Can you include LTI nindtree and TATA Elxsi in peer to peer comparison?

Posts tagged Value Pickr

Mudit’s Portfolio (Passively Active) (17-11-2023)

REGULATORYMEASURES8785E7886A044B678FB8AF2C6C051807_231117_065203.pdf (249.3 KB)

Regulatory measures towards consumer credit and bank credit to NBFCs in line with recent announcement by RBI GOVERNOR

![]() Consumer credit by banks and NBFCs to attract 125% risk weight, from 100% previously

Consumer credit by banks and NBFCs to attract 125% risk weight, from 100% previously

![]() Credit card loans by banks to attract 150% risk weight from 125% previously

Credit card loans by banks to attract 150% risk weight from 125% previously

![]() Credit card loans by NBFCs to attract 125% risk weight from 100% previously

Credit card loans by NBFCs to attract 125% risk weight from 100% previously

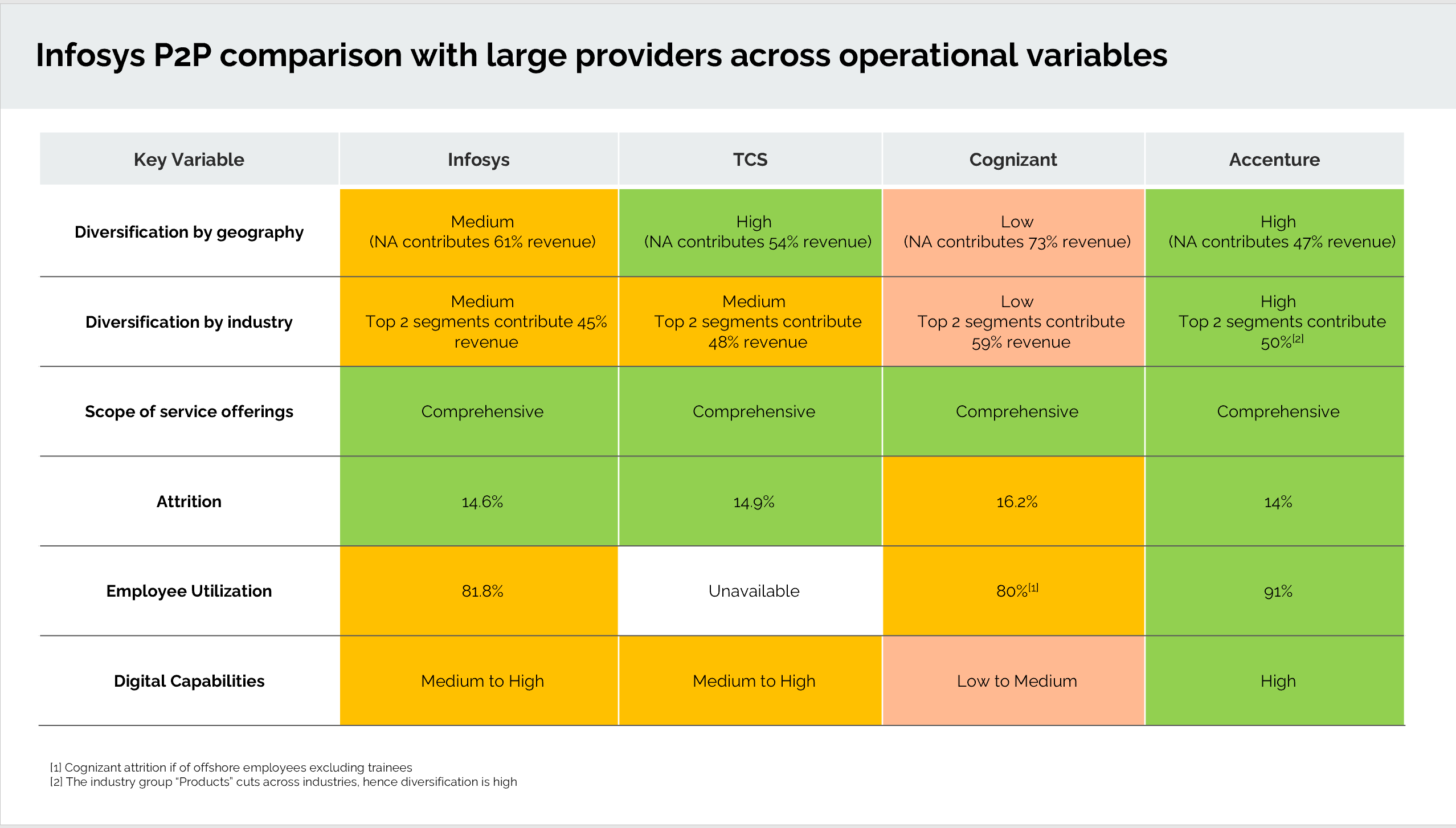

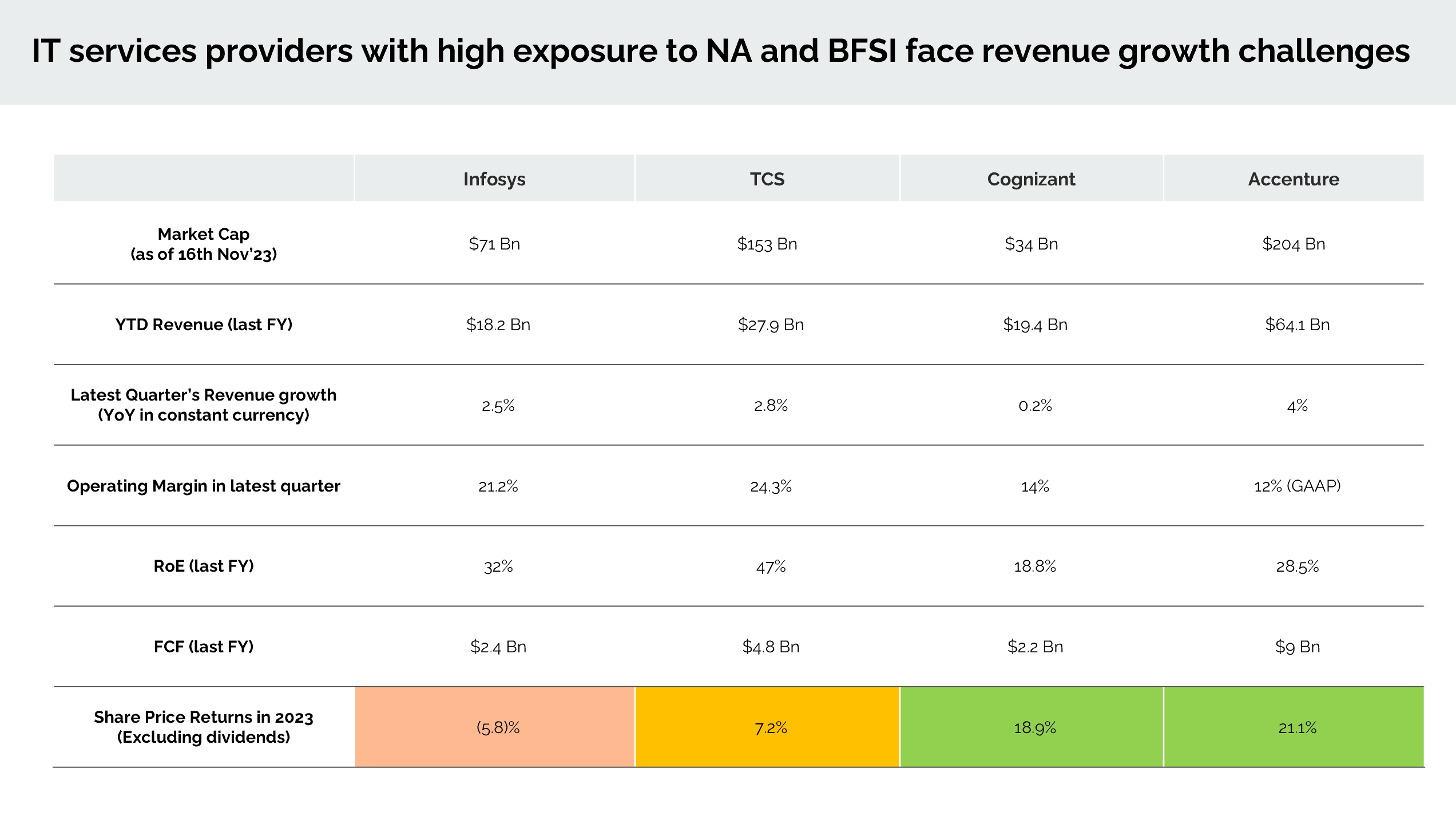

Infosys Limited – Are we getting a discount or no? (17-11-2023)

Did quick P2P Comparison:

Across operational variables:

Across latest numbers:

The harsh portfolio! (17-11-2023)

Sales were reported at 1235 cr, less QoQ and YoY, still PAT at 192. Not an expert in reading figures, eager to understand.

The harsh portfolio! (16-11-2023)

I have made a few changes to the model portfolio:

-

