Hi Manoj Is this List Updated in Google Drive ?, Very useful one Thank you for Sharing

Posts tagged Value Pickr

Investing Basics – Feel free to ask the most basic questions (17-11-2023)

Kindly check my edited post

Its ok for xirr calculation?

W S industries – Opportunities lying ahead if any (17-11-2023)

Anyone tracking W S industries?

Investing Basics – Feel free to ask the most basic questions (17-11-2023)

That is correct. You could check this too for some additional information.

And there are detailed calculating sheets available

You can check this too.

Fdc ltd (17-11-2023)

FDC Q2 highlights –

Sales – 486 vs 445 cr

EBITDA – 76 vs 67 cr, up 13 pc (margins @ 16 vs 15 pc) Margins in Q1 were 23 pc

PAT – 70 vs 52 cr ( other income @ 27 vs 13 cr )

Sales breakdown –

India formulation sales @ 391 vs 369 cr

Export formulation sales @ 76 vs 57 cr

API sales @ 19 vs 18 cr

Board approved buyback of 31 lakh shares @ Rs 500/share – that amounts to a buyback amount of Rs 150 cr – a significant amount

Last 5 yr growth data –

Sales growth @ 13 pc CAGR

India formulations sales growth @ 13 pc CAGR

Intl formulations sales growth @ 17 pc CAGR

API sales growth @ 11 pc CAGR

India business –

4800+ MRs

9 brands with sales > 50 cr

6 brands with no 1 rank in molecule category

Electral has annual sales > 400 cr

ZIFI (Cefixime-anti bacterial) has annual sales > 300 cr

Enerzal has annual sales approaching 200 cr

ZIFI-X – Ceftriaxone injection – (cephalosporin antibiotic injectable ) launched in Jun 23 – doing well

In H1, price growth is around 4.9 pc with new product growth at 0.9 pc. Legacy portfolio’s volume growth has been flat. Company finally seeing volume growth in Oct 23

Have filed 2 ANDAs in H1

Company focussing on expanding in East India where it was traditionally weak. Making descent inroads in Bihar, Orrisa, WB

Also investing behind Nutraceuticals and Derma portfolio

Certain one off expenditures in Q2 led to suppression of EBITDA margins vs Q1. However, Q1 is always the strongest Qtr with best margins for FDC Ltd

Export business momentum remains strong, expected to remain strong

Export business is already profitable, capable of funding its own growth ( minus the R&D expenses )

To focus on Opthal business wrt US mkts as the company is strong in this particular therapy

Company has 6-7 brands that generate sales > 50 cr ( except for the top 3 brands ). These are the brands where the company intends to extract higher growth and make them into 100 cr + brands

Hence the company intends to not go for aggressive new launches. Focus shall be to grow above mentioned brands into bigger ones

However, company intends to launch brand extension of the a/m brands

Henceforth, the company intends to conduct half yearly concalls

Mum-Mum infant formula is a very promising brand and company intends to grow this aggressively

Regular maint capex @ 50 cr/ yr

Disc: holding, biased, not SEBI registered

Ranvir’s Portfolio (17-11-2023)

FDC Q2 highlights –

Sales – 486 vs 445 cr

EBITDA – 76 vs 67 cr, up 13 pc (margins @ 16 vs 15 pc) Margins in Q1 were 23 pc

PAT – 70 vs 52 cr ( other income @ 27 vs 13 cr )

Sales breakdown –

India formulation sales @ 391 vs 369 cr

Export formulation sales @ 76 vs 57 cr

API sales @ 19 vs 18 cr

Board approved buyback of 31 lakh shares @ Rs 500/share – that amounts to a buyback amount of Rs 150 cr – a significant amount

Last 5 yr growth data –

Sales growth @ 13 pc CAGR

India formulations sales growth @ 13 pc CAGR

Intl formulations sales growth @ 17 pc CAGR

API sales growth @ 11 pc CAGR

India business –

4800+ MRs

9 brands with sales > 50 cr

6 brands with no 1 rank in molecule category

Electral has annual sales > 400 cr

ZIFI (Cefixime-anti bacterial) has annual sales > 300 cr

Enerzal has annual sales approaching 200 cr

ZIFI-X – Ceftriaxone injection – (cephalosporin antibiotic injectable ) launched in Jun 23 – doing well

In H1, price growth is around 4.9 pc with new product growth at 0.9 pc. Legacy portfolio’s volume growth has been flat. Company finally seeing volume growth in Oct 23

