – 23 pc

Mumbai – 19 pc

Kolkata – 12 pc

Hyderabad – 12 pc

Bengaluru – 9 pc

Udaipur – 7 pc

Cochin – (-) 11 pc

Chandigarh / Shimla – (-) 35 pc – due floods

EIH Domestic hotels ( including managed ) vital stats – Q2 (YoY) –

ADRR – Rs 16500, up 23 pc

Occupancy – Flat

RevPAR – Rs 11865, up 20 pc

National presence –

12 Oberoi branded hotels

10 Trident branded hotels

Total rooms @ 3772

International presence –

07 Oberoi branded hotels

Total rooms – 497

Growth in ADRRs (YoY) in luxury / 5 Star part of the Industry is in 20s vs low teens for 2-3 star properties

Current number of 5 star and above rooms avlb in India @ 1.65 lakh. New supply coming on stream till FY 28 @ 0.55 lakh. Basically the demand – supply dynamics look good for next 5 yrs !!!

CWC should help the company in Q3 wrt rates, occupancy

Q3 – recovery in Shimla has been promising specially at The Cecil. The Windflower hall is taking slightly longer for full recovery as Cecil receives greater chunk of foreign tourists ( specially from UK due to its Historical value )

Middle East properties are seeing some pressure due to the ongoing Israel – Hamas conflict

EIH – vision for 2030 – minimum 50 more hotels with additional 4500 keys ( including managed Hotels ) – Confident of achieving the same. 03 hotels already in pipeline – Tirupati, Rajgarh, Vizag

Business in H2 should be good

According to Mr Oberoi- despite sharp increases in ARRs across 5 star properties, there is still a lot of head room for further growth

RIL has announced that 03 of its properties ( 02 in Mumbai and 01 in UK ) shall be managed by EIH in near future. The UK property is a 47 room hotel, purchased by RIL in 2021. The two groups shall also develop a new property in Gujarat the details of which are not yet known

RIL owns 19 pc in EIH. Another 14 pc is owned by ITC

Disc: holding, biased, tempted to add more, not SEBI registered

Screener.in: The destination for Intelligent Screening & Reporting in India (18-11-2023)

Is there a feature in the screener to filter companies that are doing con-calls or any plans to add it in future?