Initiated 1% position in Sharat Industries. I plan to play the shrimp sector via the market leader Avanti, where I already own 4% position and a smaller co like Sharat which can benefit disproportionately with revival in the industry. Sharat is currently operating at 50% utilization and has reported good quarterly results (flat sales, 32% EBITDA growth, 64% EPS growth). Management has been guiding for 15-20% sales growth, 20-25% EBITDA growth, and 25-30% PAT growth over next 3-4 years. By FY26, they want to reach 9-11% EBITDA margin by improving their capacity utilization. If this turns out to be the case, their FY26 revenues can be around 500 cr. and they can potentially report 20-25 cr. PAT. Their current market cap of 137 cr. offers a very good risk reward.

-

Reduced position size in NESCO (from 4% to 2%), Ajanta Pharma (from 4% to 2%), Sundaram Finance (from 2% to 1%). This transaction is largely to make space for new companies in the portfolio, and reallocation to other bets, where I feel risk reward is better. Ajanta has been one of my favorite businesses, however they have been topping out around 6.5x sales, where they are currently trading. Nesco is not so expensive, so my quantum of selling has been much more measured here. Sundaram has doubled since I bought, and are now trading at higher end of their valuation band, hence taking money off table.

-

Increased position size in Aegis Logistics from 2% to 4%. I have been amazed at how Aegis has grown over time. Its rare to find a small cap which has grown profits by 10x+ in 10 years, while maintaining 20-40% dividend payout without equity dilution.

They have managed to reach PAT/fixed assets of 15-20% in good times. With current LPG expansion, their net block in 3 years will be around 5000 cr., which implies they can reach potential PAT of ~1000 cr (vs 510 cr. in FY23). I am reasonably confident of them achieving these nos, given their very good track record. Current valuation of 21x PE is towards the lower end of their traded band.

-

Increased position size in Propequity from 2% to 4%. This is largely due to stock doubling in quick time, rather than me adding to existing positions. They have been scaling very well, and plan to maintain sales growth of 30%+ in the near term. Their current revenue runrate is around 35 cr., and I feel they can reach 70-80 cr. sales in next 3-4 years. As this is a unique business model with very high margins and low capital requirement, I feel market will ascribe 10x+ Mcap/sales if they scale well, and I hope that they cross 1000 cr. Mcap in the next few years.

-

Reintroduced Chamanlal Setia at 2% position size. The numbers being reported by Chamanlal is worth noticing. For these kind of nos, I feel 8-9x PE is quite cheap. This being a cyclical space, I am closely tracking basmati prices as any sharp drawdown in that can bring down their earnings. I just hope that I am not buying at peak earnings!

Updated folio is below and cash stays at zero.