Have filed 2 ANDAs in H1

Company focussing on expanding in East India where it was traditionally weak. Making descent inroads in Bihar, Orrisa, WB

Also investing behind Nutraceuticals and Derma portfolio

Certain one off expenditures in Q2 led to suppression of EBITDA margins vs Q1. However, Q1 is always the strongest Qtr with best margins for FDC Ltd

Export business momentum remains strong, expected to remain strong

Export business is already profitable, capable of funding its own growth ( minus the R&D expenses )

To focus on Opthal business wrt US mkts as the company is strong in this particular therapy

Company has 6-7 brands that generate sales > 50 cr ( except for the top 3 brands ). These are the brands where the company intends to extract higher growth and make them into 100 cr + brands

Hence the company intends to not go for aggressive new launches. Focus shall be to grow above mentioned brands into bigger ones

However, company intends to launch brand extension of the a/m brands

Henceforth, the company intends to conduct half yearly concalls

Mum-Mum infant formula is a very promising brand and company intends to grow this aggressively

Regular maint capex @ 50 cr/ yr

Disc: holding, biased, not SEBI registered

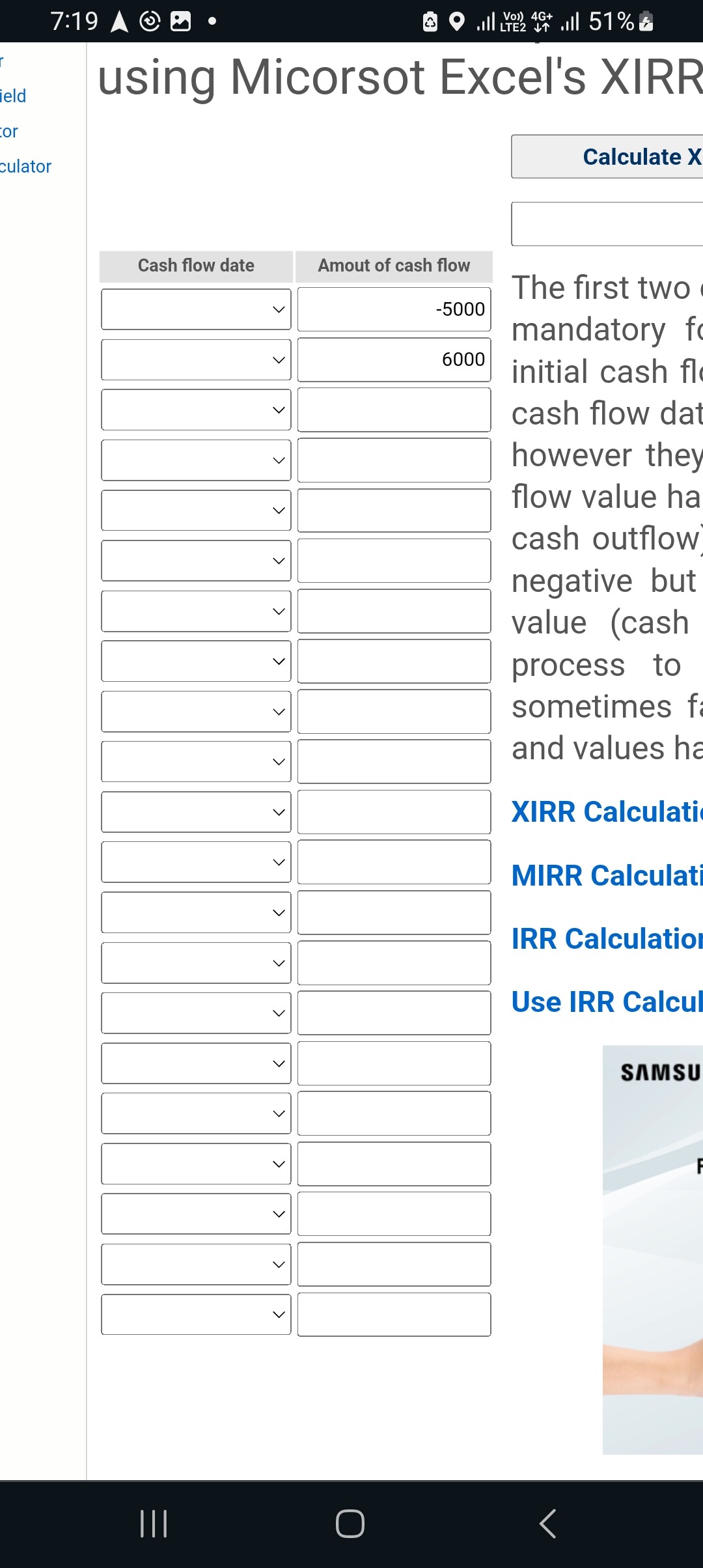

Investing Basics – Feel free to ask the most basic questions (17-11-2023)

Is this right method to calculate XIRR?

