Is source of this is from AGM? I didn’t hear the word ‘abroad’ or I may have missed it.

Posts tagged Value Pickr

LUX INDUSTRIES – Can it Scale? (17-11-2023)

Is anyone following the tax evasion update? Has anyone ever met/spoken to management to know their background on ethics? what is the max. penalty for this in case they are guilty?

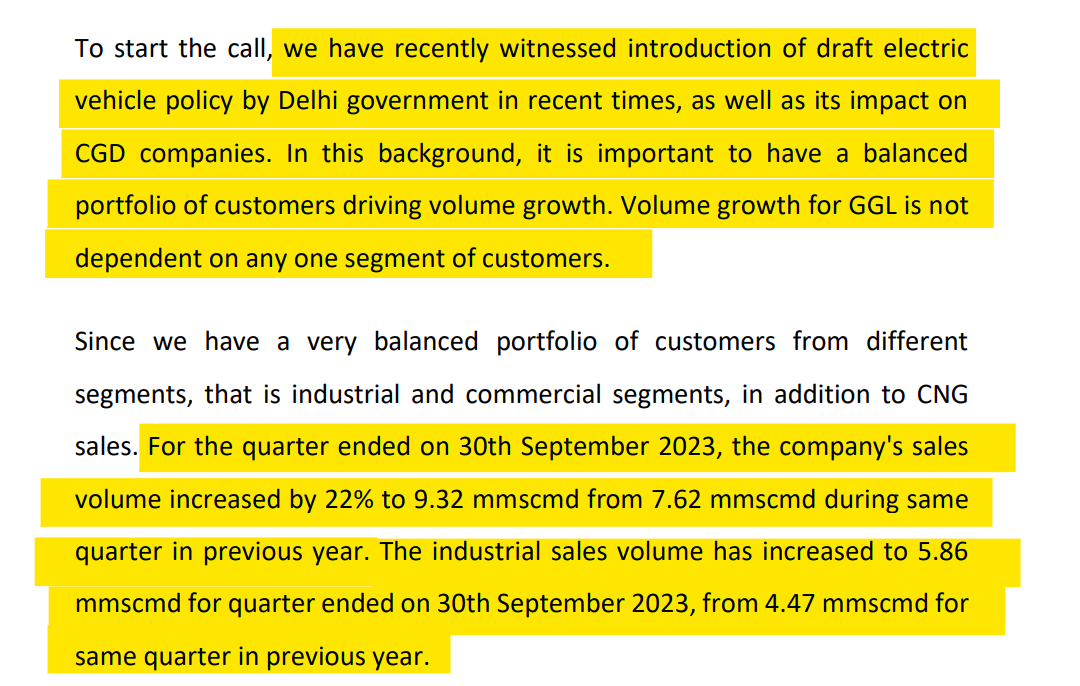

GUJARAT GAS Improving outlook on volumes (17-11-2023)

Recent con call GGL’s chief financial officer said that the volume of GGL is not dependent on any one segment. Since GGL has a very balanced portfolio of customers from different segments, that is industrial and commercial segments, in addition to CNG sales.

So maybe it not might affect GGL as compared to IGL

Marksans Pharma- Can it be the next Pharma Biggie? (17-11-2023)

Q2FY24 Short Notes:

Vision of the Company:

Strengthening the product pipeline and creating a complete offering in four key therapeutic segments that is pain, cough and cold, gastro, and anti- allergy.

Revenue Potential:

Revenue growth 17% y-o-y. Management confident of Good Revenue Growth next year due to improved demand from all geographies which has increased the order Book

Company recently received key product approvals from USFDA and market authorization from UK MHRA in the pain segment, cough and cold segment, and digestive.

Company planning for 5 product approvals in US and 20 product approvals in Europe year on year.

Currently OTC: Rx proportion is 70:30. In future it will remain in the same range or in the range of 75:25.

Company planning to doubling the supplies to the geographies they are operating with acquisition of the TEVA Plant. So, Teva will contribute to equivalent amount of revenue like existing old Plant.

Revenue contribution to increase from Teva facility Quarter on Quarter. Full Revenue potential from April 2024 onwards.

Margin Potential:

EBITDA and PAT Growth 40% y-o-y.

Improved Margins was result of Cost efficiencies and Reduction in Raw Material and freight Cost. Management believes that same will continue in the next half of the year.

Backward integration on three molecules which form 30% of the overall Revenue. This will help in improvement of the margins. This will kick in from mid to latter part of 2024

Compliances:

USFDA inspection conducted in October 2023 for a wholly owned subsidiary time cap laboratories and was completed with EIR status.

Teva Facility audit by German Authorities with no major observation.

Capital Allocation Strategy:

Company remains debt free with Total Cash of Rs 661 crore. Exploring options of M&A in Europe. Company is presently in Generic area. If Good M& A options come in Branded medicine in India, company will explore it.

R&D spend to be 2% from the present 1.6% of the Total revenue.

Brand concept – New Emerging Micro cap Retailer (17-11-2023)

great update, thanks Mayank.

Jupiter Wagons Ltd (previously CEBBCO) (17-11-2023)

Important points:

- For backward integration company is starting to make wheels, braking systems and foundry operations.

- By FY25 company will be making 1000 wagons per month from 700 currently.

- 20,000 wagon tender of Railways is closing on 15 November and two separate tenders of 10,000 units each for deferent design wagons, including aluminium wagons, are expected before the end of current fiscal year.

- ARAI certification for commercial EV will be available by December or January.

- Commercial rollout of vehicles expected in April 2025 and they expect to sell 2000 vehicles in first year.

Praveen’s Information Attic (Obervations, Lessons, Thoughts) (17-11-2023)

Today I happened to look at the stock of SBI cards as there’s some news chatter around it (RBI changes risk weights for Unsecured lending). I could see that the stock is still trading @733 at close against IPO issue price of 755 Rs. Few things that are hampering the stock performance are

- P/B is 6.3, which is expensive, but the growth is also good as the co. grew it’s book value at ~26% CAGR over past 3.4 years

- Loss in spends market share from 19.1% to ~17.5%

Positives:

- ROE is 25.7%

- P/E is ~30x

- Asset quality is decent. GNPA 2.43% and NNPA ~0.9%

- Along with above metrics, short to medium term trigger would be cutting down of incentives by Credit Card cos (like removing lounge access or restricting it, More constrains on cashback (not allowed for offline spends, or constrains like that)

- Technicals: 3 year low is ~680 levels, which may protect the downside

Considering above points the co. looks expensive in terms or P/B (but reasonably valued in terms of P/E, if someone considers this metric for evaluation).

Views on co:

Co has always looked highly valued, as there are good story/narratives around the future of Credit Card business in India and TINA (There Is No Alternative) factor. But, considering the historical valuation, the co is avaialblle at good price (since it’s close to historical lows), but not too attractive at current levels when compared with other alternatives avaialble.

Disc: No recommendation. No position at the moment, but open to buy/trade in future

Praveen

Tara Chand Infralogistic Solutions Ltd (17-11-2023)

I Recently Came Across this Microcap Company

With Business model Combined to that of ACE and Sanghvi Movers

I have Made my notes on it and sharing the same

Views are welcomed

Disclaimer – Not Invested but Tracking to get better Price

Tara Chand Infralogistic Solutions Ltd.pdf (851.9 KB)

Arvind SmartSpaces: Will it make smartspace for Retail Investors? (17-11-2023)

I thought this is live. As this community driven, if you fel it does not look like live, please make it live with meaningful posts!

is there anything changing? Last 5 years, looks like nothing changed in revenue or profit, rather they deteriorated as per screener when I had a quick look.