Core compounder (44%)

| Companies | Weightage |

|---|---|

| Aegis Logistics Ltd. | 4.00% |

| Eris Lifesciences Ltd. | 4.00% |

| HDFC Bank Ltd. | 4.00% |

| HDFC Asset Management Company Ltd | 4.00% |

| Gufic Biosciences | 4.00% |

| Godfrey Phillips | 4.00% |

| P.E. Analytics Ltd | 4.00% |

| Ajanta Pharmaceuticals Ltd. | 2.00% |

| NESCO Ltd. | 2.00% |

| I T C Ltd. | 2.00% |

| PI Industries Ltd. | 2.00% |

| LINCOLN PHARMACEUTICALS LTD. | 2.00% |

| Caplin Point Laboratories Ltd. | 2.00% |

| Aptus Value Housing Finance India Ltd. | 2.00% |

| Shree Ganesh Remedies Ltd – PP | 2.00% |

Cyclical (44%)

| Companies | Weightage |

|---|---|

| Kolte-Patil Developers Ltd. | 4.00% |

| Avanti Feeds Ltd. | 4.00% |

| Alembic Pharmaceuticals Ltd. | 4.00% |

| Amara Raja Batteries Ltd. | 4.00% |

| Sharda Cropchem Ltd. | 2.00% |

| Stylam Industries Limited | 2.00% |

| Ashiana Housing Ltd. | 2.00% |

| Ashok Leyland Ltd. | 2.00% |

| Kaveri Seed Company Ltd. | 2.00% |

| Time Technoplast Ltd. | 2.00% |

| RACL Geartech Ltd | 2.00% |

| Manappuram Finance Ltd. | 2.00% |

| ANUH PHARMA LTD. | 2.00% |

| Dharmaj Crop Guard Ltd | 2.00% |

| MAYUR UNIQUOTERS LTD. | 2.00% |

| Godrej Agrovet Ltd. | 2.00% |

| Chaman Lal Setia Exp | 2.00% |

| KSE LTD. | 1.00% |

| Sundaram Finance Ltd. | 1.00% |

Turnaround (2%)

| Companies | Weightage |

|---|---|

| Punjab Chem. & Corp | 2.00% |

Deep value (10%)

| Companies | Weightage |

|---|---|

| Geekay Wires | 2.00% |

| Worth Peripherals Ltd | 2.00% |

| Sharat Industries | 1.00% |

| Jagran Prakashan Ltd. | 1.00% |

| D.B.Corp Ltd. | 1.00% |

| Shemaroo Entertainment Ltd. | 1.00% |

| Modison Metals | 1.00% |

| RKEC Projects | 1.00% |

I have never found a single good stock idea from a MF, instead I have seen a lot of MFs buying a stock I already own or track, which then increases its valuation. So, I am not the right person to answer this. On VP, there is no dearth of stock ideas.

Very good performance, I have increased allocation a bit, but not a lot. In hindsight, I should have taken larger bets on a number of pharma cos earlier this year (SGRL, Caplin, Anuh, Lincoln, Ajanta). But overall I am reasonably satisfied with my bunch of pharma cos, I will try to increase position in SGRL if there is a big dip.

Religare Enterprises (16-11-2023)

Here is the Ingovern report in Religare. This investor advisory firm backs Burman’s case against Religare Chairman. To read this report in favour of minority shareholders, one needs to understand the history of REL and read this report between the lines.

Religare-CG Alert Remuneration-November 2023.pdf (260.6 KB)

Ashiana Housing – Banking on Tier II and III towns! (16-11-2023)

Ashiana had their second best quarter since 2016. Demand seems to be very strong, and management is confident of reaching 1500 cr. presales in FY24. Project pipeline remains strong

FY24Q2

- Current pipeline: 12 lakh sq.ft in ongoing projects + 84 lakh sq.ft in future projects + 21 lakh sq.ft in land (excluding Milakpur and Kolkata) ~ 117 lakh sq.ft

- Annual sales volume run rate should increase from 25 lakh sq.ft (12.45 lakh sq.ft sold in H1FY24)

- Greenfield projects: 6 (3 in Jaipur, 1 in Gurgaon, 2 senior living in Chennai). 4 will be launched in remaining FY24 and 2 in FY25

- Ashiana Amodh (Pune, senior living): Successful launch (27% of Phase 1 inventory sold this quarter)

- Ashiana Shubham (Chennai, senior living): Last phase launched (56% of inventory sold this quarter)