A…I considered all my investments along with dates as negative.

B…I had hardly sell my stocks, so not mentioned

C…In last row, i considered my total investment value (as of today )as positive.

Kindly guide

Thanks

Affle India – India Mobile Internet Advertising Leader (17-11-2023)

Let’s talk patents!

Affle India has announced that they have filed the following patents in India. This post will try and breakdown what these patents could potentially bring to the company.

NOTE: This is just my understanding of the patents.

What is an AI agent?

For those with a non-CS background: In artificial intelligence, an agent is a computer program or system that is designed to perceive its environment, make decisions and take actions to achieve a specific goal or set of goals. An example of a Gaming Agent is a computer program to play chess with a human opponent. For the context of Affle, these agents that they are talking about are designed to analyze data, make decisions, and optimize various aspects of the advertising process.

Patent list

-

Systems and methods for ownership and biometric based authentication through Artificial Intelligent (AI) agent.

It looks like the system that is mentioned provides a secure and convenient way to assign ownership to data. Those who are authorised to access this data, can use biometric authentication to verify their identity ensuring that only authorized individuals can access this digital information.

Type: Security -

Systems and methods for managing a secure cloud based enclave without breach of user privacy.

The enclave is a secure environment within the cloud that is isolated from the rest of the cloud environment. This isolation helps to protect user data from unauthorized access. The patent also describes methods for managing the enclave, such as provisioning, monitoring, and revoking access.

Type: Security, New services -

Systems and methods for categorizing personal information into relevant categories corresponding to social engagement AI agents in a privacy and ad sensitive manner.

The system uses natural language processing (NLP) and machine learning (ML) to extract and categorize personal information from social media posts, emails, and other online sources. The system then uses this categorized information to create profiles of individuals, which can be used by social engagement AI agents to tailor their interactions with users.

Type: Security -

Systems and methods for augmenting responses/recommendations and generating enhanced decisions through resource sharing between AI agents.

The system allows AI agents to share their knowledge and resources with each other, which can help to improve the quality of their responses and recommendations. The system also allows AI agents to learn from each other’s mistakes, which can help to prevent them from making the same mistakes in the future.

Type: Optimzation -

Collaborative AI agent systems with coordinators/recommendations for shared applications and methods thereof.

The system enables multiple AI agents to collaborate on tasks and problems, coordinating their efforts and sharing information to achieve common goals. The system also provides a mechanism for recommending actions or strategies to the AI agents based on their collective knowledge and experience.

Type: Optimization

Potential new revenue streams:

- Subscription fees: The company could charge users a monthly or annual subscription fee to use the systems and enclaves.

- Professional/Management services: The company could offer professional services to help customers deploy, manage, and secure their enclaves.

- Licensing fees: The company could license the technology to other companies in the AdTech industry.

- Data sales: The company could collect and sell data about user activity to advertisers and other businesses.

- Partnerships: The company could partner with other cloud providers to offer the enclave as a managed service.

Summary:

The patents filed are focused on two primary aspects: security and optimization. What they would ultimately help in is improving margins and securing data. This is directly linked to the effective CPCu business model of Affle. It’s important to note that the more they work on fine tuning their algorithms, it will trickle down to their OPM margins. The effective CPCu (cost per converted user) will increase, and customers will not mind paying a premium to tap into Affle’s algorithms and consumer base. The security oriented patents might not correlate directly to revenue, but what they will help in is building trust among its customers and consumers on ethical data handling. It’s too early to comment on any new revenue streams that these patents would allow for, hopefully the company addresses these patents in a discussion or presentation.

Please note that these patents have only been filed and have not yet been granted. Let’s hope that all/most of them are granted to add to the impressive patents count and the R&D culture of the company.

Affle India – India Mobile Internet Advertising Leader (17-11-2023)

(post deleted by author)

Satia Industries – Journey towards Cyclical to Shallow Cyclical? (17-11-2023)

Shot an email and got the reply!!

Got reply within an hour…Super quick response!