- Ashiana Prakriti (Jamshedpur): Phase 2 launched (76% inventory sold this quarter)

- Jaipur: Acquired new land in Jaisingpura (11 lakh sq.ft). Its near the Ashiana Ekansh project

- Construction: Will do 2-2.2mn sq.ft in FY24 (0.9 mn sq.ft constructed in H1)

- Larger focus will be on increasing prices

- Will not get into horizontal plotted development

- New Gurgaon prices have increased 2-3x over last 5 years (Ashiana Amarah region)

- Channel partners in NCR add a lot of value as there are lots of projects available in this region. This is not the case in Jaipur or smaller cities

- Senior living is gaining a lot of traction

- Economic ROE will cross 15% in FY24 and seem sustainable (and probably higher than 15%)

- FY25-27: Plan to do cumulative delivery of 50 lakh sq.ft (2600-3000 cr. revenues)

- Kid-centric projects: Planned launch of one project in Gurgaon and one in Jaipur. First sign is evident in Ashiana Umang.

Disclosure: Invested (position size here, no transactions in last-30 days)

Religare Enterprises (16-11-2023)

During the last five years, Religare Enterprises has moved from a loss to profitability. That kind of transition can be an inflection point that justifies a strong share price gain in coming time. The business is just fully ready to fire on all cylinders, and Burmans coming in will bring substantial positives.

Disclosure: I have holding and tracking the company since 2018, so my opinion may be biassed. Thank you

Time technoplast (16-11-2023)

I am pleasantly surprised that Time Technoplast has gotten into a very good growth patch, with improvement in margins and continued growth in sales. Sales grew by 16.6% and EPS by 41% this quarter. They are close to finalizing the international divestment deal. Concall notes below.

FY24Q2

- FY24 revenues should cross 5000 cr. (H1:H2 revenue mix is 45:55)

- Debt reduced by 2 cr. in Q2FY24

- Capex: 55 cr. (22 cr. towards established products + 33 cr. towards value-added products)

- CNG cascade: order book of 225 cr.

- FY24 expected ROCE: 15.5% and 1.5% improvement each year

- 18-22% margins in composite cylinders

- Seeing 15%+ growth in IBCs. GNX brand from Time Technoplast has been well established globally and is their main competitive advantage, as overseas customers ask for GNX IBCs for chemical shipments

- Target divestment of 100 cr. of non-core assets and no non-core assets by FY25

- Overseas divestment: valuation of ~1000 cr., will be selling 80%. Will be finished in FY24

I am also adding my notes from their AGM held earlier.

AGM23 notes

- LPG Composite cylinders: Added new countries like Taiwan, Ghana, Nigeria, Bermuda, St. Lucia, Romania, Burundi and Australia. Applied for approval to supply LPG cylinders to the USA

- CNG cascade cylinder order book: 250 cr.

- Introduction of Multi-Layer Technology for Industrial Packaging products (Drums, Jerry cans and IBCs) for use of Post Consumer Recycled (PCR) material in the middle layer of the product and use of PCR material to manufacture IBC Components are few steps in that direction. To encourage reuse of IBC, innovative business models such as cross bottling, collection, rebottling and reuse is now the new norm

- Overseas divestment: offering businesses on the basis of 3 regions, i.e. USA, South East Asia (including Taiwan) and MENA Region. Due diligence including legal process is on for two out of three regions and is expected to be completed any time soon

- FY24 capex: ~200 cr.

Disclosure: Invested (position size here, no transactions in last-30 days)

Amara Raja Energy & Mobility Limited: Powering Ahead (16-11-2023)

Thank you @Nishant_Sampat for the Report – which gives us many more avenues to explore ARE&M New Energy division plans/viability

Another slightly dated report (2022) highlights a crucial aspect: Re-emergence of LFP tech, and why Tesla and VW have reposed full faith in LFP now (Chinese Patents expiry in 2022 – my have been a big contributing factor, even for ARE&M?

Some other (could be useful) Reports/Articles

Battery ecosystem: A global overview, gap analysis in Indian context

Understanding Lithium-ion/other

Investor Perspectives on growth of Indin Electric Vehicle Ecosystem